- Canada

- /

- Renewable Energy

- /

- TSX:PIF

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Polaris Infrastructure Inc.'s (TSE:PIF) CEO For Now

Performance at Polaris Infrastructure Inc. (TSE:PIF) has been reasonably good and CEO Marc Murnaghan has done a decent job of steering the company in the right direction. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 24 June 2021. However, some shareholders will still be cautious of paying the CEO excessively.

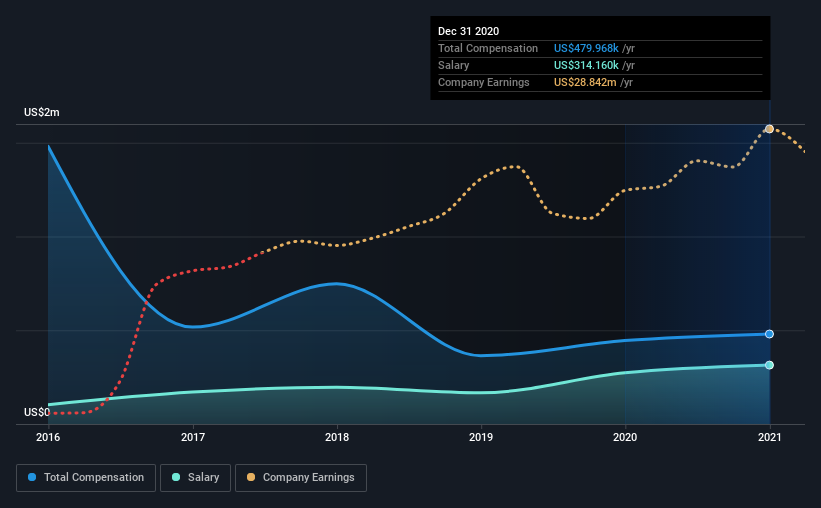

Check out our latest analysis for Polaris Infrastructure

Comparing Polaris Infrastructure Inc.'s CEO Compensation With the industry

Our data indicates that Polaris Infrastructure Inc. has a market capitalization of CA$362m, and total annual CEO compensation was reported as US$480k for the year to December 2020. That's just a smallish increase of 7.9% on last year. In particular, the salary of US$314.2k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar companies from the same industry with market caps ranging from CA$125m to CA$499m, we found that the median CEO total compensation was US$281k. Accordingly, our analysis reveals that Polaris Infrastructure Inc. pays Marc Murnaghan north of the industry median. Furthermore, Marc Murnaghan directly owns CA$8.2m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$314k | US$273k | 65% |

| Other | US$166k | US$171k | 35% |

| Total Compensation | US$480k | US$445k | 100% |

On an industry level, around 49% of total compensation represents salary and 51% is other remuneration. According to our research, Polaris Infrastructure has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Polaris Infrastructure Inc.'s Growth Numbers

Over the past three years, Polaris Infrastructure Inc. has seen its earnings per share (EPS) grow by 90% per year. Its revenue is down 3.8% over the previous year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. While it would be good to see revenue growth, profits matter more in the end. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Polaris Infrastructure Inc. Been A Good Investment?

We think that the total shareholder return of 53%, over three years, would leave most Polaris Infrastructure Inc. shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 4 warning signs for Polaris Infrastructure (1 is a bit concerning!) that you should be aware of before investing here.

Switching gears from Polaris Infrastructure, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:PIF

Polaris Renewable Energy

Engages in the acquisition, exploration, development, and operation of renewable energy projects in Latin America and the Caribbean.

Undervalued established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)