- Canada

- /

- Electric Utilities

- /

- TSX:FTS

Fortis (TSX:FTS) Valuation Check After Capital Plan Boost, Earnings Growth and Dividend Increase

Reviewed by Simply Wall St

Fortis (TSX:FTS) is back in the spotlight after Q3 results showed rate base growth humming along, an 11% bump in its multi year capital plan, and another uptick in the dividend.

See our latest analysis for Fortis.

Those steady updates on capital spending and dividends seem to be filtering into the market, with Fortis’s share price at $69.25 and a robust year to date share price return of 16.15%, translating into a 19.35% one year total shareholder return and signalling gradually improving momentum for a traditionally defensive utility.

If Fortis’s mix of stability and growth has you thinking bigger picture, this could be a good moment to explore fast growing stocks with high insider ownership for other compelling ideas with strong alignment between management and shareholders.

With earnings still grinding higher, a bigger capital plan in place, and the dividend marching upward, is Fortis quietly trading below its true value, or are investors already paying up for that future growth?

Most Popular Narrative: 5.3% Undervalued

With Fortis last closing at CA$69.25 against a narrative fair value of CA$73.10, the storyline leans toward modest upside driven by regulated growth.

Substantial planned capital investments in grid modernization, renewable energy integration, and battery storage (e.g., $2.9B invested in H1 2025 and upcoming projects at ITC and FortisBC) position the company to benefit from policy-driven infrastructure upgrades and decarbonization mandates, supporting above-average asset base growth and improved earnings visibility.

Want to see what powers that upside view? The narrative quietly stacks revenue growth, margin expansion and a richer profit multiple into one long term playbook. Curious how those pieces fit together, and what they imply for earnings a few years from now? Dive in to uncover the full valuation blueprint behind that fair value.

Result: Fair Value of $73.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that blueprint could unravel if regulators push back on rate hikes or if higher interest costs erode returns on Fortis’s expanded capital plan.

Find out about the key risks to this Fortis narrative.

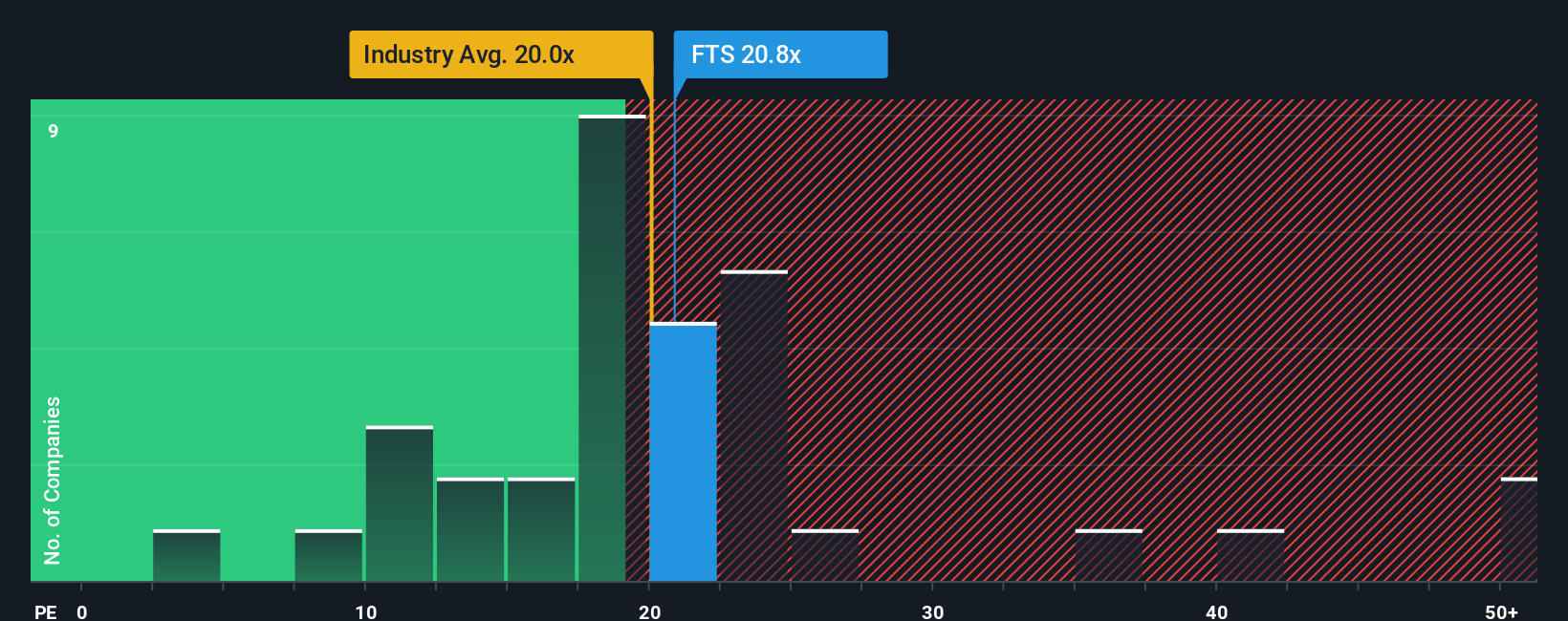

Another View: Market Multiples Look Less Generous

Step away from that 5.3% upside story and a simple earnings multiple paints a tougher picture. Fortis trades on about 20.6x earnings, richer than the North American utilities sector at 19.9x and its own 20.5x fair ratio, which hints at limited margin for error if growth disappoints.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fortis Narrative

If you see things differently or just like digging into the numbers yourself, you can spin up a fresh narrative in minutes with Do it your way.

A great starting point for your Fortis research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next investing move?

Before you lock in any decision on Fortis, put its story in context by lining it up against fresh ideas from the Simply Wall St Screener today.

- Capture potential mispricings by scanning these 907 undervalued stocks based on cash flows that the market may be overlooking right now.

- Ride powerful tech tailwinds by targeting these 25 AI penny stocks shaping the next wave of intelligent software and automation.

- Strengthen your income stream by reviewing these 12 dividend stocks with yields > 3% that could boost your portfolio’s cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:FTS

Fortis

Operates as an electric and gas utility company in Canada, the United States, and the Caribbean countries.

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion