Advertisement

- Canada

- /

- Transportation

- /

- TSX:CP

Canadian Pacific Kansas City Valuation After Cross Border Network Expansion and Recent Share Price Rebound

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Canadian Pacific Kansas City is fairly priced or if the market is overlooking something, you are not alone. This stock often divides opinion among long term investors.

- Over the last week the share price has crept up about 2.1%, and it is up roughly 3.7% over the past month. However, it is still down around 2.9% over the last year and only modestly ahead over three years, which hints at shifting sentiment rather than a runaway growth story.

- Recent headlines have focused on the strategic potential of its cross border network after the Kansas City Southern merger closed, with investors weighing how much long term value a uniquely integrated Canada to Mexico rail route can unlock. At the same time, debate around North American freight volumes, trade flows and infrastructure spending has kept the stock in the spotlight as a bellwether for economic trends.

- On our framework Canadian Pacific Kansas City currently scores 4 out of 6 on the undervaluation checks, which suggests some value support but not a screaming bargain. Next, we will walk through the main valuation approaches and then finish with a more holistic way to judge what the market might really be missing.

Approach 1: Canadian Pacific Kansas City Discounted Cash Flow (DCF) Analysis

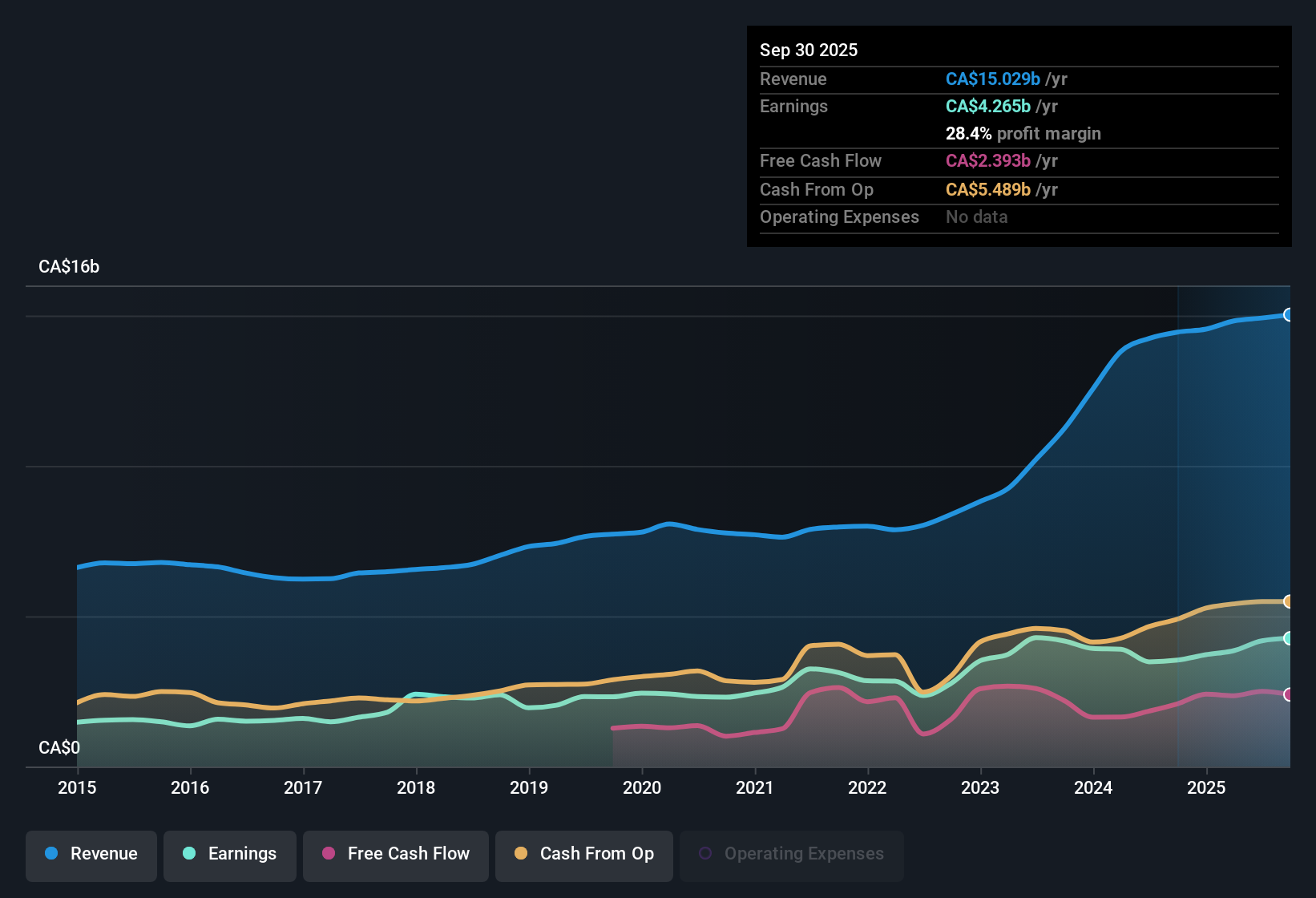

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in CA$, to reflect risk and the time value of money.

For Canadian Pacific Kansas City, the latest twelve month Free Cash Flow is about CA$2.4 billion. Analysts expect this to rise steadily, with Simply Wall St extrapolating their forecasts so that projected Free Cash Flow reaches roughly CA$7.1 billion by 2035 in a two stage Free Cash Flow to Equity model.

When all those future cash flows are discounted back to today, the model arrives at an intrinsic value of around CA$124.05 per share. That implies the shares are trading at a 16.8% discount to this estimate, which suggests the market is not fully pricing in the company’s long term cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Canadian Pacific Kansas City is undervalued by 16.8%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

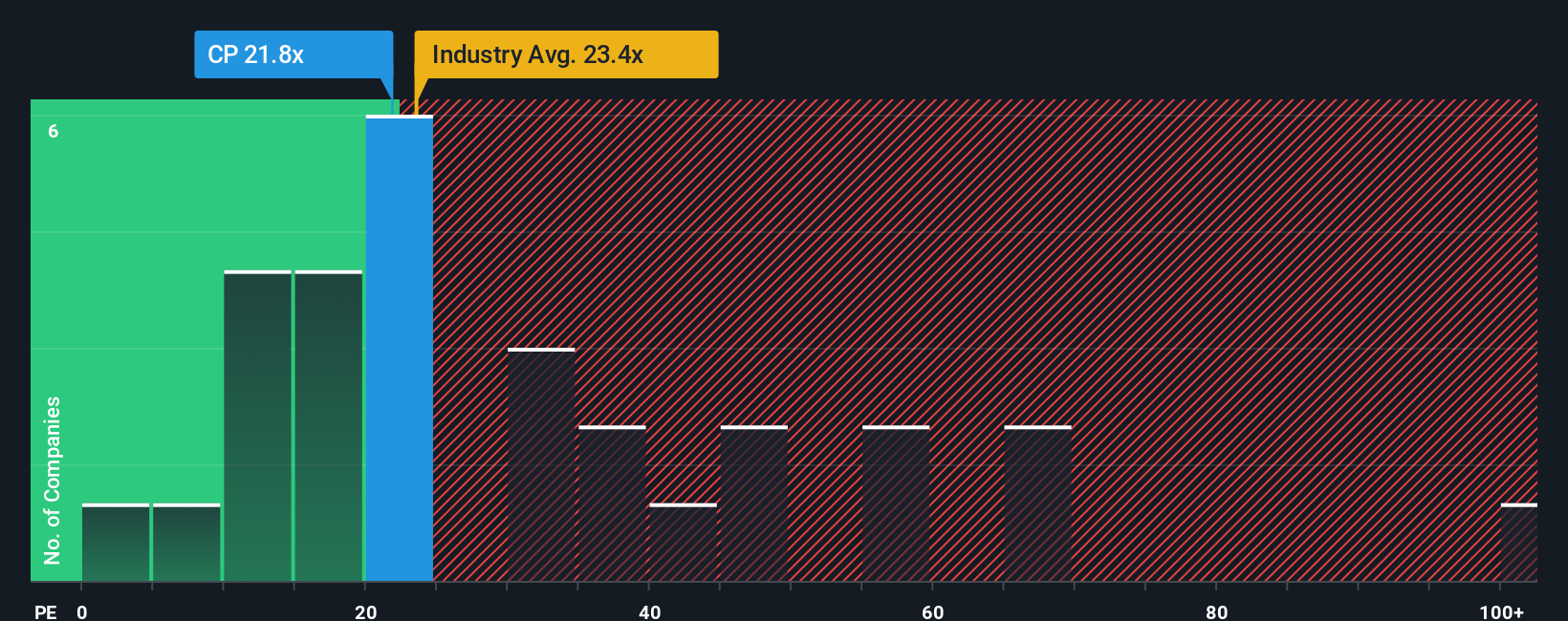

Approach 2: Canadian Pacific Kansas City Price vs Earnings

For a profitable, mature business like Canadian Pacific Kansas City, the Price to Earnings, or PE, ratio is a practical way to gauge how much investors are willing to pay for each dollar of current earnings. In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE, while slower growing or riskier businesses usually trade on lower multiples.

Canadian Pacific Kansas City currently trades on a PE of about 21.8x. That is above the broader Transportation industry average of roughly 15.2x, but very close to the 22.0x average for its direct peers. Simply Wall St also calculates a proprietary Fair Ratio of 22.0x for the company, which is the PE you might expect given its earnings growth outlook, profitability, size, industry and risk profile.

This Fair Ratio is more informative than a simple comparison with peers or the industry, because it adjusts for company specific factors rather than assuming all railroads, or all transport stocks, deserve the same multiple. Since Canadian Pacific Kansas City’s actual PE of 21.8x is almost exactly in line with the 22.0x Fair Ratio, the shares appear fairly priced on this metric.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Canadian Pacific Kansas City Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach your own story about Canadian Pacific Kansas City to the numbers behind its fair value, including your assumptions for future revenue, earnings and profit margins.

A Narrative connects three pieces together: what you believe about the company’s business story, how that belief translates into a concrete financial forecast, and finally what fair value those forecasts imply for the stock today.

On Simply Wall St, millions of investors use Narratives in the Community page as an easy, accessible tool to decide when to buy or sell by comparing the fair value implied by their Narrative to the current share price and seeing whether the gap is large enough to act on.

Because Narratives are updated dynamically as new information arrives, such as earnings results or major news about freight volumes and trade flows, your view of Canadian Pacific Kansas City can evolve in real time. One investor might, for example, see upside from stronger cross border growth, while another expects weaker margins and a lower fair value.

Do you think there's more to the story for Canadian Pacific Kansas City? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CP

Canadian Pacific Kansas City

Owns and operates a transcontinental freight railway in Canada, the United States, and Mexico.

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

43 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.7% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.6% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative