- Canada

- /

- Personal Products

- /

- TSX:JWEL

Top Three TSX Stocks Estimated To Be Undervalued In June 2024

Reviewed by Simply Wall St

Amidst a shifting economic landscape marked by moderating inflation and central bank policies, the Canadian market presents unique opportunities for investors. As the Bank of Canada embarks on a potential rate-cutting cycle, understanding which stocks are undervalued becomes particularly crucial in leveraging these evolving market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Calibre Mining (TSX:CXB) | CA$1.77 | CA$3.15 | 43.8% |

| Trisura Group (TSX:TSU) | CA$42.05 | CA$80.18 | 47.6% |

| Kinaxis (TSX:KXS) | CA$150.29 | CA$250.69 | 40% |

| Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

| Aura Minerals (TSX:ORA) | CA$12.70 | CA$21.47 | 40.9% |

| Endeavour Mining (TSX:EDV) | CA$28.29 | CA$53.97 | 47.6% |

| Green Thumb Industries (CNSX:GTII) | CA$16.06 | CA$27.21 | 41% |

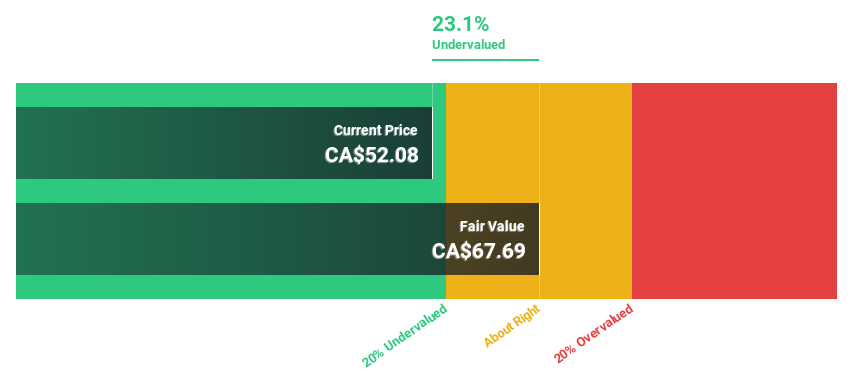

| Jamieson Wellness (TSX:JWEL) | CA$27.86 | CA$46.80 | 40.5% |

| Kits Eyecare (TSX:KITS) | CA$7.98 | CA$14.30 | 44.2% |

| Capstone Copper (TSX:CS) | CA$8.83 | CA$16.35 | 46% |

Below we spotlight a couple of our favorites from our exclusive screener

Brookfield Asset Management (TSX:BAM)

Overview: Brookfield Asset Management Ltd. is a real estate investment firm specializing in alternative asset management services, with a market capitalization of approximately CA$21.84 billion.

Operations: The firm generates revenue through its specialization in managing alternative assets.

Estimated Discount To Fair Value: 22.1%

Brookfield Asset Management's recent strategic moves, including potential acquisitions and divestitures, underscore its active management approach amidst a dynamic market. Despite trading below fair value by more than 20%, concerns about dividend coverage persist. The company's revenue and earnings growth forecasts significantly outpace the market, suggesting potential underestimation by current valuations. However, shareholder dilution within the past year raises questions about future equity value retention.

- Our growth report here indicates Brookfield Asset Management may be poised for an improving outlook.

- Click here to discover the nuances of Brookfield Asset Management with our detailed financial health report.

Jamieson Wellness (TSX:JWEL)

Overview: Jamieson Wellness Inc. operates in the health products sector, focusing on the development, manufacturing, distribution, marketing, and sale of branded and customer-branded products for humans across Canada, the United States, China, and other international markets with a market cap of approximately CA$1.14 billion.

Operations: The company generates revenue through two primary segments: Jamieson Brands, which brought in CA$558.41 million, and Strategic Partners, contributing CA$109.08 million.

Estimated Discount To Fair Value: 40.5%

Jamieson Wellness, despite a recent quarterly loss with sales dropping to CA$128.04 million from CA$136.73 million year-over-year, maintains a positive outlook for 2024 with expected revenue between CA$720.0 million and CA$760.0 million. Trading at CA$27.86, significantly below the estimated fair value of CA$46.8, the stock appears undervalued based on cash flows and DCF analysis. However, its dividend coverage by cash flow is weak, raising concerns about sustainability despite an affirmed quarterly dividend of $0.19 per share.

- Our comprehensive growth report raises the possibility that Jamieson Wellness is poised for substantial financial growth.

- Unlock comprehensive insights into our analysis of Jamieson Wellness stock in this financial health report.

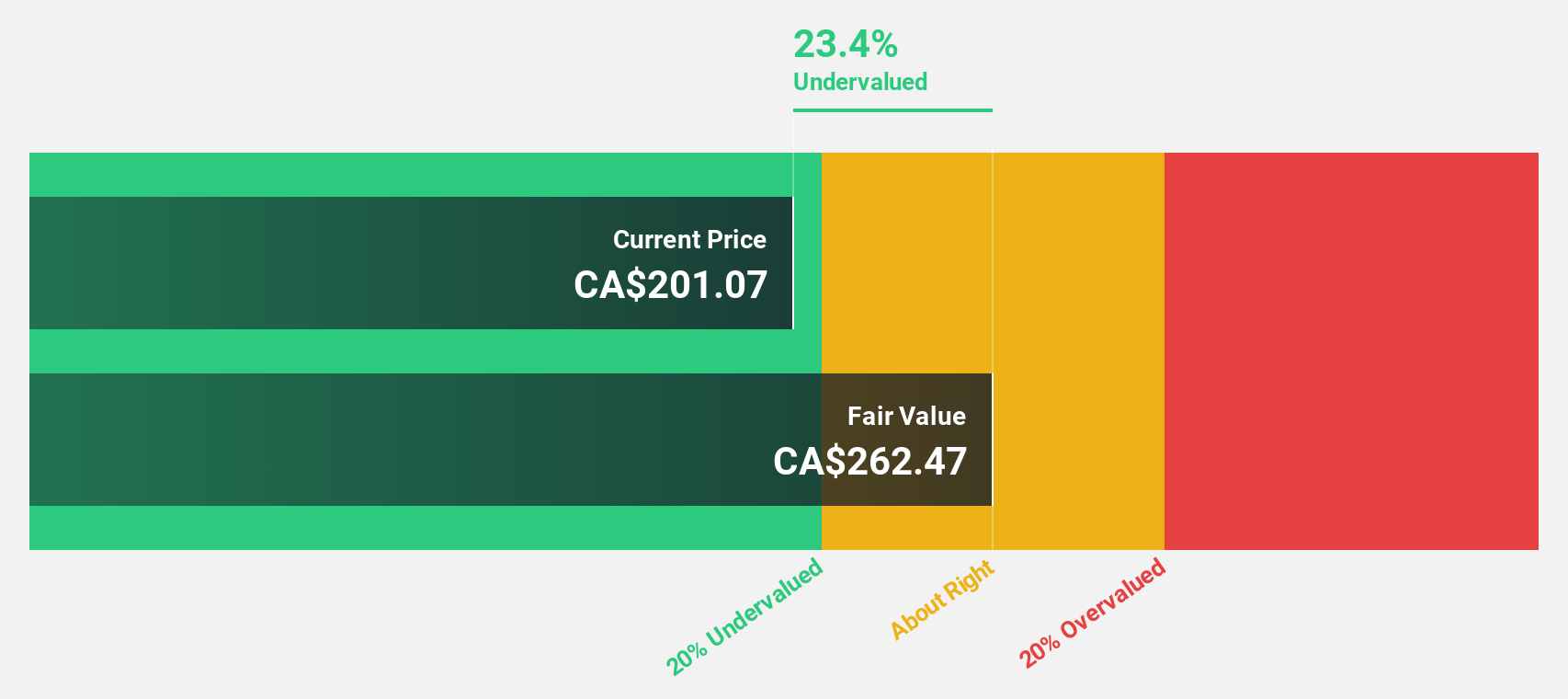

Kinaxis (TSX:KXS)

Overview: Kinaxis Inc. is a company that offers cloud-based subscription software for supply chain operations across the United States, Europe, Asia, and Canada, with a market capitalization of approximately CA$4.22 billion.

Operations: The company generates its revenue primarily from software and programming services, amounting to CA$445.21 million.

Estimated Discount To Fair Value: 40%

Kinaxis, priced at CA$150.29, is considered undervalued against a fair value of CA$250.69 based on DCF analysis. Recent client gains like Intercos and Servier underscore its robust supply chain solutions amidst volatile markets, enhancing its appeal. Despite slower revenue growth projections at 14.7% annually compared to some peers, its earnings are expected to surge by 51% annually, outpacing the Canadian market average. However, significant insider selling in the past quarter might raise caution among investors.

- The growth report we've compiled suggests that Kinaxis' future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Kinaxis.

Summing It All Up

- Click this link to deep-dive into the 23 companies within our Undervalued TSX Stocks Based On Cash Flows screener.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:JWEL

Jamieson Wellness

Develops, manufactures, distributes, markets, and sells the natural health products for human in Canada, the United States, China, and internationally.

Solid track record and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)