Advertisement

ICEsoft Technologies Canada (CSE:ISFT) Third Quarter 2024 Results

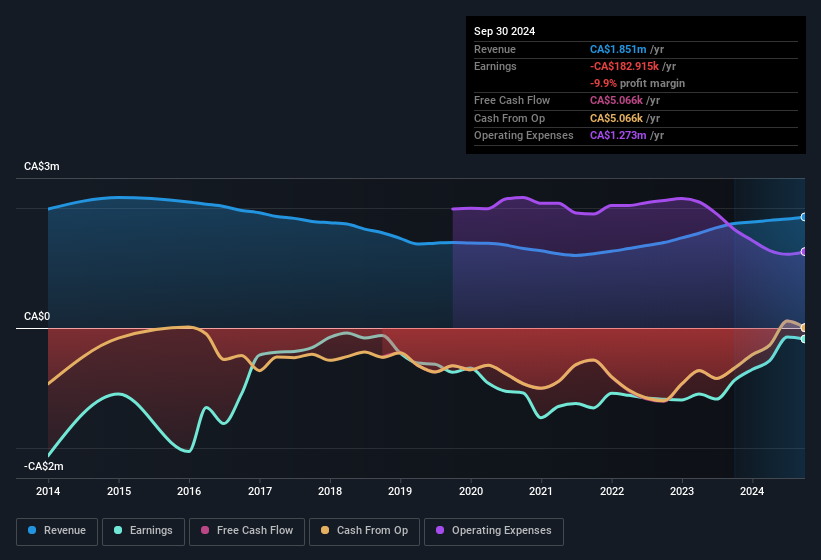

Key Financial Results

- Revenue: CA$491.3k (up 7.6% from 3Q 2023).

- Net income: CA$919 (down 97% from 3Q 2023).

- Profit margin: 0.2% (down from 7.6% in 3Q 2023). The decrease in margin was driven by higher expenses.

All figures shown in the chart above are for the trailing 12 month (TTM) period

ICEsoft Technologies Canada's share price is broadly unchanged from a week ago.

Risk Analysis

You should always think about risks. Case in point, we've spotted 4 warning signs for ICEsoft Technologies Canada you should be aware of, and 3 of them are concerning.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CNSX:ISFT

ICEsoft Technologies Canada

Provides community alerting and engagement, and enterprise middleware solutions for desktop and mobile enterprises in Canada, Europe, the United States, and internationally.

Moderate risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This Gold Stock Could Triple if Its Gold Resource Grows

Fair Value:CA$466.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9720.3% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.6% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$23.861.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Hektar Real Estate Investment Trust ·

Hektar REIT: Deep Value, Attractive Yield, and a Portfolio Transformation Story in the Making

Fair Value:RM 156.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on CSG ·

CSG represents a high-quality industrial compounder operating in a structurally growing and geopolitically reinforced market,

Fair Value:€3037.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

artoflosing on BlackBerry ·

Accidental transformation from Phones to Physical AI.

Fair Value:CA$16.2228.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.1% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6120.0% undervalued

1192 followersusers have followed this narrative

7 commentsusers have commented on this narrative

35 likesusers have liked this narrative