Advertisement

- Canada

- /

- Specialty Stores

- /

- TSX:LNF

Do Its Financials Have Any Role To Play In Driving Leon's Furniture Limited's (TSE:LNF) Stock Up Recently?

Leon's Furniture (TSE:LNF) has had a great run on the share market with its stock up by a significant 19% over the last month. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. In this article, we decided to focus on Leon's Furniture's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

We've discovered 2 warning signs about Leon's Furniture. View them for free.How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Leon's Furniture is:

14% = CA$159m ÷ CA$1.2b (Based on the trailing twelve months to March 2025).

The 'return' is the yearly profit. Another way to think of that is that for every CA$1 worth of equity, the company was able to earn CA$0.14 in profit.

See our latest analysis for Leon's Furniture

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Leon's Furniture's Earnings Growth And 14% ROE

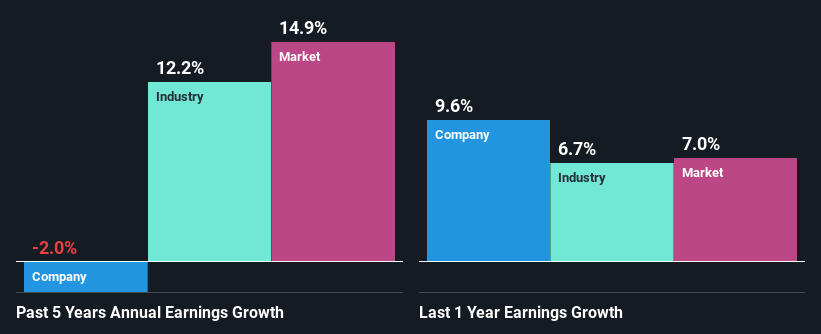

At first glance, Leon's Furniture seems to have a decent ROE. Even when compared to the industry average of 12% the company's ROE looks quite decent. As you might expect, the 2.0% net income decline reported by Leon's Furniture is a bit of a surprise. So, there might be some other aspects that could explain this. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for instance.

That being said, we compared Leon's Furniture's performance with the industry and were concerned when we found that while the company has shrunk its earnings, the industry has grown its earnings at a rate of 12% in the same 5-year period.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. Is Leon's Furniture fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Leon's Furniture Making Efficient Use Of Its Profits?

In spite of a normal three-year median payout ratio of 32% (that is, a retention ratio of 68%), the fact that Leon's Furniture's earnings have shrunk is quite puzzling. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

Moreover, Leon's Furniture has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Our latest analyst data shows that the future payout ratio of the company is expected to rise to 40% over the next three years.

Conclusion

On the whole, we do feel that Leon's Furniture has some positive attributes. However, given the high ROE and high profit retention, we would expect the company to be delivering strong earnings growth, but that isn't the case here. This suggests that there might be some external threat to the business, that's hampering its growth. That being so, the latest industry analyst forecasts show that analysts are forecasting a slight improvement in the company's future earnings growth. The company's existing shareholders might have some respite after all. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:LNF

Leon's Furniture

Operates as a retailer of home furnishings, mattresses, appliances, and electronics in Canada.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor