- Canada

- /

- Specialty Stores

- /

- TSX:GRGD

3 TSX Stocks Estimated To Be Trading At Discounts Of Up To 49.7%

Reviewed by Simply Wall St

As the Canadian economy navigates a period of rising inflation and anticipated interest rate cuts by the Bank of Canada, investors are keeping a close eye on potential opportunities within the market. In this environment, identifying undervalued stocks can be particularly appealing, as these equities may offer substantial upside potential when market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Savaria (TSX:SIS) | CA$17.05 | CA$30.34 | 43.8% |

| Docebo (TSX:DCBO) | CA$44.64 | CA$84.75 | 47.3% |

| K92 Mining (TSX:KNT) | CA$12.06 | CA$19.76 | 39% |

| Thunderbird Entertainment Group (TSXV:TBRD) | CA$1.67 | CA$3.25 | 48.7% |

| Lithium Royalty (TSX:LIRC) | CA$4.89 | CA$9.15 | 46.6% |

| Groupe Dynamite (TSX:GRGD) | CA$14.75 | CA$27.24 | 45.8% |

| Tourmaline Oil (TSX:TOU) | CA$68.70 | CA$136.58 | 49.7% |

| Kits Eyecare (TSX:KITS) | CA$12.35 | CA$24.49 | 49.6% |

| Aya Gold & Silver (TSX:AYA) | CA$12.91 | CA$24.91 | 48.2% |

| CAE (TSX:CAE) | CA$36.48 | CA$60.63 | 39.8% |

Underneath we present a selection of stocks filtered out by our screen.

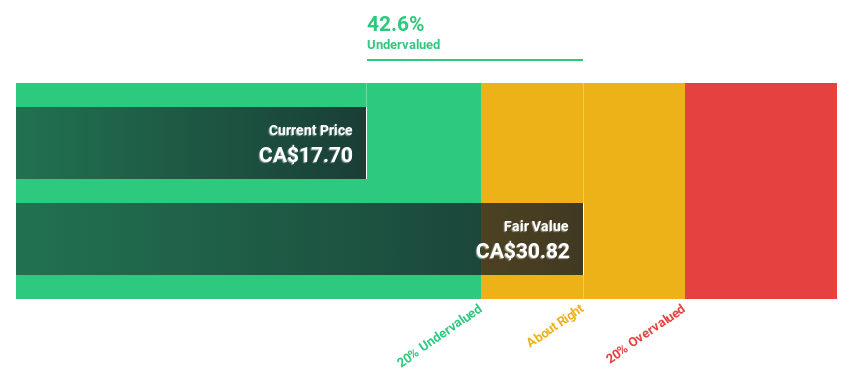

Groupe Dynamite (TSX:GRGD)

Overview: Groupe Dynamite Inc. operates fashion retail stores in North America and has a market cap of CA$1.46 billion.

Operations: The company's revenue from apparel amounts to CA$927.05 million.

Estimated Discount To Fair Value: 45.8%

Groupe Dynamite is trading at CA$14.75, significantly below its estimated fair value of CA$27.24, indicating it may be undervalued based on cash flows. Despite a high level of debt, the company's earnings are forecast to grow at 16.6% annually, outpacing the Canadian market's average growth rate. Analysts agree on a potential stock price increase of 76.6%, supported by past earnings growth of 66.5% and strong future revenue projections.

- According our earnings growth report, there's an indication that Groupe Dynamite might be ready to expand.

- Click here to discover the nuances of Groupe Dynamite with our detailed financial health report.

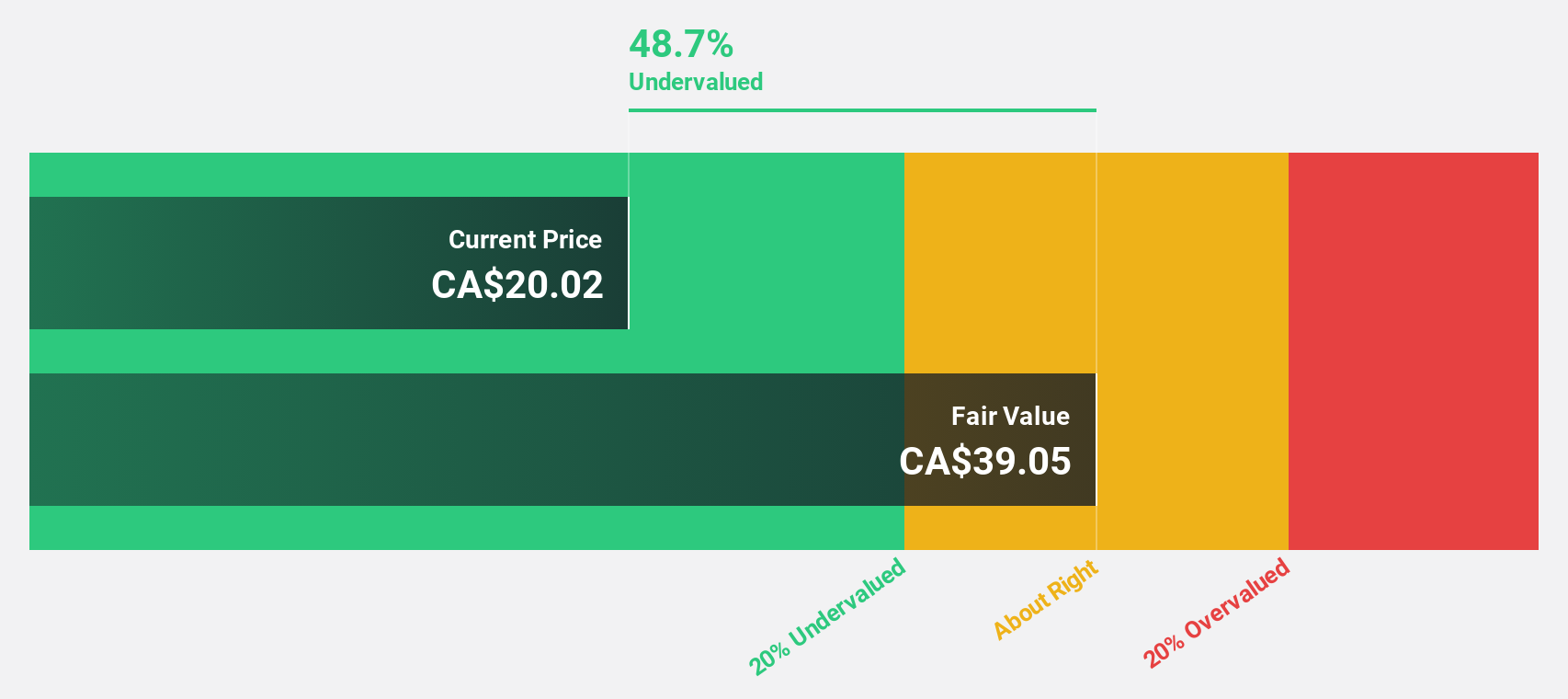

Kits Eyecare (TSX:KITS)

Overview: Kits Eyecare Ltd. operates a digital eyecare platform in the United States and Canada, with a market cap of CA$374.19 million.

Operations: The company generates revenue of CA$159.34 million from the sale of eyewear products across its digital platform in the United States and Canada.

Estimated Discount To Fair Value: 49.6%

Kits Eyecare, trading at CA$12.35, is valued significantly below its estimated fair value of CA$24.49. The company's earnings are expected to grow substantially at 49.5% per year, outpacing the Canadian market's average growth rate. Recent innovations include launching integrated vision care insurance support in the U.S., enhancing customer experience and potentially driving future revenue growth, which is projected to increase by 17.6% annually, faster than the broader Canadian market.

- Upon reviewing our latest growth report, Kits Eyecare's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Kits Eyecare.

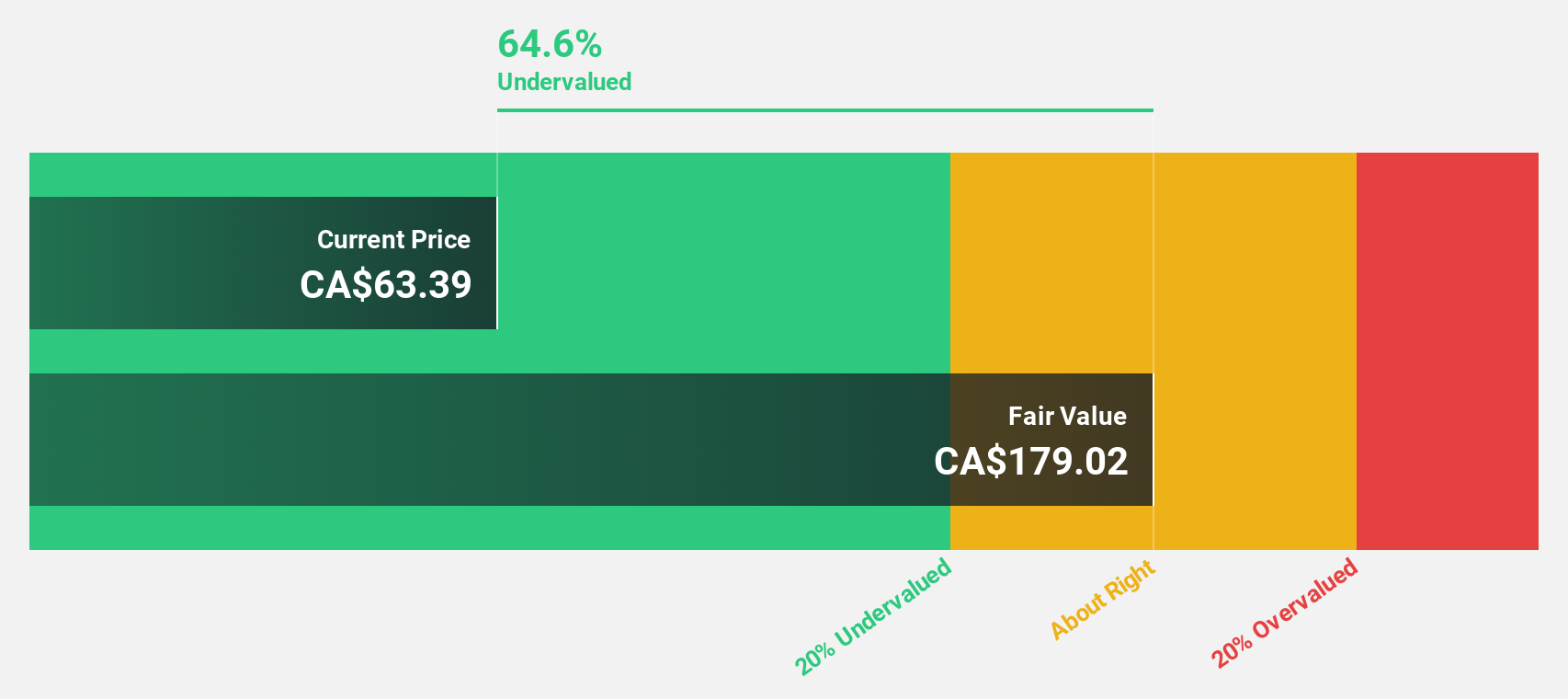

Tourmaline Oil (TSX:TOU)

Overview: Tourmaline Oil Corp. is involved in the acquisition, exploration, development, and production of petroleum and natural gas properties in the Western Canadian Sedimentary Basin, with a market cap of CA$25.82 billion.

Operations: The company's revenue is primarily derived from its petroleum and natural gas properties, totaling CA$4.84 billion.

Estimated Discount To Fair Value: 49.7%

Tourmaline Oil, trading at CA$68.7, is significantly undervalued compared to its estimated fair value of CA$136.58. Despite a recent decline in net income to CA$1.26 billion from the previous year, the company's revenue and earnings are forecasted to grow over 24% annually, surpassing the Canadian market average. However, its dividend yield of 5.6% isn't well covered by free cash flows, highlighting potential sustainability concerns despite robust production growth projections for 2025.

- The growth report we've compiled suggests that Tourmaline Oil's future prospects could be on the up.

- Dive into the specifics of Tourmaline Oil here with our thorough financial health report.

Make It Happen

- Discover the full array of 22 Undervalued TSX Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Groupe Dynamite, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:GRGD

Groupe Dynamite

Designs, distributes, and sells women’s apparel in the market of Canada and the United States of America.

Outstanding track record and undervalued.

Market Insights

Community Narratives