- Canada

- /

- Retail REITs

- /

- TSX:CRR.UN

Investing in Crombie Real Estate Investment Trust (TSE:CRR.UN) five years ago would have delivered you a 58% gain

Crombie Real Estate Investment Trust (TSE:CRR.UN) shareholders might be concerned after seeing the share price drop 10% in the last quarter. But the silver lining is the stock is up over five years. Unfortunately its return of 16% is below the market return of 49%. Unfortunately not all shareholders will have held it for the long term, so spare a thought for those caught in the 16% decline over the last twelve months.

So let's investigate and see if the longer term performance of the company has been in line with the underlying business' progress.

Though if you're not interested in researching what drove CRR.UN's performance, we have a free list of interesting investing ideas to potentially inspire your next investment!

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

During five years of share price growth, Crombie Real Estate Investment Trust actually saw its EPS drop 5.1% per year.

Since the EPS are down strongly, it seems highly unlikely market participants are looking at EPS to value the company. Given that EPS is down, but the share price is up, it seems clear the market is focussed on other aspects of the business, at the moment.

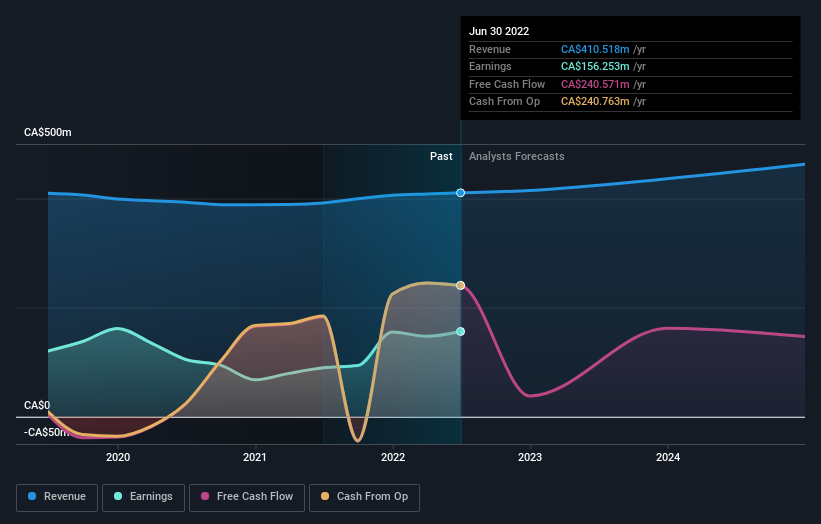

There's no sign of growing dividends, which might have explained the resilient share price. We doubt the diminishing revenue (at 0.9% per year) encouraged buyers. But a closer look at the history of earnings and revenue might give clues as to why the share price is up.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. You can see what analysts are predicting for Crombie Real Estate Investment Trust in this interactive graph of future profit estimates.

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. In the case of Crombie Real Estate Investment Trust, it has a TSR of 58% for the last 5 years. That exceeds its share price return that we previously mentioned. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

We regret to report that Crombie Real Estate Investment Trust shareholders are down 11% for the year (even including dividends). Unfortunately, that's worse than the broader market decline of 2.1%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Longer term investors wouldn't be so upset, since they would have made 10%, each year, over five years. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Like risks, for instance. Every company has them, and we've spotted 4 warning signs for Crombie Real Estate Investment Trust (of which 2 make us uncomfortable!) you should know about.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

If you're looking to trade Crombie Real Estate Investment Trust, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:CRR.UN

Crombie Real Estate Investment Trust

Crombie invests in real estate that enriches local communities and enables long-term sustainable growth.

Proven track record average dividend payer.