Advertisement

Auditors Are Concerned About Green Organic Dutchman Holdings (TSE:TGOD)

When The Green Organic Dutchman Holdings Ltd. (TSE:TGOD) reported its results to December 2020 its auditors, KPMG LLP - Klynveld Peat Marwick Goerdeler could not be sure that it would be able to continue as a going concern in the next year. This means that, based on the financial results to that date, the company arguably should raise capital, or otherwise strengthen the balance sheet, as soon as possible.

Given its situation, it may not be in a good position to raise capital on favorable terms. So shareholders should absolutely be taking a close look at how risky the balance sheet is. Debt is always a risk factor in these cases, as creditors could be in a position to wind up the company, in the worst case scenario.

View our latest analysis for Green Organic Dutchman Holdings

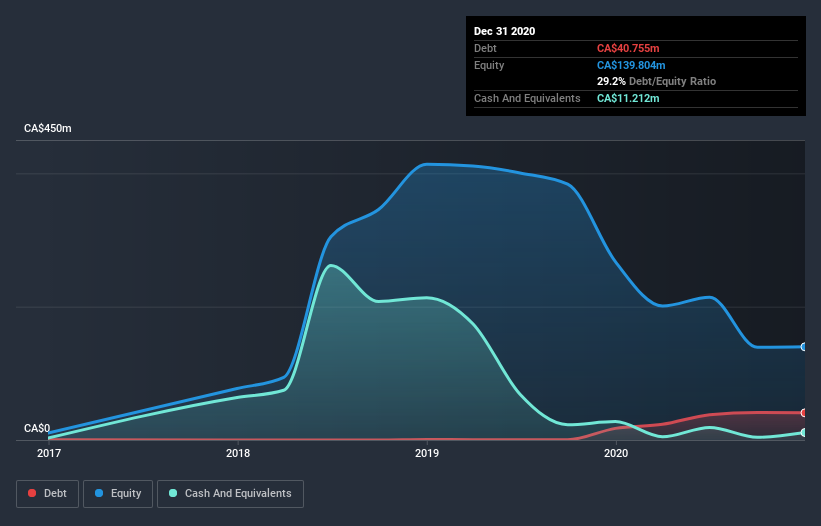

How Much Debt Does Green Organic Dutchman Holdings Carry?

The image below, which you can click on for greater detail, shows that at December 2020 Green Organic Dutchman Holdings had debt of CA$40.8m, up from CA$17.4m in one year. On the flip side, it has CA$11.2m in cash leading to net debt of about CA$29.5m.

How Healthy Is Green Organic Dutchman Holdings' Balance Sheet?

We can see from the most recent balance sheet that Green Organic Dutchman Holdings had liabilities of CA$66.4m falling due within a year, and liabilities of CA$5.39m due beyond that. Offsetting this, it had CA$11.2m in cash and CA$10.2m in receivables that were due within 12 months. So it has liabilities totalling CA$50.4m more than its cash and near-term receivables, combined.

Green Organic Dutchman Holdings has a market capitalization of CA$184.5m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Green Organic Dutchman Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Green Organic Dutchman Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 96%, to CA$21m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Even though Green Organic Dutchman Holdings managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Indeed, it lost a very considerable CA$44m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled CA$87m in negative free cash flow over the last twelve months. So in short it's a really risky stock. We're too cautious to want to invest in a company after an auditor has expressed doubts about its ability to continue as a going concern. That's because companies should always make sure the auditor has confidence that the company will continue as a going concern, in our view. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for Green Organic Dutchman Holdings (2 are a bit unpleasant!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Green Organic Dutchman Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BZAM might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CNSX:BZAM

BZAM

Operates as a cannabis producer with a focus on branded consumer goods.

Slight with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor