Market Cool On Numinus Wellness Inc.'s (TSE:NUMI) Revenues Pushing Shares 30% Lower

To the annoyance of some shareholders, Numinus Wellness Inc. (TSE:NUMI) shares are down a considerable 30% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 63% loss during that time.

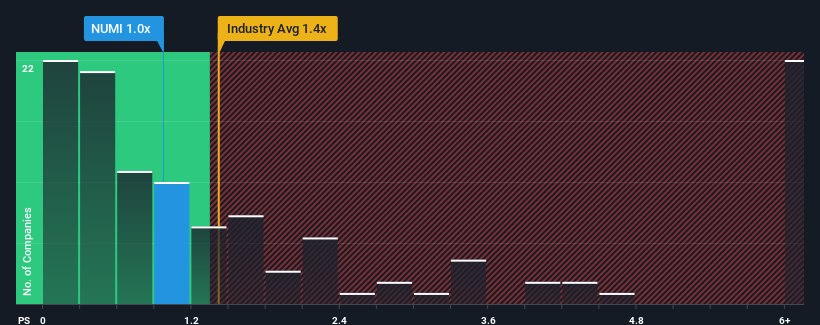

Even after such a large drop in price, you could still be forgiven for feeling indifferent about Numinus Wellness' P/S ratio of 1x, since the median price-to-sales (or "P/S") ratio for the Pharmaceuticals industry in Canada is also close to 1.4x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Numinus Wellness

How Numinus Wellness Has Been Performing

Recent times have been advantageous for Numinus Wellness as its revenues have been rising faster than most other companies. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Keen to find out how analysts think Numinus Wellness' future stacks up against the industry? In that case, our free report is a great place to start.How Is Numinus Wellness' Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Numinus Wellness' is when the company's growth is tracking the industry closely.

If we review the last year of revenue growth, the company posted a terrific increase of 45%. This great performance means it was also able to deliver immense revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 45% each year over the next three years. With the industry only predicted to deliver 8.1% per year, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that Numinus Wellness' P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Key Takeaway

Numinus Wellness' plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Despite enticing revenue growth figures that outpace the industry, Numinus Wellness' P/S isn't quite what we'd expect. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Numinus Wellness (at least 1 which is a bit unpleasant), and understanding them should be part of your investment process.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Numinus Wellness might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:NUMI

Numinus Wellness

Provides psychedelic-assisted psychotherapy products and services in Canada and the United States.

High growth potential slight.