Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Focus Graphite Inc. (CVE:FMS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Our analysis indicates that FMS is potentially overvalued!

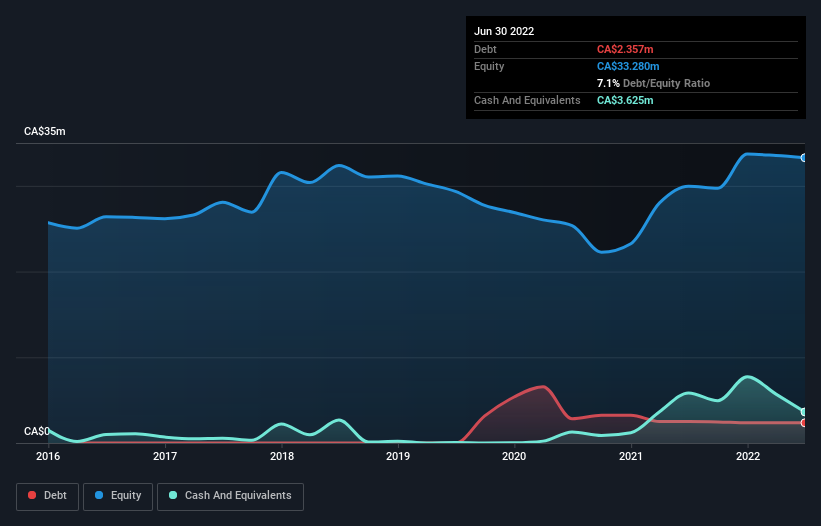

How Much Debt Does Focus Graphite Carry?

The image below, which you can click on for greater detail, shows that Focus Graphite had debt of CA$2.36m at the end of June 2022, a reduction from CA$2.51m over a year. However, its balance sheet shows it holds CA$3.63m in cash, so it actually has CA$1.27m net cash.

How Healthy Is Focus Graphite's Balance Sheet?

According to the last reported balance sheet, Focus Graphite had liabilities of CA$7.61m due within 12 months, and liabilities of CA$58.9k due beyond 12 months. Offsetting these obligations, it had cash of CA$3.63m as well as receivables valued at CA$2.03m due within 12 months. So its liabilities total CA$2.02m more than the combination of its cash and short-term receivables.

Of course, Focus Graphite has a market capitalization of CA$23.1m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Focus Graphite also has more cash than debt, so we're pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Focus Graphite's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Given its lack of meaningful operating revenue, investors are probably hoping that Focus Graphite finds some valuable resources, before it runs out of money.

So How Risky Is Focus Graphite?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Focus Graphite had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of CA$6.7m and booked a CA$6.5m accounting loss. Given it only has net cash of CA$1.27m, the company may need to raise more capital if it doesn't reach break-even soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 6 warning signs we've spotted with Focus Graphite (including 4 which make us uncomfortable) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:FMS

Focus Graphite

An exploration stage company, acquires, explores, and develops mineral properties in Quebec, Canada.

Medium-low risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor