Shifts in investor sentiment toward small-cap stocks in the Canadian market are not uncommon and can be influenced by a variety of factors such as changes in economic conditions, market dynamics, and investor preferences. These shifts underscore the importance of identifying undervalued small caps that demonstrate strong insider buying as potential opportunities for informed investors.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Martinrea International | 6.2x | 0.2x | 44.39% | ★★★★★★ |

| Dundee Precious Metals | 8.6x | 3.0x | 42.30% | ★★★★★★ |

| CI Financial | NA | 0.7x | 32.17% | ★★★★★★ |

| Guardian Capital Group | 10.5x | 4.1x | 32.28% | ★★★★★☆ |

| Calfrac Well Services | 2.2x | 0.2x | 2.05% | ★★★★★☆ |

| Primaris Real Estate Investment Trust | 11.4x | 3.0x | 35.88% | ★★★★★☆ |

| Rogers Sugar | 13.8x | 0.6x | 40.61% | ★★★★☆☆ |

| Gear Energy | 19.8x | 1.4x | 28.20% | ★★★★☆☆ |

| Nexus Industrial REIT | 2.4x | 3.0x | 18.54% | ★★★★☆☆ |

| Freehold Royalties | 15.5x | 6.7x | 46.90% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

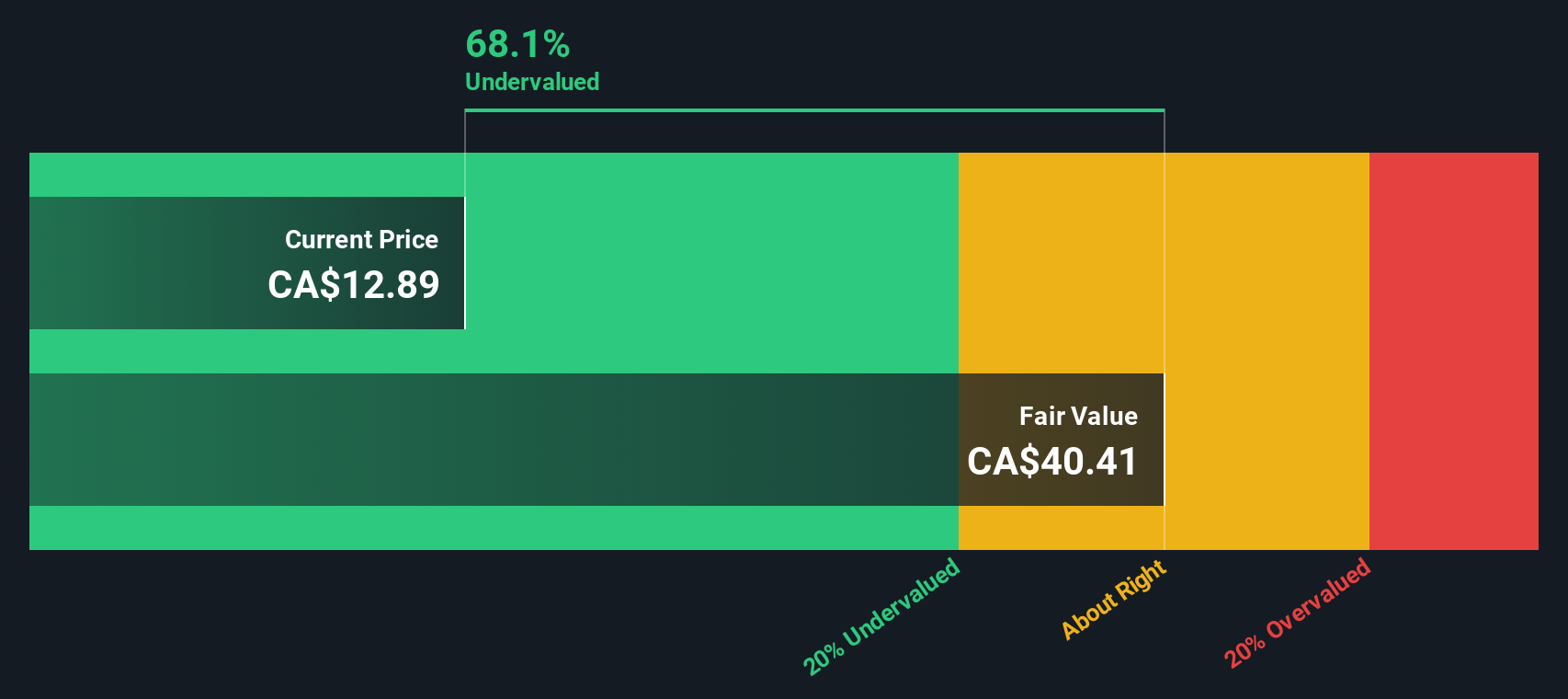

Freehold Royalties (FRU)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Freehold Royalties is a company that focuses on oil and gas exploration and production, with a market capitalization of approximately CA$1.63 billion.

Operations: The company operates in the oil and gas exploration and production sector, generating CA$312.28 million in revenue with a gross profit margin of 96.74%. Its net income for the latest reported period stands at CA$134.87 million, reflecting a net income margin of 43.19%.

PE: 15.5x

Recently, David Spyker demonstrated confidence in Freehold Royalties by acquiring 20,000 shares for CA$276,000. This insider activity underscores a strong belief in the company's prospects amidst its consistent financial performance. In the first quarter of 2024, Freehold reported a net income increase to CA$34 million from CA$31 million year-over-year and maintained steady production levels. Moreover, the firm has reaffirmed its annual production forecast, signaling stable future operations. These factors make Freehold an intriguing consideration within Canada's underappreciated investment opportunities.

- Click here to discover the nuances of Freehold Royalties with our detailed analytical valuation report.

-

Evaluate Freehold Royalties' historical performance by accessing our past performance report.

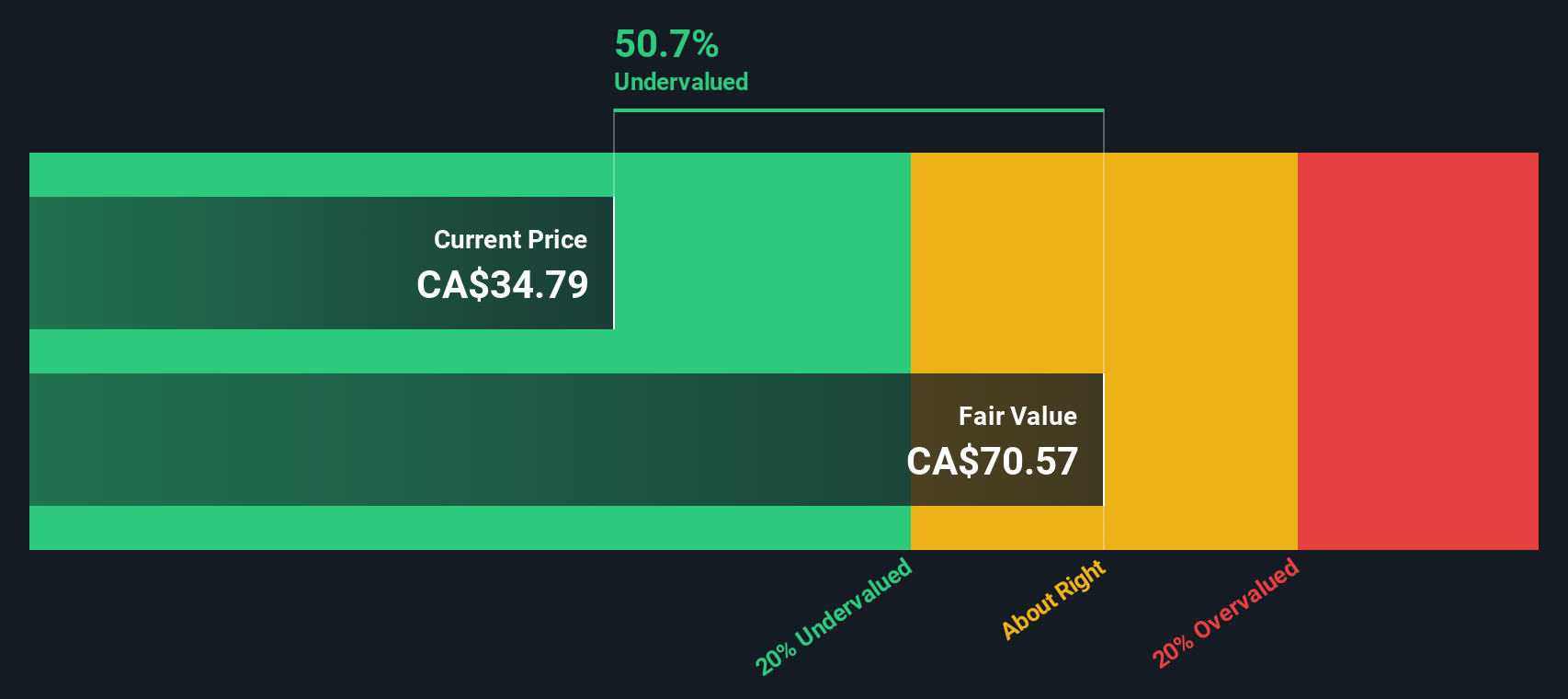

Jamieson Wellness (JWEL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Jamieson Wellness is a company that specializes in the manufacture and distribution of natural health products, operating primarily through its Jamieson Brands and Strategic Partners segments.

Operations: The company generates revenue primarily through its Jamieson Brands and Strategic Partners segments, contributing CA$558.41 million and CA$109.08 million respectively. Over recent periods, it has experienced a gross profit margin fluctuation, peaking at 0.37% in the second quarter of 2022 before slightly decreasing to 0.35% by mid-2023.

PE: 30.6x

Recently, Timothy Penner demonstrated confidence in Jamieson Wellness by purchasing 11,000 shares for CA$298,496. This move aligns with the company's robust sales growth forecast of up to 12.5% for 2024, despite a dip in profit margins from last year. The firm continues to pay dividends, with CA$8 million distributed this quarter, underscoring its commitment to shareholder returns even as it navigates a challenging financial landscape marked by higher external borrowing and a recent labor agreement that promises significant wage increases.

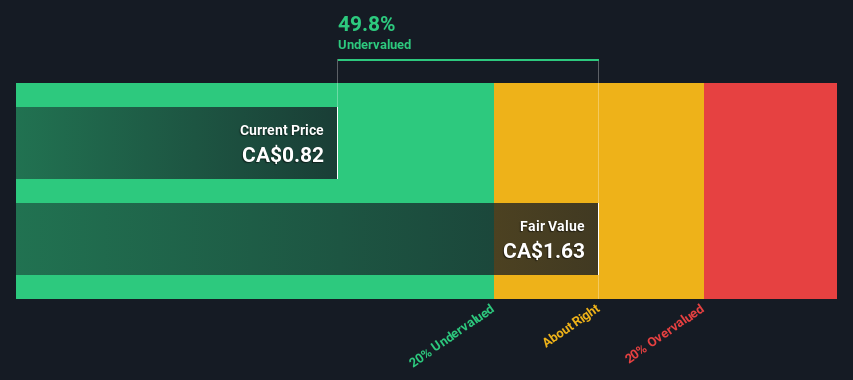

Queen's Road Capital Investment (QRC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Queen's Road Capital Investment primarily focuses on the selection, acquisition, and management of investments.

Operations: The entity generates revenue through the selection, acquisition, and management of investments, achieving a gross profit margin of 100% in recent periods. Notably, net income has shown significant fluctuations with a notable increase to $69.34 million as per the latest data.

PE: 4.2x

Recently, Queen's Road Capital Investment showcased a significant turnaround in its financial performance. For the first half of 2024, the company reported a net income of US$47.89 million, rebounding from a net loss the previous year. This improvement is underscored by an impressive revenue increase to US$50.04 million from previously negative figures. Such positive earnings reflect not only recovery but also potential underappreciated market value, particularly interesting given that all liabilities are managed through higher-risk external borrowings—indicating no reliance on customer deposits. This financial maneuvering suggests strategic agility in capital management, aligning with insider confidence as they have recently increased their stakes, signaling strong belief in future growth prospects.

Seize The Opportunity

- Get an in-depth perspective on all 38 Undervalued TSX Small Caps With Insider Buying by using our screener here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Queen's Road Capital Investment, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Queen's Road Capital Investment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:QRC

Queen's Road Capital Investment

A resource focused investment company, invests in privately held and publicly traded resource companies.

Fair value with mediocre balance sheet.

Market Insights

Community Narratives