- Canada

- /

- Metals and Mining

- /

- TSX:K

Kinross Gold (TSX:K) Valuation Check After 180% One-Year Surge and Recent Share Price Strength

Reviewed by Simply Wall St

Kinross Gold (TSX:K) has quietly turned into one of the stronger performers on the TSX, with the stock up about 20% in the past 3 months and nearly 180% over the past year.

See our latest analysis for Kinross Gold.

After a strong run, the current CA$38.46 share price reflects both Kinross Gold’s recent operational progress and a reset in risk perception, with the 1 year total shareholder return signaling that momentum is still firmly on its side.

If Kinross has you rethinking your playbook, it might be worth exploring other resource heavyweights and discovering fast growing stocks with high insider ownership as potential candidates for the next leg of your portfolio’s growth.

With earnings still growing, a modest upside to analyst targets, and gold prices supporting cash flows, investors now face a key question: is Kinross still trading below its long term potential, or has the market already priced in its next chapter of growth?

Most Popular Narrative: 30% Overvalued

With Kinross Gold closing at CA$38.46 versus a most popular narrative fair value near CA$38.33, the story leans toward a slightly stretched valuation built on resilient margins and tempered growth assumptions.

The fair value estimate has risen slightly to approximately 38.33 dollars from about 37.79 dollars, reflecting a modestly higher intrinsic value assessment. The future P/E has edged higher to about 16.3x from roughly 16.0x, suggesting a small upward shift in the valuation multiple applied to projected earnings.

Want to see why modest revenue growth, thicker margins, and a tweaked discount rate can still argue for a rich earnings multiple? The narrative walks through how steady production, disciplined buybacks, and long dated project optionality are blended into one valuation blueprint, and which cash flow assumptions end up doing the real heavy lifting.

Result: Fair Value of $38.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising operating costs and ongoing permitting or regulatory delays across key jurisdictions could quickly erode margins and challenge today’s optimistic valuation narrative.

Find out about the key risks to this Kinross Gold narrative.

Another View: Market Comparisons Paint A Milder Picture

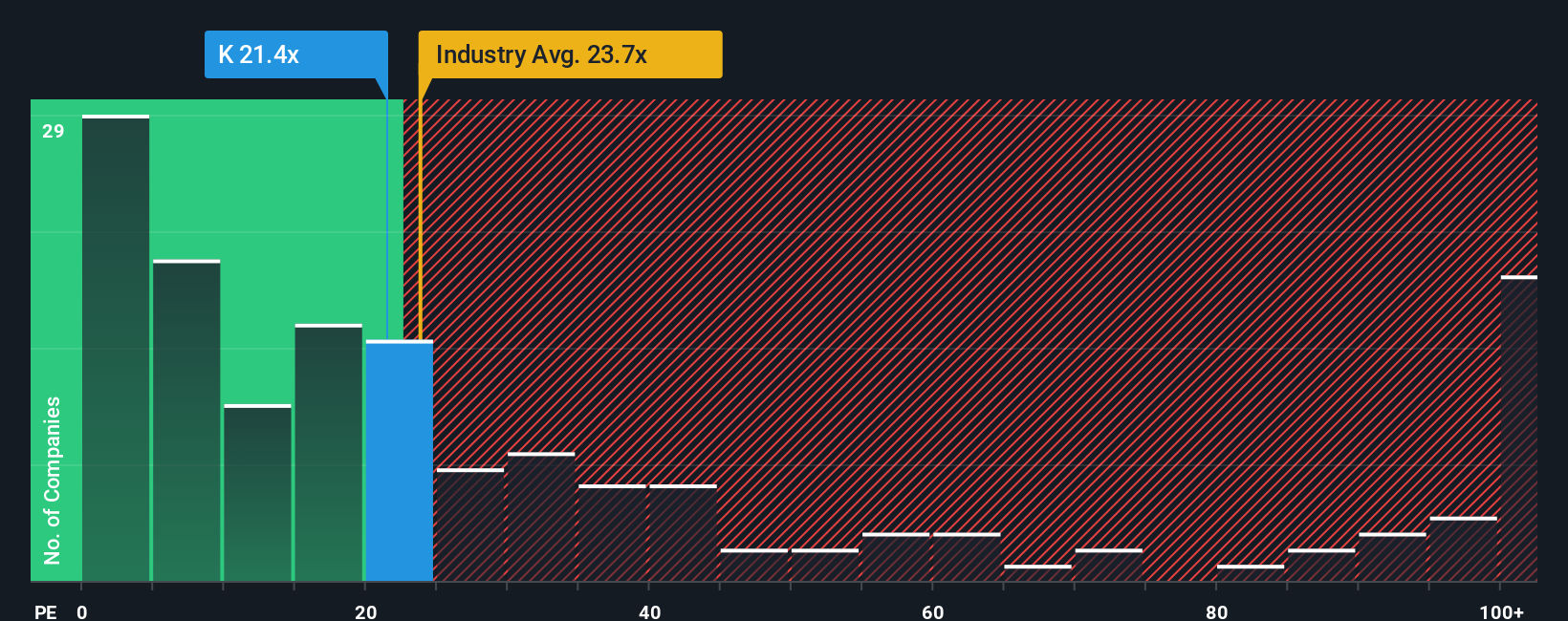

While the narrative model flags Kinross as about 30% overvalued, its 19.2x price to earnings ratio sits below the metals and mining industry at 21.5x and close to a 19.6x fair ratio. That suggests valuation risk may be more contained than the headline implies. Or does it?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Kinross Gold Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Kinross Gold.

Looking for more investment ideas?

Do not stop at one winning story when you can quickly scan a world of opportunities tailored to your style, risk appetite, and return goals.

- Capture mispriced opportunities by targeting these 904 undervalued stocks based on cash flows that may offer stronger upside than mature large caps.

- Position ahead of the next tech inflection by filtering for these 26 AI penny stocks riding structural demand for intelligent software and automation.

- Strengthen your income stream by focusing on these 13 dividend stocks with yields > 3% that can complement growth names like Kinross.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kinross Gold might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:K

Kinross Gold

Engages in the acquisition, exploration, and development of gold properties principally in the United States, Brazil, Chile, Canada, and Mauritania.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)