Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:AII

TSX Growth Stocks With High Insider Ownership Include Almonty Industries And Two Others

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates the complexities of trade tariffs and inflationary pressures, investors are encouraged to maintain a diversified portfolio, especially as recent performance has shown resilience with indices like the TSX rising over 5% in May. In such an environment, growth companies with high insider ownership can be particularly appealing, as they often demonstrate strong management commitment and potential for long-term value creation.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Propel Holdings (TSX:PRL) | 36.5% | 33% |

| Robex Resources (TSXV:RBX) | 16.8% | 174% |

| Almonty Industries (TSX:AII) | 12% | 55.8% |

| goeasy (TSX:GSY) | 21.9% | 18.2% |

| Aritzia (TSX:ATZ) | 17.5% | 24.7% |

| Enterprise Group (TSX:E) | 32.2% | 24.8% |

| Discovery Silver (TSX:DSV) | 17.5% | 39.4% |

| Ivanhoe Mines (TSX:IVN) | 12.4% | 28.6% |

| Allied Gold (TSX:AAUC) | 15% | 80% |

| Tenaz Energy (TSX:TNZ) | 10.4% | 151.2% |

Let's explore several standout options from the results in the screener.

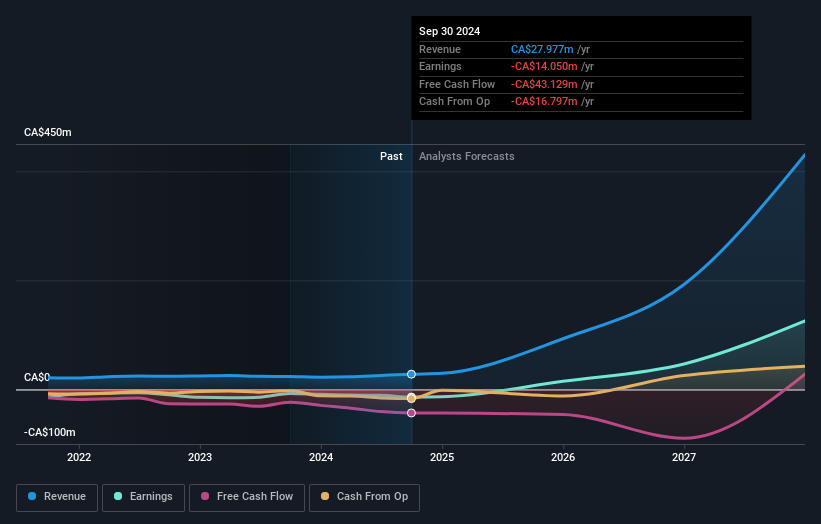

Almonty Industries (TSX:AII)

Simply Wall St Growth Rating: ★★★★★★

Overview: Almonty Industries Inc. is involved in the mining, processing, and shipping of tungsten concentrate, with a market cap of CA$754.43 million.

Operations: The company's revenue is primarily derived from its Panasqueira segment, amounting to CA$28.88 million.

Insider Ownership: 12%

Almonty Industries, a Canadian growth company with high insider ownership, is strategically positioning itself in the critical metals sector through partnerships and board appointments. Recent additions to its board include Alan Estevez and General Gustave Perna, both bringing substantial defense and logistics expertise. Despite reporting a significant net loss of C$34.62 million for Q1 2025, Almonty's revenue is forecasted to grow rapidly at 45% annually. The company's insider buying activity suggests confidence in its future prospects amidst volatile share prices.

- Click here to discover the nuances of Almonty Industries with our detailed analytical future growth report.

- The valuation report we've compiled suggests that Almonty Industries' current price could be quite moderate.

Maple Leaf Foods (TSX:MFI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Maple Leaf Foods Inc., along with its subsidiaries, produces food products across Canada, the United States, Japan, China, and other international markets with a market cap of CA$3.39 billion.

Operations: Maple Leaf Foods generates revenue from producing food products across Canada, the United States, Japan, China, and other international markets.

Insider Ownership: 39.9%

Maple Leaf Foods, with significant insider ownership, is experiencing a transformative phase. Despite recent impairment charges of C$866,000, the company has become profitable and forecasts earnings growth of 46.4% annually—outpacing the Canadian market. Analysts project a 20.1% stock price increase as it trades below fair value estimates. While insiders have shown modest buying activity recently, Maple Leaf's strategic share repurchase plan and increased dividend to C$0.96 annually reflect strong shareholder commitment amid moderate revenue growth expectations.

- Take a closer look at Maple Leaf Foods' potential here in our earnings growth report.

- According our valuation report, there's an indication that Maple Leaf Foods' share price might be on the cheaper side.

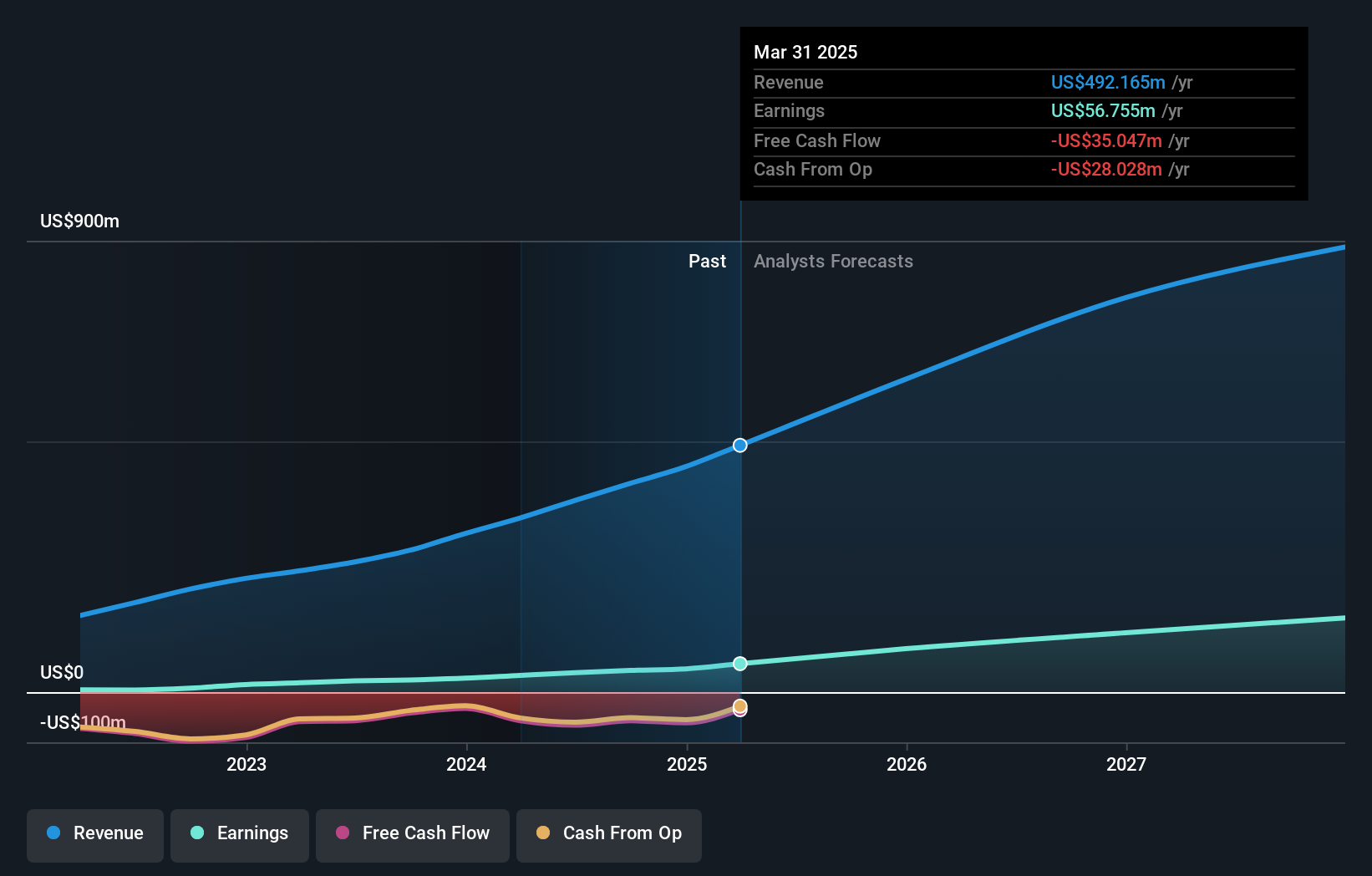

Propel Holdings (TSX:PRL)

Simply Wall St Growth Rating: ★★★★★★

Overview: Propel Holdings Inc., along with its subsidiaries, operates as a financial technology company and has a market cap of CA$1.23 billion.

Operations: The company's revenue is primarily derived from providing lending-related services to borrowers, banks, and other institutions, amounting to $492.16 million.

Insider Ownership: 36.5%

Propel Holdings, with substantial insider ownership, is poised for significant growth. Recent earnings showed a 69.5% increase in profits year-over-year, with revenue reaching US$138.94 million for Q1 2025. Analysts forecast annual earnings growth of 33%, surpassing the Canadian market's average. Despite trading at a discount to fair value, Propel has not engaged in share buybacks recently but increased its dividend by 9%. Debt refinancing and credit facility upsizing aim to lower capital costs further enhancing financial stability.

- Click here and access our complete growth analysis report to understand the dynamics of Propel Holdings.

- Our valuation report unveils the possibility Propel Holdings' shares may be trading at a discount.

Key Takeaways

- Take a closer look at our Fast Growing TSX Companies With High Insider Ownership list of 44 companies by clicking here.

- Contemplating Other Strategies? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:AII

Almonty Industries

Engages in mining, processing, and shipping of tungsten concentrate.

Exceptional growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor