Advertisement

Intact Financial Corporation's (TSE:IFC) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

It is hard to get excited after looking at Intact Financial's (TSE:IFC) recent performance, when its stock has declined 14% over the past three months. However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. In this article, we decided to focus on Intact Financial's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Intact Financial is:

13% = CA$2.4b ÷ CA$19b (Based on the trailing twelve months to June 2025).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each CA$1 of shareholders' capital it has, the company made CA$0.13 in profit.

See our latest analysis for Intact Financial

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Intact Financial's Earnings Growth And 13% ROE

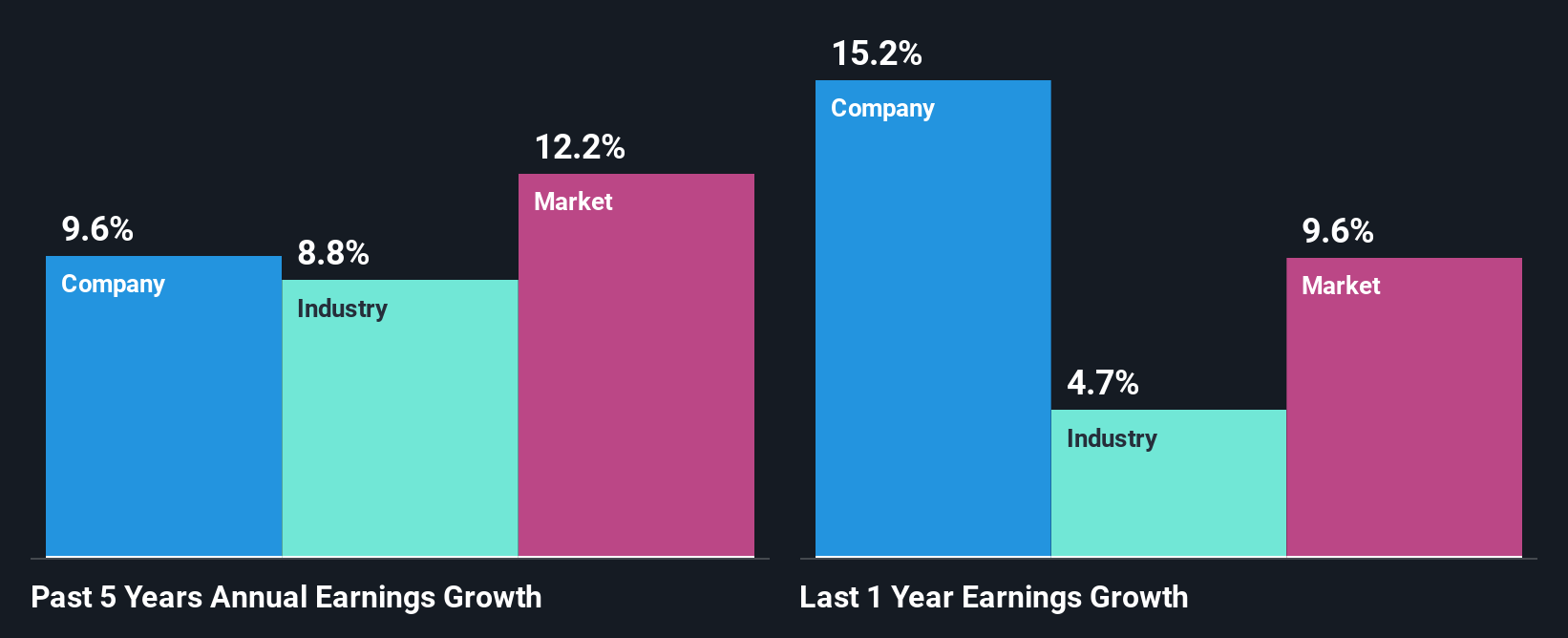

To begin with, Intact Financial seems to have a respectable ROE. Even when compared to the industry average of 13% the company's ROE looks quite decent. Consequently, this likely laid the ground for the decent growth of 9.6% seen over the past five years by Intact Financial.

We then performed a comparison between Intact Financial's net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 8.8% in the same 5-year period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. What is IFC worth today? The intrinsic value infographic in our free research report helps visualize whether IFC is currently mispriced by the market.

Is Intact Financial Making Efficient Use Of Its Profits?

Intact Financial has a three-year median payout ratio of 40%, which implies that it retains the remaining 60% of its profits. This suggests that its dividend is well covered, and given the decent growth seen by the company, it looks like management is reinvesting its earnings efficiently.

Additionally, Intact Financial has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 33% of its profits over the next three years. Still, forecasts suggest that Intact Financial's future ROE will rise to 16% even though the the company's payout ratio is not expected to change by much.

Conclusion

In total, we are pretty happy with Intact Financial's performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. Unsurprisingly, this has led to an impressive earnings growth. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:IFC

Intact Financial

Through its subsidiaries, provides property and casualty insurance products to individuals and businesses in Canada, the United States, the United Kingdom, and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

AB

Abc on Global X Etfs Icav - Global X Silver Miners Ucits ETF ·

Many trends acting at the same time

Fair Value:€10068.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative