Advertisement

The harsh reality for Jura Energy Corporation (CVE:JEC) shareholders is that its auditors, PricewaterhouseCoopers LLP, expressed doubts about its ability to continue as a going concern, in its reported results to December 2020. It is therefore fair to assume that, based on those financials, the company should strengthen its balance sheet in the short term, perhaps by issuing shares.

If the company does have to issue more shares, potential investors will be sure to consider how desperate it is for capital. So it is suddenly extremely important to consider whether the company is taking too much risk on its balance sheet. Debt is always a risk factor in these cases, as creditors could be in a position to wind up the company, in the worst case scenario.

View our latest analysis for Jura Energy

How Much Debt Does Jura Energy Carry?

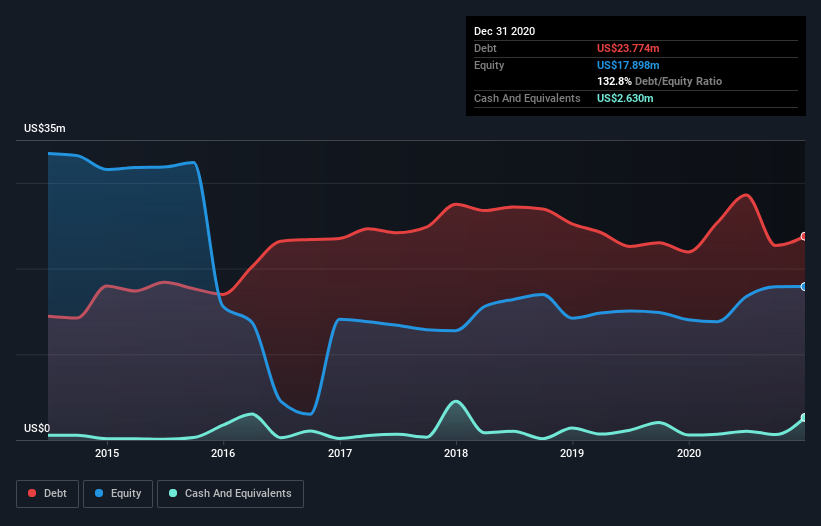

As you can see below, at the end of December 2020, Jura Energy had US$23.8m of debt, up from US$21.9m a year ago. Click the image for more detail. However, because it has a cash reserve of US$2.63m, its net debt is less, at about US$21.1m.

How Healthy Is Jura Energy's Balance Sheet?

We can see from the most recent balance sheet that Jura Energy had liabilities of US$20.7m falling due within a year, and liabilities of US$25.4m due beyond that. On the other hand, it had cash of US$2.63m and US$12.2m worth of receivables due within a year. So it has liabilities totalling US$31.2m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of US$22.4m, we think shareholders really should watch Jura Energy's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Jura Energy's net debt is sitting at a very reasonable 1.6 times its EBITDA, while its EBIT covered its interest expense just 2.5 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Notably, Jura Energy's EBIT launched higher than Elon Musk, gaining a whopping 100% on last year. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Jura Energy will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Jura Energy recorded free cash flow worth 63% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Jura Energy's level of total liabilities and interest cover definitely weigh on it, in our esteem. But its EBIT growth rate tells a very different story, and suggests some resilience. We think that Jura Energy's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. Some investors may be interested in buying high risk stocks at the right price, but we prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. We prefer to invest in companies that ensure the balance sheet remains healthier than that. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for Jura Energy you should be aware of, and 2 of them are a bit concerning.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:JEC

Jura Energy

Engages in the exploration, extraction, and production of oil and natural gas properties in Pakistan and Canada.

Good value with slight risk.

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.7% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Pagaya Technologies ·

The "Rate Cut" Supercycle Winner – Profitable & Accelerating

Fair Value:US$170.685.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$16.3254.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

110 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative