- Canada

- /

- Metals and Mining

- /

- TSX:DPM

Dundee Precious Metals And 2 Other Undiscovered Gems In Canada

Reviewed by Simply Wall St

The Canadian market has shown impressive resilience with a 1.6% increase in the last week and a remarkable 25% climb over the past year, alongside projected annual earnings growth of 16%. In this thriving environment, identifying promising stocks like Dundee Precious Metals and two other lesser-known opportunities can offer investors potential for strong returns by leveraging current market momentum.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 15.28% | 7.58% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Lithium Chile | NA | nan | 30.02% | ★★★★★★ |

| Westshore Terminals Investment | NA | -2.67% | -9.77% | ★★★★★☆ |

| Grown Rogue International | 24.92% | 43.35% | 67.95% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

| Dundee | 5.93% | -38.65% | 39.44% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

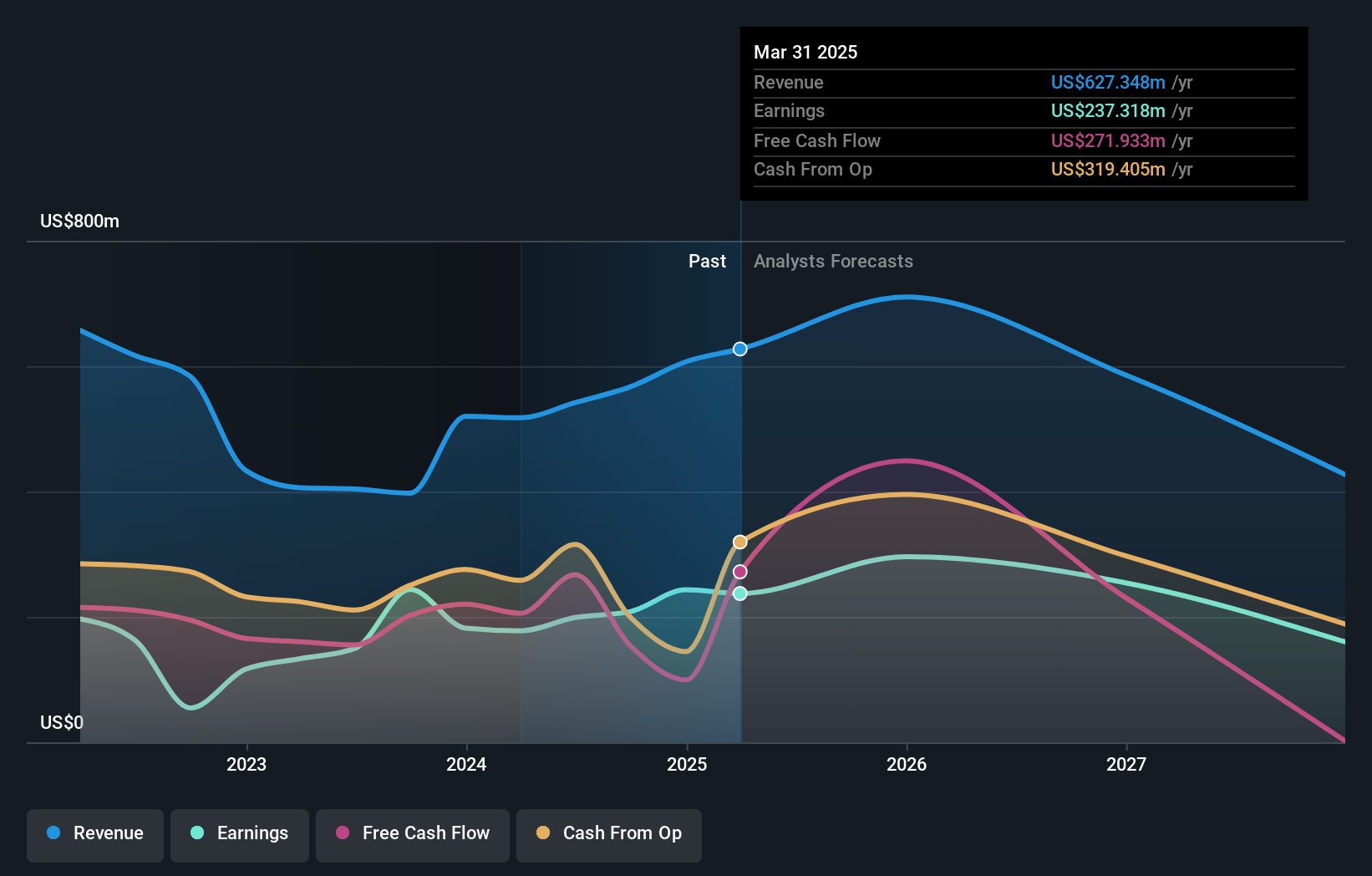

Dundee Precious Metals (TSX:DPM)

Simply Wall St Value Rating: ★★★★★★

Overview: Dundee Precious Metals Inc. is a gold mining company involved in the acquisition, exploration, development, mining, and processing of precious metals with a market capitalization of CA$2.53 billion.

Operations: Dundee Precious Metals generates revenue primarily from its Ada Tepe and Chelopech segments, contributing $237.16 million and $304.68 million, respectively.

Dundee Precious Metals stands out with its debt-free status, a significant improvement from five years ago when its debt to equity ratio was 6%. The company has demonstrated high-quality earnings, with a notable 33% growth in the past year, surpassing the industry average of 2.8%. Trading at 25% below estimated fair value suggests potential undervaluation. Recent operational highlights include processing over 711 Kt of ore and producing substantial quantities of gold and copper. Additionally, DPM repurchased over three million shares for $26.4 million this year, indicating confidence in its own valuation amidst ongoing project advancements like Coka Rakita.

- Click here to discover the nuances of Dundee Precious Metals with our detailed analytical health report.

Gain insights into Dundee Precious Metals' past trends and performance with our Past report.

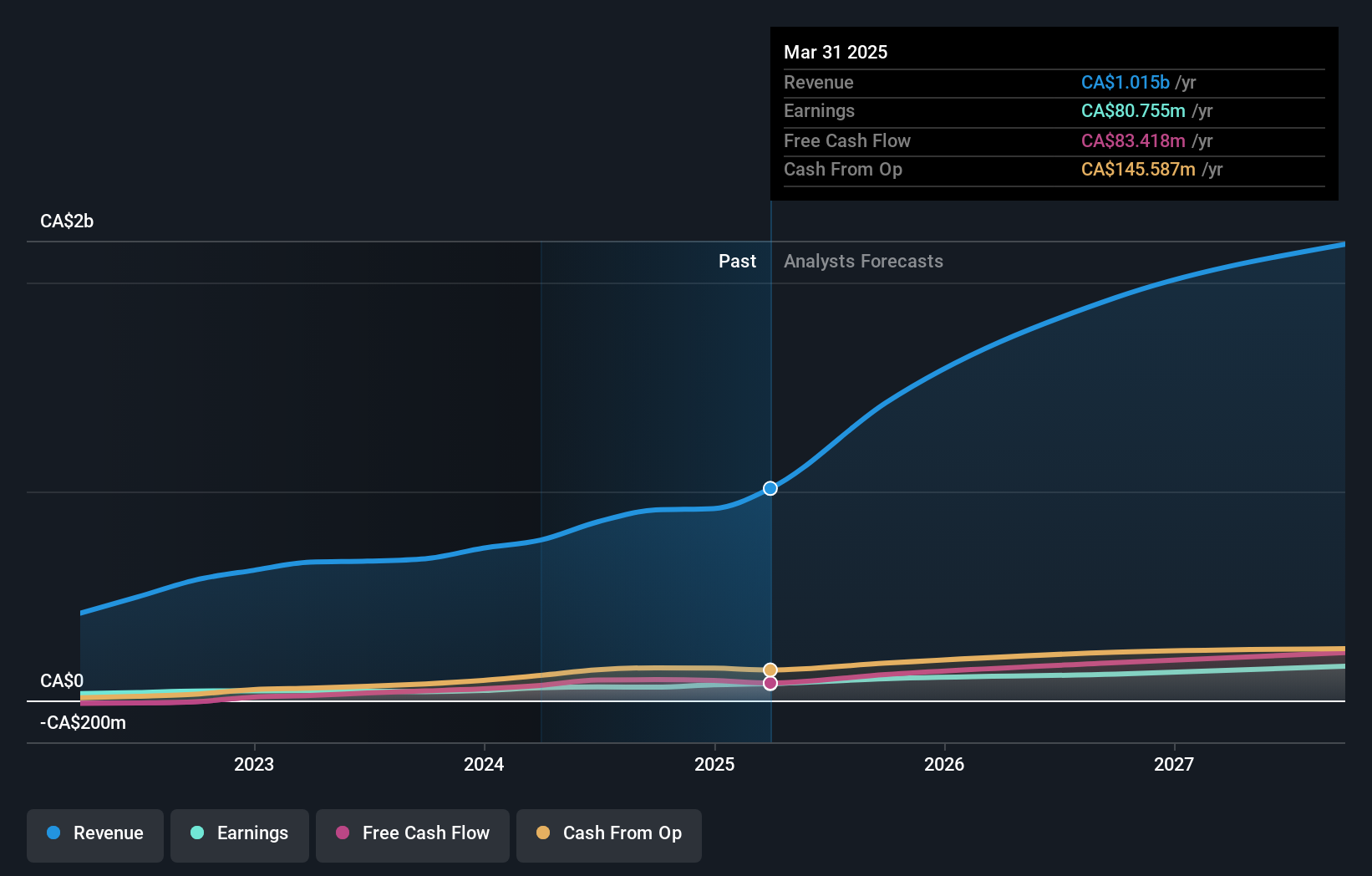

TerraVest Industries (TSX:TVK)

Simply Wall St Value Rating: ★★★★★☆

Overview: TerraVest Industries Inc. is a Canadian company that manufactures and sells goods and services to the energy, agriculture, mining, transportation, and other markets in Canada and the United States, with a market cap of CA$1.98 billion.

Operations: The company generates revenue primarily from HVAC and Containment Equipment (CA$292.90 million), Compressed Gas Equipment (CA$243.77 million), Service (CA$201.78 million), and Processing Equipment (CA$117.58 million). The Corporate segment shows a slight negative contribution of CA$0.93 million to the overall revenue mix.

TerraVest Industries, a Canadian player in the energy services sector, has shown promising growth with earnings up 43.6% over the past year, outpacing its industry peers. The company reported a significant revenue increase to CAD 238 million in Q3 from CAD 150 million last year, boosting net income to CAD 11.92 million from CAD 7.97 million. Despite a high net debt to equity ratio at 42%, it has reduced significantly from five years ago when it was at 117.9%. Recently added to the S&P Global BMI Index and trading below its estimated fair value by about 21%, TerraVest seems poised for continued attention in the market.

Westshore Terminals Investment (TSX:WTE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Westshore Terminals Investment Corporation operates a coal storage and unloading/loading terminal at Roberts Bank, British Columbia, with a market capitalization of CA$1.49 billion.

Operations: The company generates revenue primarily from its transportation infrastructure segment, totaling CA$379.34 million.

Westshore Terminals, a notable player in the infrastructure sector, has shown impressive earnings growth of 36.4% over the past year, surpassing the industry's 10.9%. Trading at 8.2% below its estimated fair value, it offers potential for investors seeking undervalued opportunities. The company is debt-free and has consistently delivered high-quality earnings without concerns over interest payments or cash runway due to profitability. Recent activities include a share buyback of 675,009 shares for CAD 15.56 million and a dividend announcement of CAD 0.375 per share for Q3 2024, though it was recently removed from several S&P/TSX indices in September.

- Get an in-depth perspective on Westshore Terminals Investment's performance by reading our health report here.

Understand Westshore Terminals Investment's track record by examining our Past report.

Seize The Opportunity

- Reveal the 50 hidden gems among our TSX Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Dundee Precious Metals, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:DPM

Dundee Precious Metals

A gold mining company, engages in the acquisition, exploration, development, mining, and processing of precious metals.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives