TC Energy Corporation (TSE:TRP) will increase its dividend from last year's comparable payment on the 30th of April to CA$0.96. This will take the dividend yield to an attractive 7.0%, providing a nice boost to shareholder returns.

See our latest analysis for TC Energy

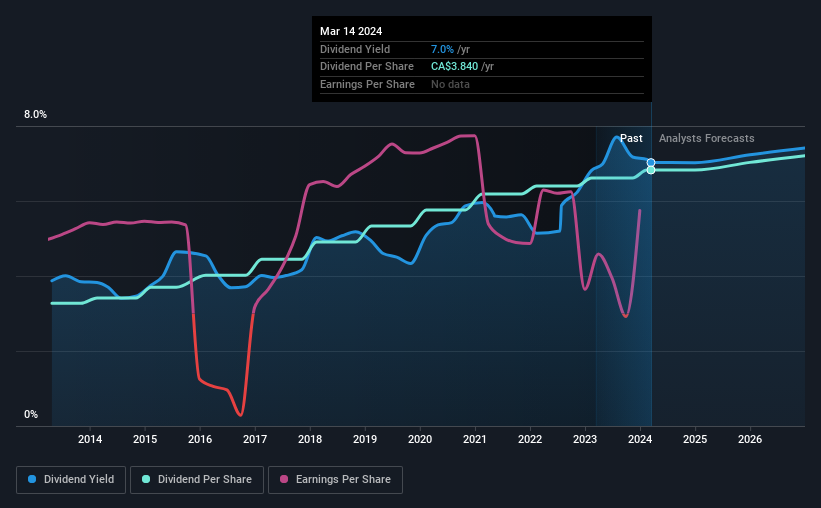

TC Energy's Dividend Is Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, the dividend made up 135% of earnings, and the company was generating negative free cash flows. This high of a dividend payment could start to put pressure on the balance sheet in the future.

EPS is set to grow by 80.8% over the next year. Assuming the dividend continues along recent trends, our estimates say the payout ratio could reach 82% - on the higher side, but we wouldn't necessarily say this is unsustainable.

TC Energy Has A Solid Track Record

The company has an extended history of paying stable dividends. The dividend has gone from an annual total of CA$1.84 in 2014 to the most recent total annual payment of CA$3.84. This implies that the company grew its distributions at a yearly rate of about 7.6% over that duration. The growth of the dividend has been pretty reliable, so we think this can offer investors some nice additional income in their portfolio.

Dividend Growth May Be Hard To Come By

Investors could be attracted to the stock based on the quality of its payment history. Let's not jump to conclusions as things might not be as good as they appear on the surface. TC Energy has seen earnings per share falling at 7.0% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

The Dividend Could Prove To Be Unreliable

In summary, while it's always good to see the dividend being raised, we don't think TC Energy's payments are rock solid. We can't deny that the payments have been very stable, but we are a little bit worried about the very high payout ratio. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, TC Energy has 3 warning signs (and 2 which don't sit too well with us) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if TC Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:TRP

Average dividend payer low.