- Canada

- /

- Healthcare Services

- /

- TSX:EXE

Top TSX Dividend Stocks To Watch In December 2024

Reviewed by Simply Wall St

As the Canadian market navigates through a period of economic assessment and strategic portfolio development, investors are increasingly focused on dividend stocks for their potential to provide steady income amidst fluctuating conditions. In this environment, identifying strong dividend stocks involves evaluating companies with solid fundamentals and a consistent track record of returning value to shareholders.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 7.45% | ★★★★★★ |

| Acadian Timber (TSX:ADN) | 6.42% | ★★★★★★ |

| Olympia Financial Group (TSX:OLY) | 6.64% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 4.88% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.78% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.34% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 3.79% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.09% | ★★★★★☆ |

| Richards Packaging Income Fund (TSX:RPI.UN) | 5.65% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 3.92% | ★★★★★☆ |

Click here to see the full list of 29 stocks from our Top TSX Dividend Stocks screener.

Here's a peek at a few of the choices from the screener.

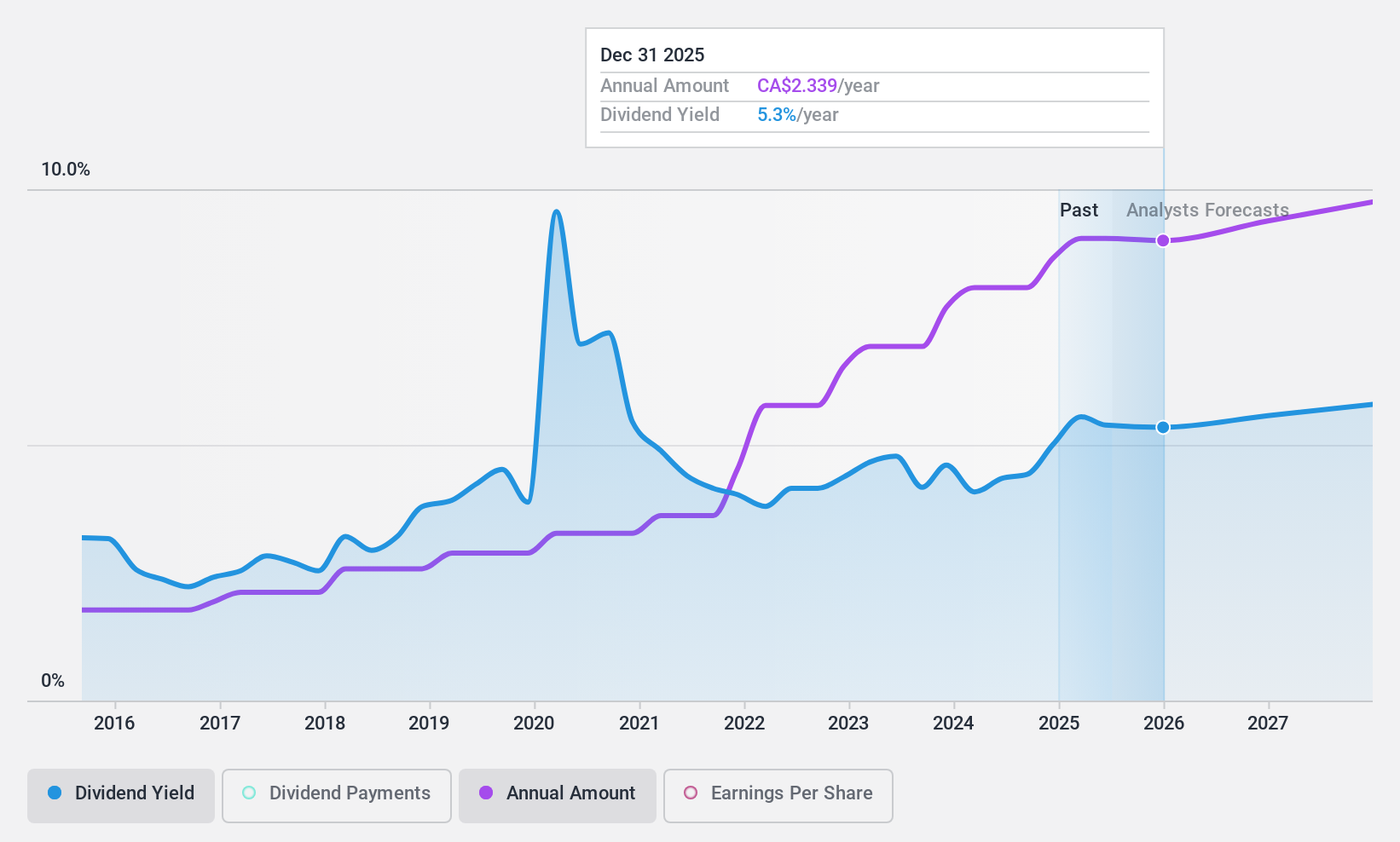

Canadian Natural Resources (TSX:CNQ)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Canadian Natural Resources Limited is involved in acquiring, exploring, developing, producing, marketing, and selling crude oil, natural gas, and natural gas liquids with a market cap of approximately CA$94.50 billion.

Operations: Canadian Natural Resources Limited generates revenue from several segments, including Oil Sands Mining and Upgrading (CA$16.30 billion), Exploration and Production - North America (CA$17.21 billion), Midstream and Refining (CA$937 million), Exploration and Production - North Sea (CA$537 million), and Exploration and Production - Offshore Africa (CA$557 million).

Dividend Yield: 4.8%

Canadian Natural Resources has recently increased its quarterly dividend by 7% to C$0.5625 per share, reflecting a commitment to returning value to shareholders. The company's dividend is well-covered by both earnings and cash flows, with payout ratios of 58.4% and 45.6%, respectively, indicating sustainability. Although the dividend yield of 4.78% is below the top quartile in Canada, it remains reliable and stable over a decade, supported by recent acquisitions that enhance cash flow potential.

- Unlock comprehensive insights into our analysis of Canadian Natural Resources stock in this dividend report.

- The analysis detailed in our Canadian Natural Resources valuation report hints at an deflated share price compared to its estimated value.

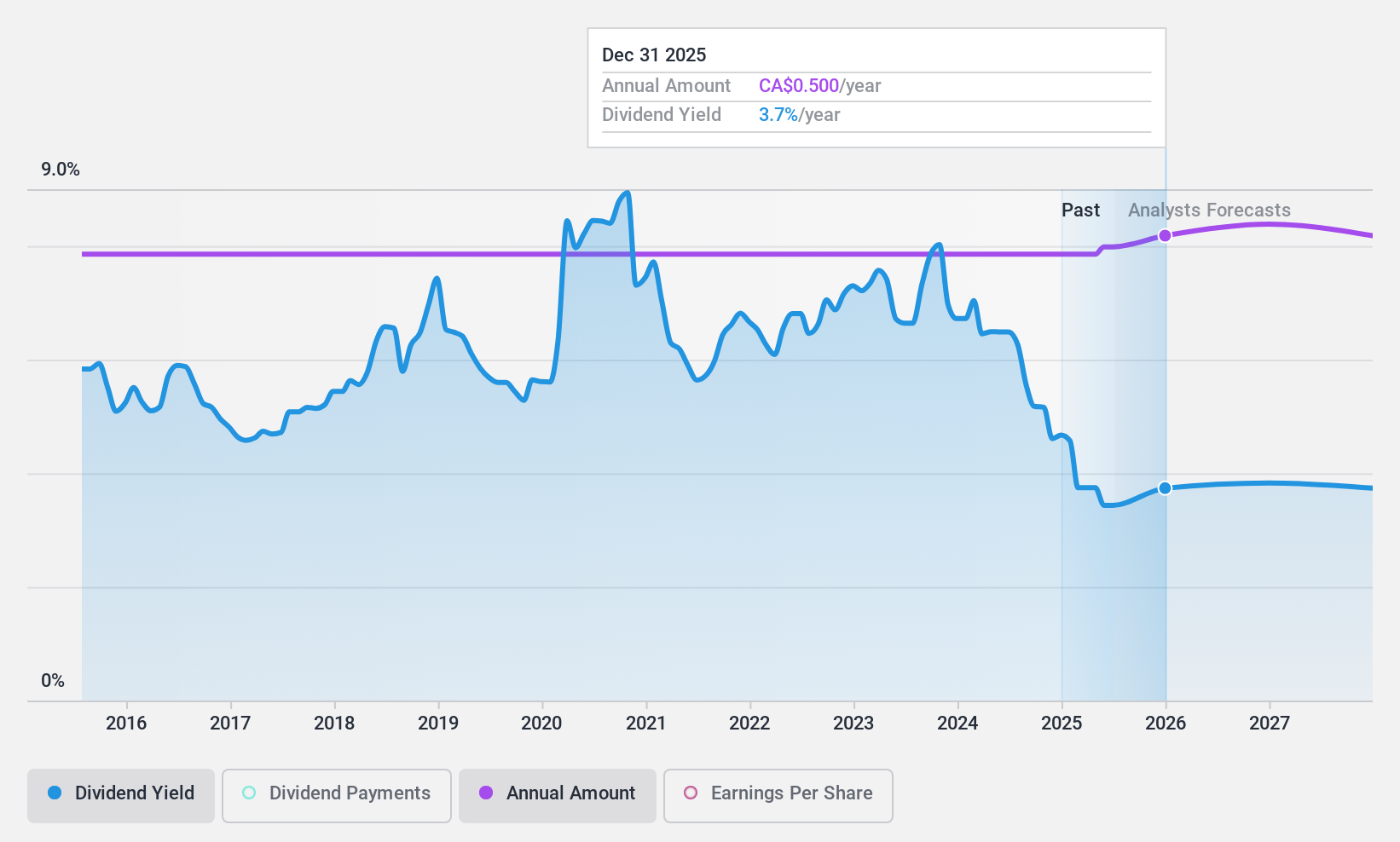

Extendicare (TSX:EXE)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Extendicare Inc., with a market cap of CA$848.86 million, operates through its subsidiaries to provide care and services for seniors in Canada.

Operations: Extendicare Inc.'s revenue is derived from three main segments: Long-Term Care (CA$808.94 million), Home Health Care (CA$545.46 million), and Managed Services (CA$70.43 million).

Dividend Yield: 4.7%

Extendicare's dividend yield of 4.72% is below the Canadian top quartile, with payments covered by earnings (63.3%) and cash flows (41.5%), ensuring sustainability despite a high debt level. Dividends have been stable but not growing over the past decade, with recent affirmations of CAD 0.04 per share monthly dividends through December 2024. Earnings growth has been robust, yet dividend reliability remains a concern due to historical volatility and lack of growth.

- Click here and access our complete dividend analysis report to understand the dynamics of Extendicare.

- Our valuation report here indicates Extendicare may be overvalued.

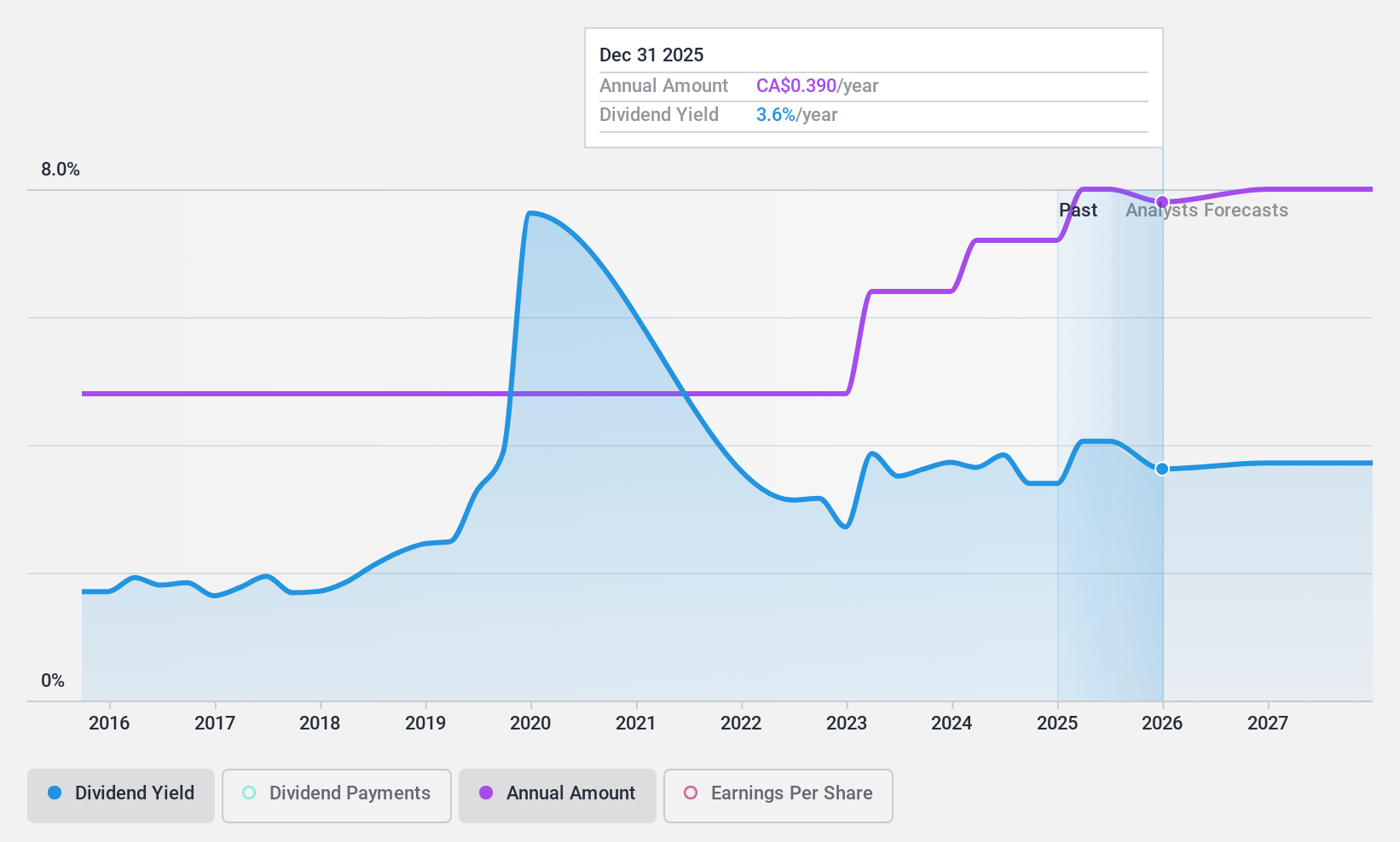

Total Energy Services (TSX:TOT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Total Energy Services Inc. is an energy services company operating in Canada, the United States, and Australia with a market cap of CA$448.79 million.

Operations: Total Energy Services Inc. generates its revenue from four main segments: Well Servicing (CA$91.14 million), Contract Drilling Services (CA$310.43 million), Compression and Process Services (CA$392.99 million), and Rentals and Transportation Services (CA$79.16 million).

Dividend Yield: 3%

Total Energy Services offers a low dividend yield of 3.05%, underperforming compared to Canada's top quartile, but maintains strong coverage with a payout ratio of 32.3% and cash payout at 14.2%. Despite past volatility in dividends, recent affirmations include a CAD 0.09 quarterly payment for December 2024. The company is actively pursuing M&A opportunities while executing share buybacks, having repurchased approximately 4.7% of its issued capital recently, indicating strategic financial management and shareholder returns focus.

- Get an in-depth perspective on Total Energy Services' performance by reading our dividend report here.

- Our valuation report here indicates Total Energy Services may be undervalued.

Taking Advantage

- Take a closer look at our Top TSX Dividend Stocks list of 29 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Extendicare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:EXE

Extendicare

Through its subsidiaries, provides care and services for seniors in Canada.

Solid track record established dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)