Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:CCO

Cameco (TSX:CCO) Valuation Check After Powerful Multi‑Year Run And Recent Pullback

Simply Wall St

Reviewed by Simply Wall St

Cameco (TSX:CCO) has been on a strong long term run, even after a recent pullback this month, and that combination is exactly what has uranium investors rechecking their expectations.

See our latest analysis for Cameco.

With the share price still around CA$123.40 after a 1 month share price return of roughly negative 13 percent, but a powerful year to date share price return above 60 percent and a 5 year total shareholder return above 700 percent, momentum looks more like a healthy pause than a trend reversal as investors reassess growth expectations and uranium market risks.

If Cameco’s run has you thinking about where the next big winners might come from, this could be a good moment to explore fast growing stocks with high insider ownership.

With earnings rising, uranium demand improving and the stock still trading below analyst targets, investors now face a key question: Is Cameco still undervalued, or is the market already pricing in its next phase of growth?

Most Popular Narrative Narrative: 18.7% Undervalued

With Cameco last closing at CA$123.40 against a narrative fair value of CA$151.75, the current price implies meaningful upside if the thesis plays out.

Analysts expect earnings to reach CA$1.2 billion (and earnings per share of CA$2.8) by about September 2028, up from CA$533.6 million today. However, there is a considerable amount of disagreement amongst the analysts, with the most bullish expecting CA$1.3 billion in earnings and the most bearish expecting CA$873 million.

Want to see what kind of revenue expansion, margin lift, and future earnings multiple are included in that upside case? The narrative relies on bold growth assumptions, an aggressive profitability reset, and a premium valuation that would usually sit with market darlings. Curious how those moving parts combine into one target number? Read on to uncover the full playbook behind this fair value.

Result: Fair Value of $151.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent delays in new reactor approvals and ongoing operational challenges at key mines could easily derail Cameco’s high growth and margin expansion narrative.

Find out about the key risks to this Cameco narrative.

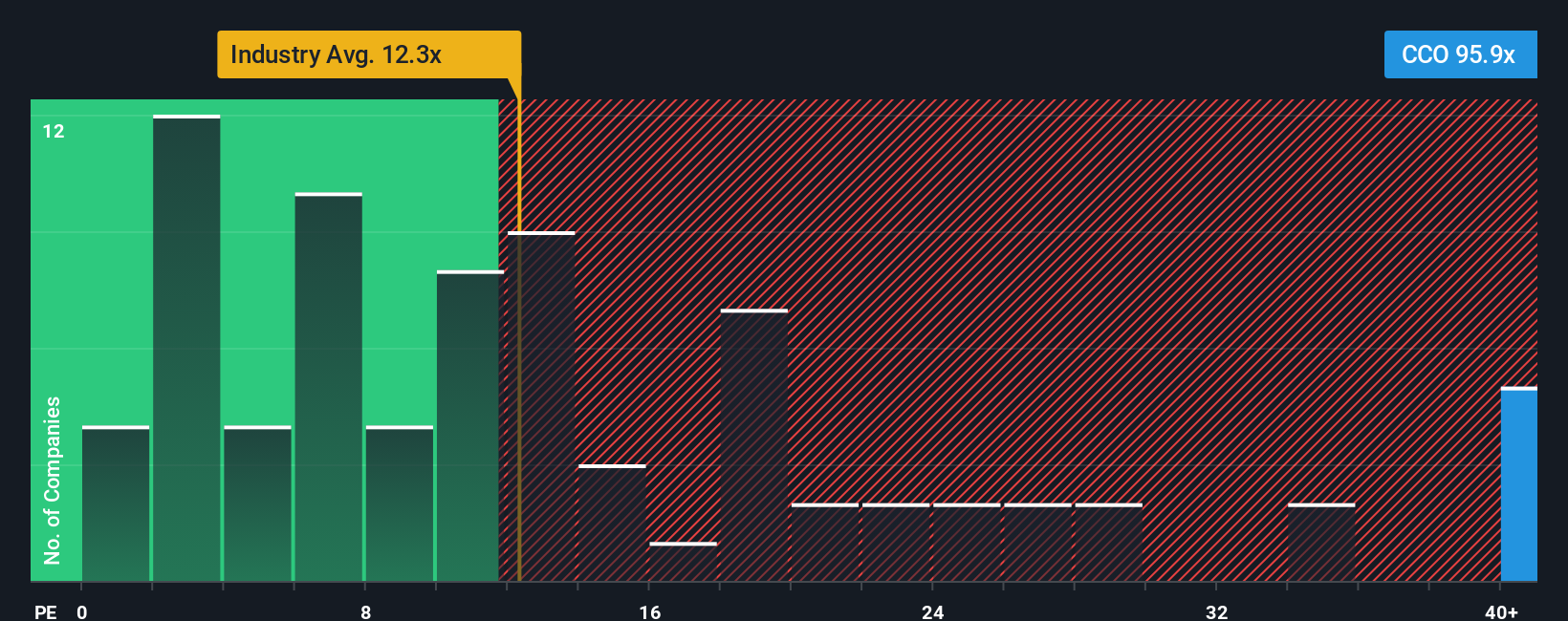

Another Way To Look At Value

While the narrative fair value suggests Cameco is 18.7 percent undervalued, its current price to earnings ratio of about 102 times tells a very different story. This is far above peers at 16.4 times and above a fair ratio of 20.7 times, which points to real downside risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Cameco Narrative

If you see the story differently or want to stress test the assumptions with your own research, you can craft a personalized thesis in minutes using Do it your way.

A great starting point for your Cameco research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next potential winners by using the Simply Wall Street Screener to uncover opportunities most investors are still overlooking.

- Capture early stage growth by targeting these 3569 penny stocks with strong financials that already back their promise with solid financial foundations and improving business momentum.

- Capitalize on structural tech shifts by focusing on these 24 AI penny stocks positioned at the heart of automation, data intelligence, and productivity transformation.

- Strengthen your long term core holdings with these 933 undervalued stocks based on cash flows that current market prices do not yet fully reflect, based on underlying cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CCO

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

11 followersusers have followed this narrative

5 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.562.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

947 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative