As the Canadian market navigates through a landscape of cautious interest rate cuts and persistent consumer spending, investors are keenly watching for opportunities that might be overlooked. In this context, understanding what constitutes an undervalued stock becomes crucial, especially when economic indicators suggest resilience yet consumer sentiment remains tepid.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Calian Group (TSX:CGY) | CA$56.15 | CA$110.49 | 49.2% |

| Kinaxis (TSX:KXS) | CA$151.10 | CA$250.17 | 39.6% |

| goeasy (TSX:GSY) | CA$195.18 | CA$313.75 | 37.8% |

| Trisura Group (TSX:TSU) | CA$41.23 | CA$80.18 | 48.6% |

| Calibre Mining (TSX:CXB) | CA$1.82 | CA$3.22 | 43.5% |

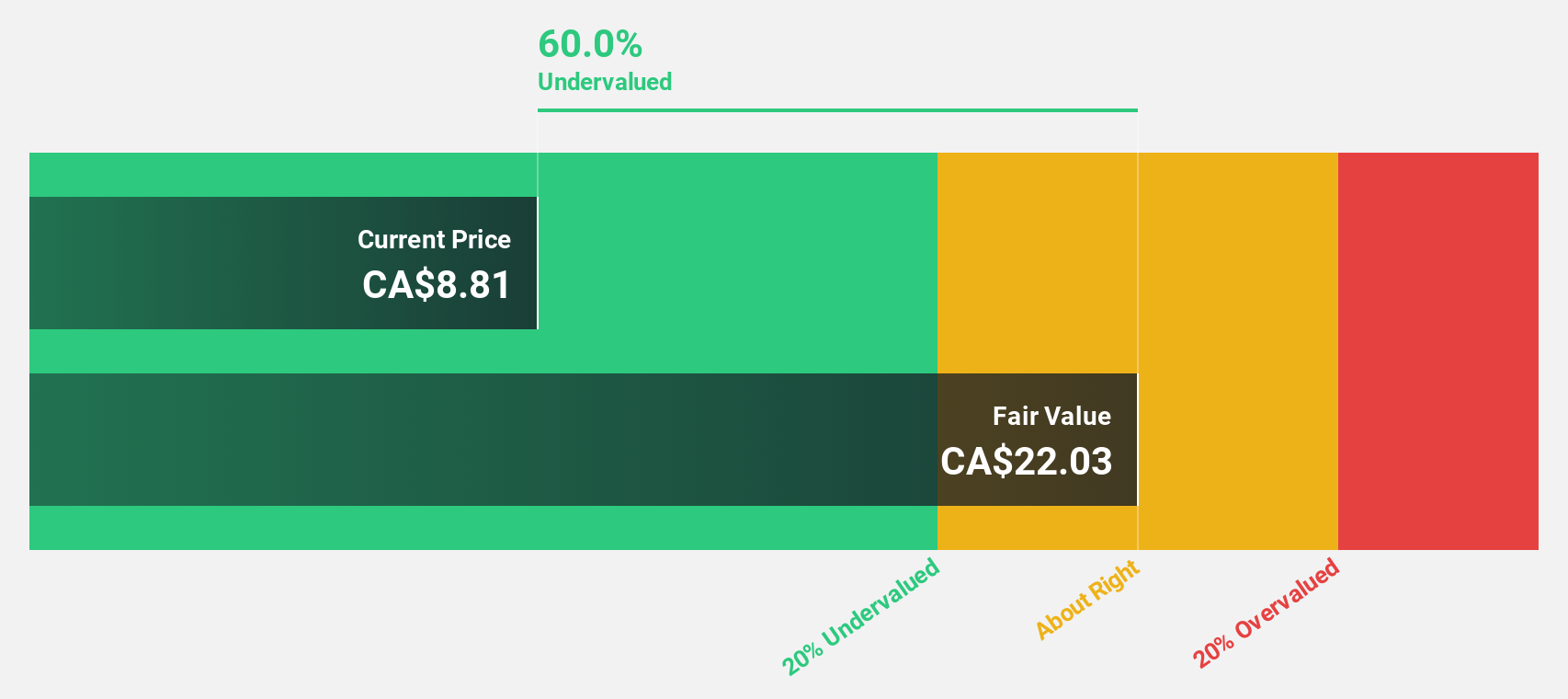

| Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

| Endeavour Mining (TSX:EDV) | CA$28.86 | CA$57.16 | 49.5% |

| Jamieson Wellness (TSX:JWEL) | CA$28.42 | CA$46.94 | 39.5% |

| Kits Eyecare (TSX:KITS) | CA$8.20 | CA$14.34 | 42.8% |

| Capstone Copper (TSX:CS) | CA$9.76 | CA$16.47 | 40.7% |

Below we spotlight a couple of our favorites from our exclusive screener

Green Thumb Industries (CNSX:GTII)

Overview: Green Thumb Industries Inc. operates in the United States, focusing on the manufacture, distribution, marketing, and sale of cannabis products for both medical and adult use, with a market capitalization of approximately CA$4.05 billion.

Operations: The company generates revenue primarily through two segments: Retail, which brought in $806.38 million, and Consumer Packaged Goods, contributing $583.78 million.

Estimated Discount To Fair Value: 35.5%

Green Thumb Industries, priced at CA$17.52, significantly under our fair value estimate of CA$27.15, shows strong financial promise with its recent transition to profitability and a robust forecast for earnings growth at 27.3% annually—outpacing the Canadian market's 14.6%. Despite these positives, its projected Return on Equity of 10.2% suggests moderate efficiency in generating profit from shareholders' equity. Recent expansions and potential strategic mergers indicate proactive management but also underscore inherent risks in ambitious growth strategies and regulatory environments.

- The analysis detailed in our Green Thumb Industries growth report hints at robust future financial performance.

- Dive into the specifics of Green Thumb Industries here with our thorough financial health report.

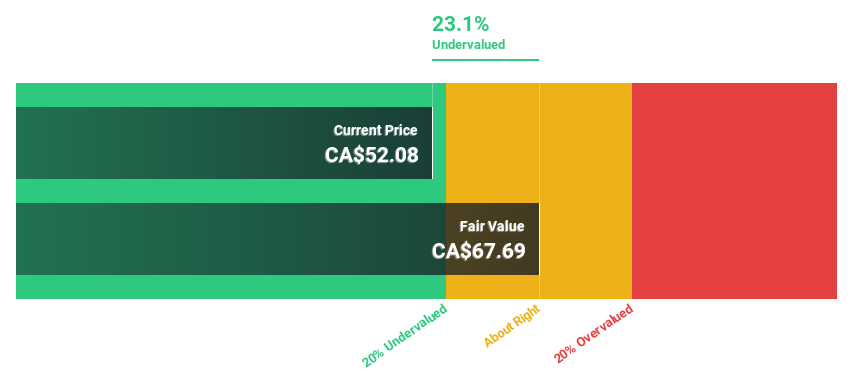

Brookfield Asset Management (TSX:BAM)

Overview: Brookfield Asset Management Ltd. is a real estate investment firm specializing in alternative asset management services, with a market capitalization of approximately CA$21.85 billion.

Operations: The firm primarily focuses on alternative asset management, generating its revenue from real estate investments.

Estimated Discount To Fair Value: 22.5%

Brookfield Asset Management, priced at CA$52.33, trades significantly below our fair value estimate of CA$67.53, reflecting its undervaluation based on discounted cash flows. Despite the company's revenue forecast to grow by 61.8% annually and earnings expected to increase by 74.6% per year, it remains underappreciated in the market. Recent M&A activities and strategic asset sales underscore its proactive approach in optimizing its portfolio for enhanced profitability, although shareholder dilution over the past year and a dividend coverage issue signal areas for investor caution.

- Our comprehensive growth report raises the possibility that Brookfield Asset Management is poised for substantial financial growth.

- Click to explore a detailed breakdown of our findings in Brookfield Asset Management's balance sheet health report.

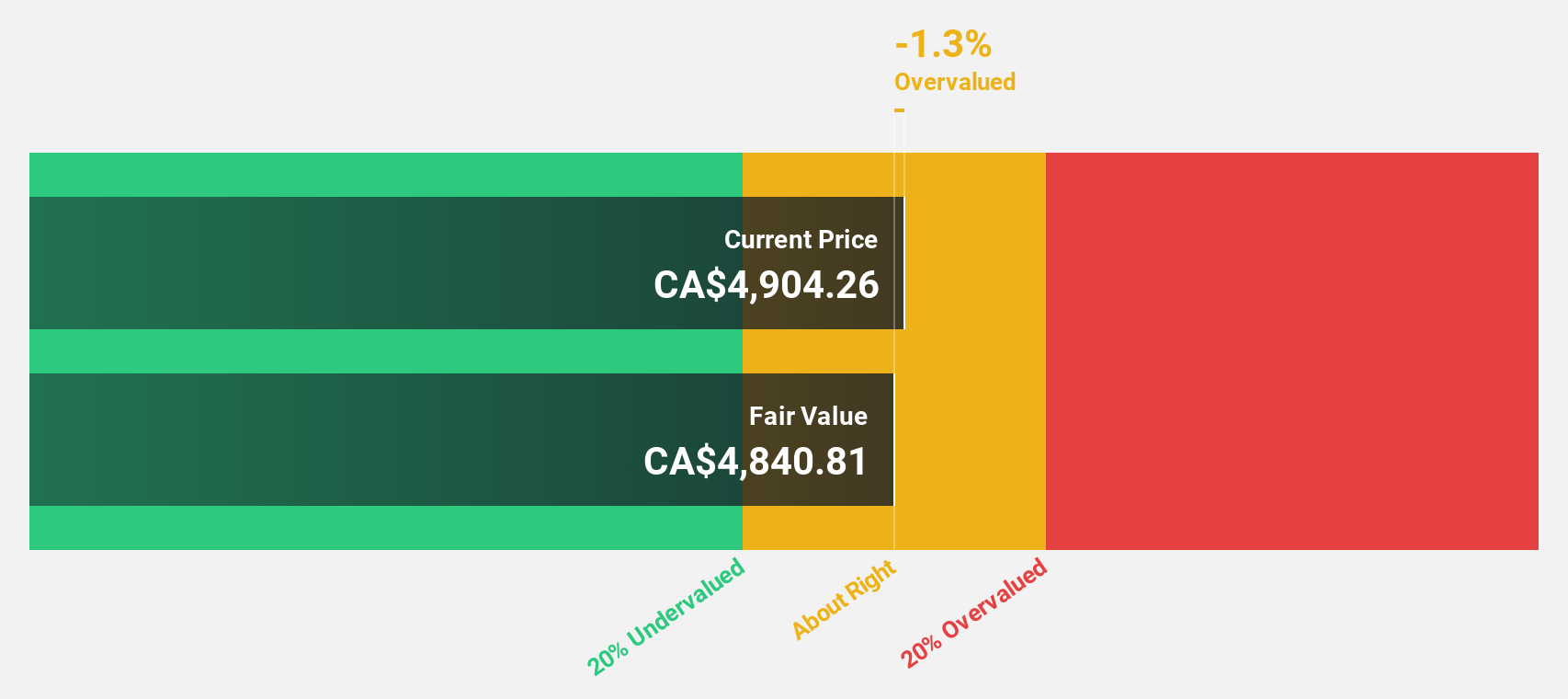

Constellation Software (TSX:CSU)

Overview: Constellation Software Inc. operates globally, focusing on acquiring, building, and managing vertical market software businesses primarily in Canada, the US, and Europe, with a market capitalization of approximately CA$81.97 billion.

Operations: The company's revenue from its software and programming segment totaled CA$8.84 billion.

Estimated Discount To Fair Value: 27.1%

Constellation Software, valued at CA$3927.5, is currently trading below its estimated fair value of CA$5384.17, indicating a potential undervaluation based on discounted cash flow analysis. Despite carrying high levels of debt, the company's robust forecasted earnings growth at 24.43% per year and revenue increase expectations of 16.1% annually outpace the Canadian market projections significantly. Recent executive changes and the launch of Omegro suggest strategic moves to bolster global software operations and capital deployment efficiency.

- The growth report we've compiled suggests that Constellation Software's future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Constellation Software.

Taking Advantage

- Explore the 21 names from our Undervalued TSX Stocks Based On Cash Flows screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Green Thumb Industries, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About CNSX:GTII

Green Thumb Industries

Manufactures, distributes, markets, and sells of cannabis products for medical and adult-use in the United States.

Undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives