- Canada

- /

- Oil and Gas

- /

- TSX:EFR

Exploring Three Top Undervalued Small Caps In Canada With Insider Actions

Reviewed by Simply Wall St

The Canadian market has shown robust performance, appreciating by 2.8% in the past week and 12% over the last year, with earnings projected to grow by 15% annually. In such a thriving environment, undervalued small caps with significant insider actions present intriguing opportunities for investors seeking potential growth.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Dundee Precious Metals | 9.0x | 3.1x | 44.23% | ★★★★★★ |

| Martinrea International | 6.0x | 0.2x | 48.76% | ★★★★★★ |

| Primaris Real Estate Investment Trust | 11.7x | 3.0x | 34.48% | ★★★★★☆ |

| Nexus Industrial REIT | 2.5x | 3.1x | 18.23% | ★★★★☆☆ |

| Calfrac Well Services | 2.3x | 0.2x | 26.74% | ★★★★☆☆ |

| Guardian Capital Group | 10.4x | 4.0x | 31.99% | ★★★★☆☆ |

| Sagicor Financial | 1.2x | 0.4x | -94.52% | ★★★★☆☆ |

| Westshore Terminals Investment | 14.3x | 3.9x | 0.92% | ★★★☆☆☆ |

| Russel Metals | 9.2x | 0.5x | -7.56% | ★★★☆☆☆ |

| Freehold Royalties | 15.8x | 6.8x | 47.43% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

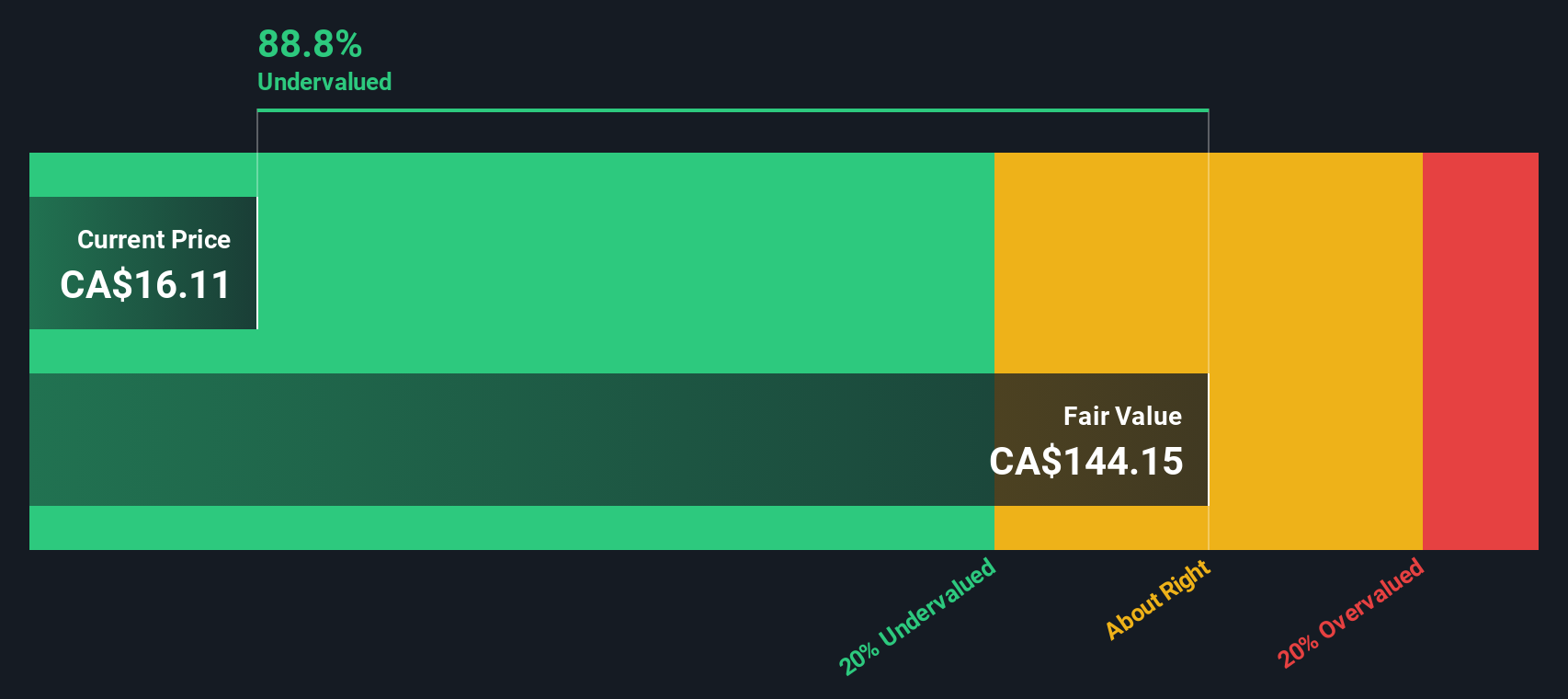

Energy Fuels (TSX:EFR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Energy Fuels is a company engaged in the extraction and recovery of uranium and vanadium, with a market capitalization of approximately $1.31 billion.

Operations: The entity generates revenue primarily through its Metals & Minings - Miscellaneous segment, which recorded $43.74 million in the latest period. Notably, it achieved a gross profit margin of 52.07% as of the most recent data point.

PE: -97.5x

Recently, Energy Fuels, a notable player in the rare earth elements (REE) and uranium sectors, demonstrated insider confidence with strategic insider purchases. With earnings forecasted to grow by 50.8% annually, their financial trajectory appears promising. Notably, they've achieved commercial production of separated REEs at their Utah Mill—a significant stride in positioning themselves within the critical minerals market. Despite dropping from several Russell indexes on July 1, 2024, they were added to the Russell 2000 Value-Defensive Index, reflecting a nuanced market perception. Their commitment to expanding uranium production underscores a robust strategy aimed at enhancing long-term shareholder value amidst dynamic market conditions.

- Get an in-depth perspective on Energy Fuels' performance by reading our valuation report here.

Examine Energy Fuels' past performance report to understand how it has performed in the past.

MTY Food Group (TSX:MTY)

Simply Wall St Value Rating: ★★★★☆☆

Overview: MTY Food Group is a diversified company operating primarily in the quick-service food industry, managing both corporate and franchised restaurants across Canada and internationally, with a market capitalization of approximately CA$1.41 billion.

Operations: MTY Food Group generates revenue primarily through its franchising operations in Canada and internationally, with significant contributions from corporate-owned locations and promotional funds. The gross profit margin has shown variability over the periods, highlighting changes in cost of goods sold and operational efficiency.

PE: 11.3x

Despite a slight dip in quarterly earnings, MTY Food Group's consistent sales figures and strategic share repurchases reflect a stable financial posture. Recently, insiders demonstrated confidence by acquiring shares, underscoring their belief in the company's prospects. With CAD 20.53 million spent on buybacks since last June and a robust dividend affirmed this July, MTY blends insider optimism with shareholder returns. This activity suggests that MTY may be positioned for growth, appealing to those eyeing underestimated entities in the market.

- Take a closer look at MTY Food Group's potential here in our valuation report.

Assess MTY Food Group's past performance with our detailed historical performance reports.

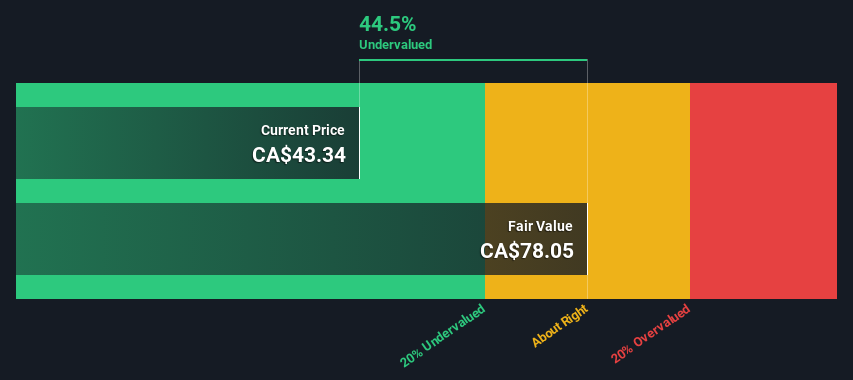

Russel Metals (TSX:RUS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Russel Metals operates as a metal distribution and processing company with a market cap of approximately CA$1.5 billion, serving various sectors including metals service centers, energy field stores, and steel distribution.

Operations: The company generates significant revenue from its Metals Service Centers, contributing CA$2.95 billion, followed by Energy Field Stores and Steel Distributors with CA$982.20 million and CA$429 million respectively. Its gross profit margin has shown a notable increase over the periods, reaching 0.213% by mid-2024 from an earlier figure of 0.171%.

PE: 9.2x

Russel Metals, a notable player in the metals service center industry, recently enhanced its market position by agreeing to acquire seven locations from Samuel, Son & Co., with completion expected in Q3 2024. Despite a dip in Q1 sales to CA$1.06 billion and net income falling to CA$49.7 million, the firm raised its quarterly dividend by 5% to CA$0.42 per share, signaling financial confidence and commitment to shareholder returns. Insider confidence is evident as they recently purchased shares; this move often reflects a positive internal outlook on the company's valuation and future prospects.

- Click to explore a detailed breakdown of our findings in Russel Metals' valuation report.

Explore historical data to track Russel Metals' performance over time in our Past section.

Summing It All Up

- Click this link to deep-dive into the 32 companies within our Undervalued TSX Small Caps With Insider Buying screener.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Energy Fuels might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:EFR

Energy Fuels

Engages in the exploration, recovery, recycling, exploration, operation, development, permitting, evaluation, and sale of uranium mineral properties in the United States.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Community Narratives