- Canada

- /

- Trade Distributors

- /

- CNSX:REK.U

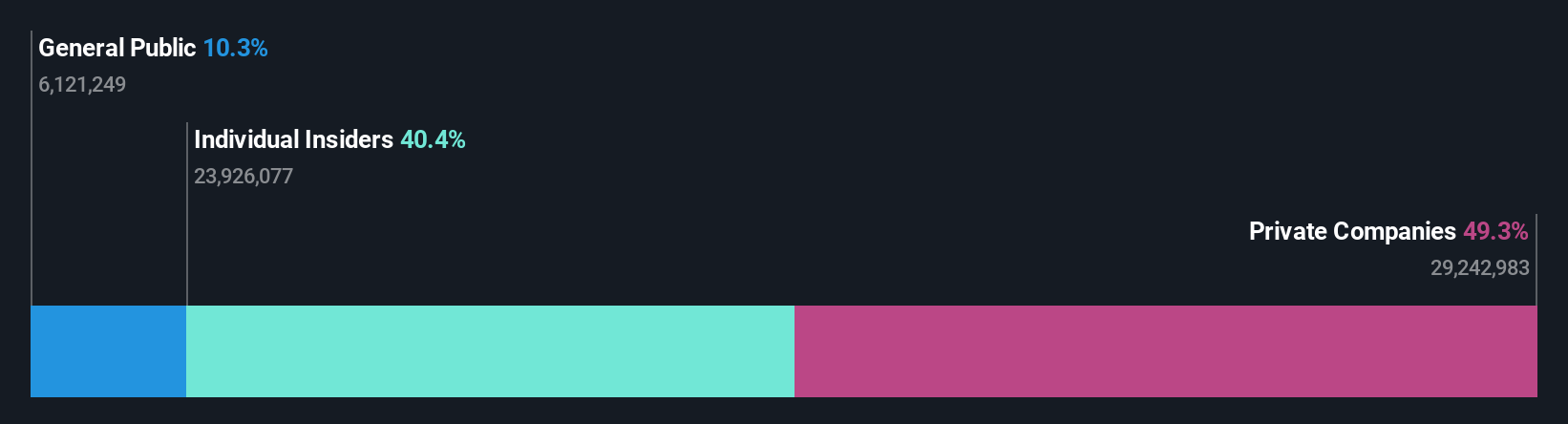

Private companies are Rektron Group Inc.'s (CSE:REK.U) biggest owners and were hit after market cap dropped US$21m

Key Insights

- The considerable ownership by private companies in Rektron Group indicates that they collectively have a greater say in management and business strategy

- A total of 2 investors have a majority stake in the company with 90% ownership

- Insiders own 40% of Rektron Group

If you want to know who really controls Rektron Group Inc. (CSE:REK.U), then you'll have to look at the makeup of its share registry. And the group that holds the biggest piece of the pie are private companies with 49% ownership. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

While the holdings of private companies took a hit after last week’s 10.0% price drop, insiders with their 40% also suffered.

Let's take a closer look to see what the different types of shareholders can tell us about Rektron Group.

See our latest analysis for Rektron Group

What Does The Lack Of Institutional Ownership Tell Us About Rektron Group?

We don't tend to see institutional investors holding stock of companies that are very risky, thinly traded, or very small. Though we do sometimes see large companies without institutions on the register, it's not particularly common.

There are many reasons why a company might not have any institutions on the share registry. It may be hard for institutions to buy large amounts of shares, if liquidity (the amount of shares traded each day) is low. If the company has not needed to raise capital, institutions might lack the opportunity to build a position. It is also possible that fund managers don't own the stock because they aren't convinced it will perform well. Rektron Group might not have the sort of past performance institutions are looking for, or perhaps they simply have not studied the business closely.

Rektron Group is not owned by hedge funds. The company's largest shareholder is Nile Flow Ltd., with ownership of 49%. Meanwhile, the second largest shareholder is Sanjeev Tolia holding 40%.

A more detailed study of the shareholder registry showed us that 2 of the top shareholders have a considerable amount of ownership in the company, via their 90% stake.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. While there is some analyst coverage, the company is probably not widely covered. So it could gain more attention, down the track.

Insider Ownership Of Rektron Group

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

It seems insiders own a significant proportion of Rektron Group Inc.. Insiders have a US$77m stake in this US$190m business. This may suggest that the founders still own a lot of shares. You can click here to see if they have been buying or selling.

General Public Ownership

With a 10% ownership, the general public, mostly comprising of individual investors, have some degree of sway over Rektron Group. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Private Company Ownership

It seems that Private Companies own 49%, of the Rektron Group stock. It might be worth looking deeper into this. If related parties, such as insiders, have an interest in one of these private companies, that should be disclosed in the annual report. Private companies may also have a strategic interest in the company.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Like risks, for instance. Every company has them, and we've spotted 3 warning signs for Rektron Group (of which 2 are a bit unpleasant!) you should know about.

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CNSX:REK.U

Rektron Group

Through its subsidiaries, trades in ferrous and nonferrous metals, crude oil, and refined oil products worldwide.

Low risk and slightly overvalued.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)