Does The Equitable Group Inc. (TSE:EQB) Share Price Fall With The Market?

If you own shares in Equitable Group Inc. (TSE:EQB) then it's worth thinking about how it contributes to the volatility of your portfolio, overall. In finance, Beta is a measure of volatility. Modern finance theory considers volatility to be a measure of risk, and there are two main types of price volatility. First, we have company specific volatility, which is the price gyrations of an individual stock. Holding at least 8 stocks can reduce this kind of risk across a portfolio. The second sort is caused by the natural volatility of markets, overall. For example, certain macroeconomic events will impact (virtually) all stocks on the market.

Some stocks mimic the volatility of the market quite closely, while others demonstrate muted, exagerrated or uncorrelated price movements. Some investors use beta as a measure of how much a certain stock is impacted by market risk (volatility). While we should keep in mind that Warren Buffett has cautioned that 'Volatility is far from synonymous with risk', beta is still a useful factor to consider. To make good use of it you must first know that the beta of the overall market is one. A stock with a beta greater than one is more sensitive to broader market movements than a stock with a beta of less than one.

View our latest analysis for Equitable Group

What does EQB's beta value mean to investors?

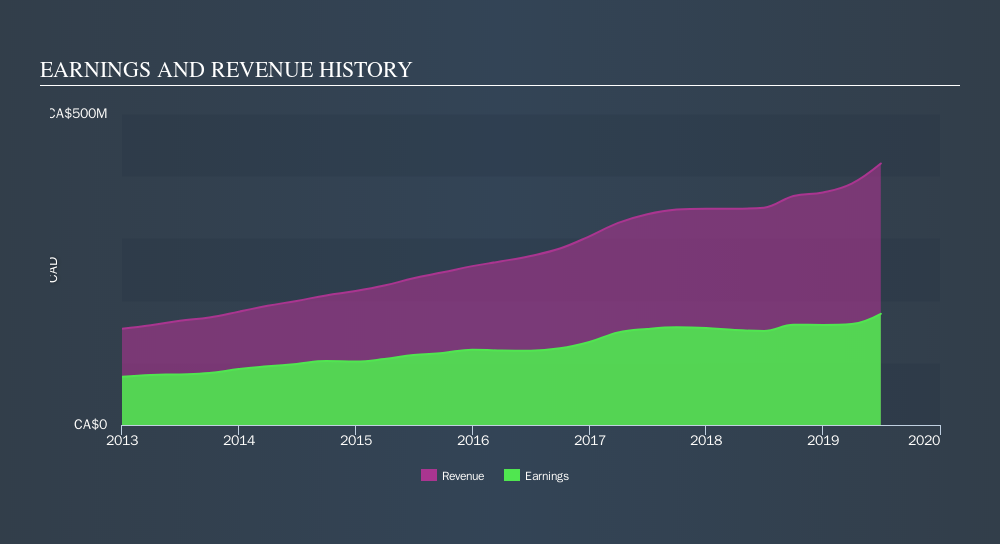

Zooming in on Equitable Group, we see it has a five year beta of 1.48. This is above 1, so historically its share price has been influenced by the broader volatility of the stock market. If the past is any guide, we would expect that Equitable Group shares will rise quicker than the markets in times of optimism, but fall faster in times of pessimism. Many would argue that beta is useful in position sizing, but fundamental metrics such as revenue and earnings are more important overall. You can see Equitable Group's revenue and earnings in the image below.

How does EQB's size impact its beta?

Equitable Group is a small cap stock with a market capitalisation of CA$1.7b. Most companies this size are actively traded. It's not particularly surprising that it has a higher beta than the overall market. That's because it takes less money to influence the share price of a smaller company, than a bigger company.

What this means for you:

Beta only tells us that the Equitable Group share price is sensitive to broader market movements. This could indicate that it is a high growth company, or is heavily influenced by sentiment because it is speculative. Alternatively, it could have operating leverage in its business model. Ultimately, beta is an interesting metric, but there's plenty more to learn. This article aims to educate investors about beta values, but it's well worth looking at important company-specific fundamentals such as Equitable Group’s financial health and performance track record. I highly recommend you dive deeper by considering the following:

- Future Outlook: What are well-informed industry analysts predicting for EQB’s future growth? Take a look at our free research report of analyst consensus for EQB’s outlook.

- Past Track Record: Has EQB been consistently performing well irrespective of the ups and downs in the market? Go into more detail in the past performance analysis and take a look at the free visual representations of EQB's historicals for more clarity.

- Other Interesting Stocks: It's worth checking to see how EQB measures up against other companies on valuation. You could start with this free list of prospective options.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:EQB

EQB

Through its subsidiary, Equitable Bank, provides personal and commercial banking services to retail and commercial customers in Canada.

High growth potential established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)