CIBC (TSX:CM) Valuation Check After Strong Earnings, Dividend Hike and CIBC by Expedia Expansion

Reviewed by Simply Wall St

CIBC (TSX:CM) just wrapped up a stronger year, lifting its dividend and extending its CIBC by Expedia travel platform, all in the context of a steady Bank of Canada rate backdrop that keeps the operating environment fairly predictable.

See our latest analysis for Canadian Imperial Bank of Commerce.

The steady macro backdrop and CIBC specific wins, from stronger earnings and a larger dividend to the CIBC by Expedia rollout, have underpinned a 15.08% 3 month share price return and a powerful 191.38% 5 year total shareholder return. This suggests momentum is still building rather than fading.

If this kind of steady compounding appeals to you, it may be a good moment to look beyond the big banks and explore fast growing stocks with high insider ownership.

With the share price already near analyst targets but intrinsic metrics still suggesting upside, is Canadian Imperial Bank of Commerce trading at a discount to its fundamentals, or is the market already baking in years of future growth?

Most Popular Narrative: 3.3% Overvalued

With Canadian Imperial Bank of Commerce last closing at CA$126.62 against a narrative fair value of about CA$122.57, expectations lean toward a mildly stretched valuation built on resilient earnings power.

Strong capital position (13.4% CET1), ongoing share buyback programs, and rising ROE (5 consecutive quarters of year over year increases) provide flexibility to drive both organic business growth and shareholder returns, further enhancing earnings per share.

Curious how modest revenue growth, steady margins and a richer earnings multiple can still add up to a higher fair value than today? See which forward profit and valuation assumptions underpin this call and how a mid single digit discount rate shapes the upside story.

Result: Fair Value of $122.57 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, elevated Canadian mortgage delinquencies and intensifying digital competition could quickly challenge the margin resilience that underpins this mildly stretched valuation.

Find out about the key risks to this Canadian Imperial Bank of Commerce narrative.

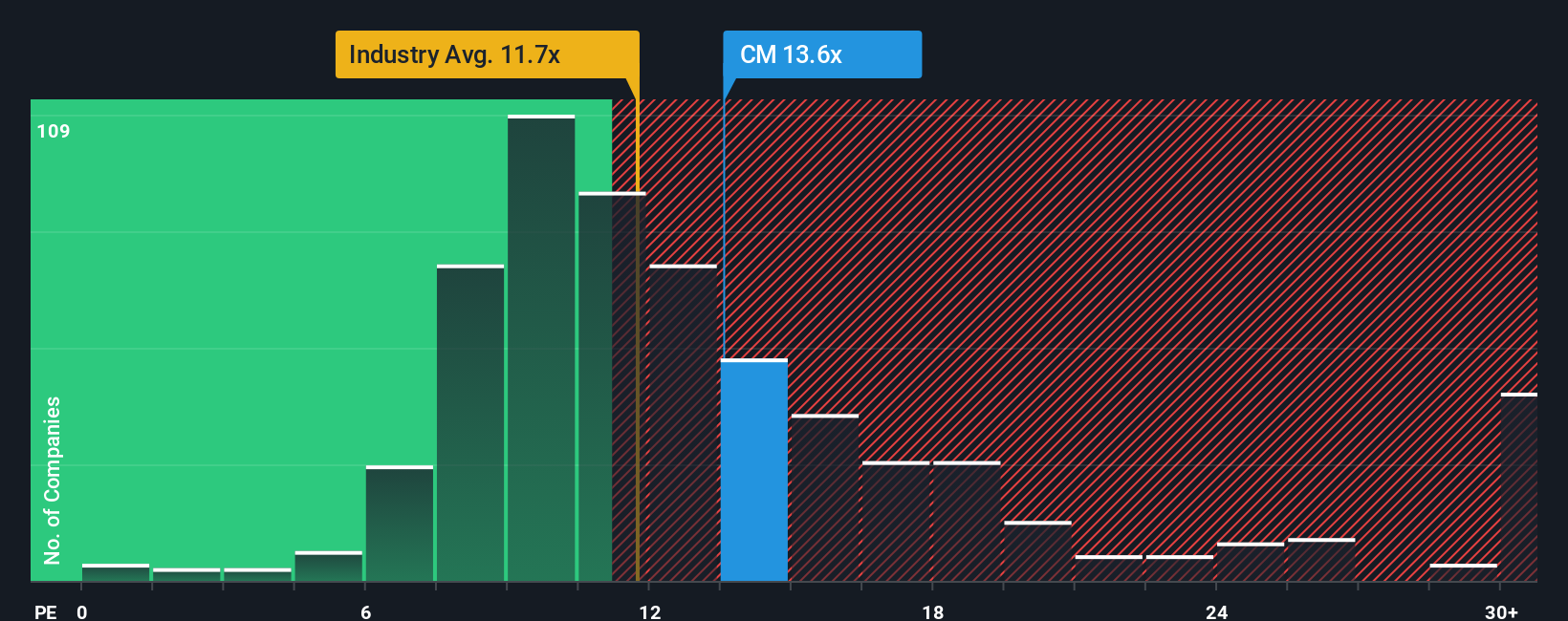

Another View: Market Ratios Tell A Different Story

On simple earnings ratios, Canadian Imperial Bank of Commerce looks less demanding, trading on 14.5 times earnings versus 15.2 times for peers, yet slightly above a 13.9 times fair ratio that the market could drift toward. Is that modest premium a warning sign or a reasonable price for quality?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Canadian Imperial Bank of Commerce Narrative

If you want to dig into the numbers yourself or take a different angle on the story, you can build a fresh narrative in just a few minutes, Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Canadian Imperial Bank of Commerce.

Ready for more investment ideas?

Do not stop with just one bank. Use the Simply Wall St Screener to uncover fresh opportunities other investors could overlook and keep your portfolio one step ahead.

- Supercharge your hunt for growth by scanning these 26 AI penny stocks that are turning artificial intelligence from buzzword into durable earnings power.

- Lock in potential income streams with these 12 dividend stocks with yields > 3% and build a portfolio that gets paid while you wait.

- Stay ahead of the next market narrative by tracking these 81 cryptocurrency and blockchain stocks shaping the evolution of digital assets and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CM

Canadian Imperial Bank of Commerce

A diversified financial institution, provides various financial products and services to personal, business, public sector, and institutional clients in Canada, the United States, and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026