One Ouro Fino Saúde Animal Participações S.A. (BVMF:OFSA3) Analyst Just Cut Their EPS Forecasts

Market forces rained on the parade of Ouro Fino Saúde Animal Participações S.A. (BVMF:OFSA3) shareholders today, when the covering analyst downgraded their forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analyst seeing grey clouds on the horizon.

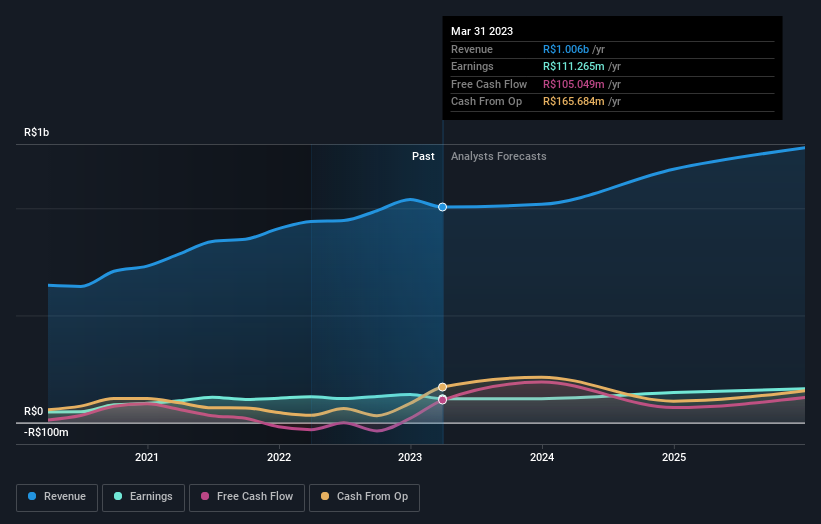

Following this downgrade, Ouro Fino Saúde Animal Participações' single analyst are forecasting 2023 revenues to be R$1.0b, approximately in line with the last 12 months. Statutory earnings per share are forecast to be R$2.07, approximately in line with the last 12 months. Previously, the analyst had been modelling revenues of R$1.2b and earnings per share (EPS) of R$2.70 in 2023. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a pretty serious decline to earnings per share numbers as well.

Check out our latest analysis for Ouro Fino Saúde Animal Participações

Despite the cuts to forecast earnings, there was no real change to the R$26.50 price target, showing that the analyst don't think the changes have a meaningful impact on its intrinsic value. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Ouro Fino Saúde Animal Participações at R$27.00 per share, while the most bearish prices it at R$26.00. Still, with such a tight range of estimates, it suggests the analyst has a pretty good idea of what they think the company is worth.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that Ouro Fino Saúde Animal Participações' revenue growth will slow down substantially, with revenues to the end of 2023 expected to display 1.7% growth on an annualised basis. This is compared to a historical growth rate of 14% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 7.5% annually. Factoring in the forecast slowdown in growth, it seems obvious that Ouro Fino Saúde Animal Participações is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Ouro Fino Saúde Animal Participações.

Unfortunately, by using these new estimates as a starting point, we've run a discounted cash flow calculation (DCF) on Ouro Fino Saúde Animal Participações that suggests the company could be somewhat overvalued. Learn why, and examine the assumptions that underpin our valuation by visiting our free platform here to learn more about our valuation approach.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you're looking to trade Ouro Fino Saúde Animal Participações, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:OFSA3

Ouro Fino Saúde Animal Participações

Engages in the development, production, and sale of veterinary drugs, vaccines, and other products for production and companion animals primarily in Brazil.

Flawless balance sheet and slightly overvalued.