Advertisement

- Brazil

- /

- Metals and Mining

- /

- BOVESPA:CBAV3

Investors Still Aren't Entirely Convinced By Companhia Brasileira de Alumínio's (BVMF:CBAV3) Revenues Despite 27% Price Jump

Companhia Brasileira de Alumínio (BVMF:CBAV3) shares have had a really impressive month, gaining 27% after a shaky period beforehand. But the last month did very little to improve the 54% share price decline over the last year.

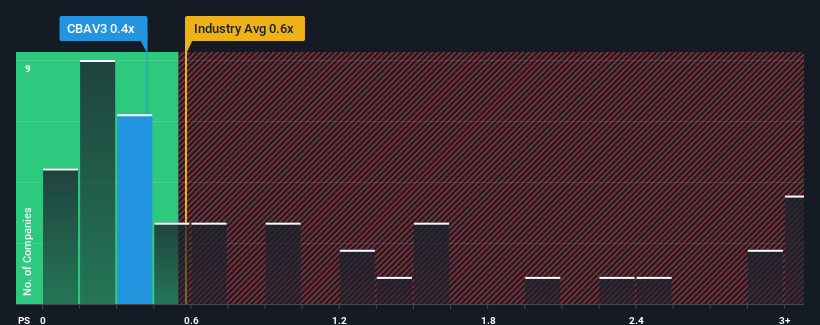

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Companhia Brasileira de Alumínio's P/S ratio of 0.4x, since the median price-to-sales (or "P/S") ratio for the Metals and Mining industry in Brazil is also close to 0.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Companhia Brasileira de Alumínio

What Does Companhia Brasileira de Alumínio's Recent Performance Look Like?

Recent times haven't been great for Companhia Brasileira de Alumínio as its revenue has been falling quicker than most other companies. Perhaps the market is expecting future revenue performance to begin matching the rest of the industry, which has kept the P/S from declining. You'd much rather the company improve its revenue if you still believe in the business. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Companhia Brasileira de Alumínio.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Companhia Brasileira de Alumínio's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 20%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 37% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Looking ahead now, revenue is anticipated to climb by 7.1% each year during the coming three years according to the six analysts following the company. With the industry only predicted to deliver 0.1% per annum, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that Companhia Brasileira de Alumínio's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Key Takeaway

Companhia Brasileira de Alumínio appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Despite enticing revenue growth figures that outpace the industry, Companhia Brasileira de Alumínio's P/S isn't quite what we'd expect. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. It appears some are indeed anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Before you take the next step, you should know about the 3 warning signs for Companhia Brasileira de Alumínio (2 are potentially serious!) that we have uncovered.

If these risks are making you reconsider your opinion on Companhia Brasileira de Alumínio, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:CBAV3

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor