Don't Buy Vulcabras S.A. (BVMF:VULC3) For Its Next Dividend Without Doing These Checks

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Vulcabras S.A. (BVMF:VULC3) is about to go ex-dividend in just 4 days. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Therefore, if you purchase Vulcabras' shares on or after the 22nd of April, you won't be eligible to receive the dividend, when it is paid on the 2nd of May.

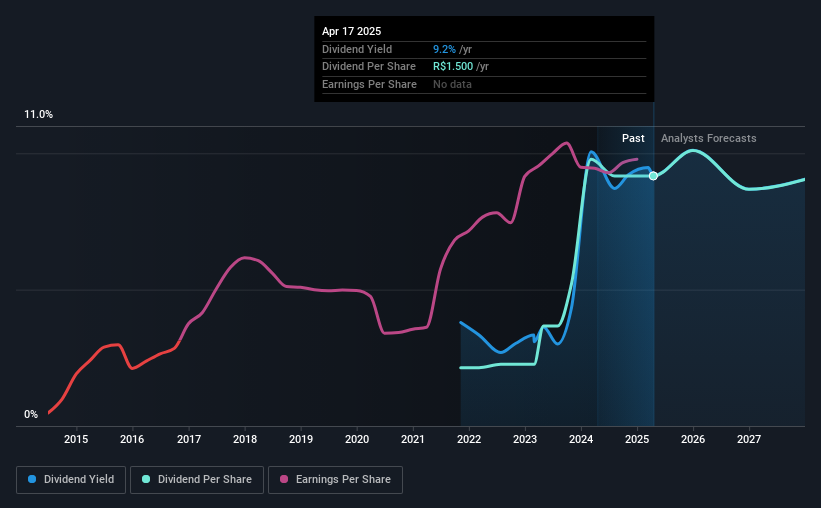

The company's next dividend payment will be R$0.125 per share, and in the last 12 months, the company paid a total of R$1.50 per share. Based on the last year's worth of payments, Vulcabras stock has a trailing yield of around 9.2% on the current share price of R$16.35. If you buy this business for its dividend, you should have an idea of whether Vulcabras's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

Our free stock report includes 1 warning sign investors should be aware of before investing in Vulcabras. Read for free now.Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Vulcabras distributed an unsustainably high 131% of its profit as dividends to shareholders last year. Without more sustainable payment behaviour, the dividend looks precarious. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out an unsustainably high 217% of its free cash flow as dividends over the past 12 months, which is worrying. Unless there were something in the business we're not grasping, this could signal a risk that the dividend may have to be cut in the future.

Cash is slightly more important than profit from a dividend perspective, but given Vulcabras's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

See our latest analysis for Vulcabras

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. It's encouraging to see Vulcabras has grown its earnings rapidly, up 29% a year for the past five years. Earnings per share have been growing rapidly, but the company is paying out a dividend that looks unsustainably high. Generally, when a company is paying out more than it earned as dividends, it could signal either that the company is spending heavily to fund its growth, or that earnings growth is likely to slow due to lack of reinvestment.

We'd also point out that Vulcabras issued a meaningful number of new shares in the past year. Trying to grow the dividend while issuing large amounts of new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past three years, Vulcabras has increased its dividend at approximately 62% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

Final Takeaway

Has Vulcabras got what it takes to maintain its dividend payments? Earnings per share have been growing, despite the company paying out a concerningly high percentage of its earnings and cashflow. We struggle to see how a company paying out so much of its earnings and cash flow will be able to sustain its dividend in a downturn, or reinvest enough into its business to continue growing earnings without borrowing heavily. It's not that we think Vulcabras is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

Although, if you're still interested in Vulcabras and want to know more, you'll find it very useful to know what risks this stock faces. For example, we've found 1 warning sign for Vulcabras that we recommend you consider before investing in the business.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

If you're looking to trade Vulcabras, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:VULC3

Vulcabras

Through its subsidiaries, operates as a footwear company in Brazil and internationally.

Solid track record with excellent balance sheet.

Market Insights

Community Narratives