- Brazil

- /

- Consumer Durables

- /

- BOVESPA:CYRE3

Many Still Looking Away From Cyrela Brazil Realty S.A. Empreendimentos e Participações (BVMF:CYRE3)

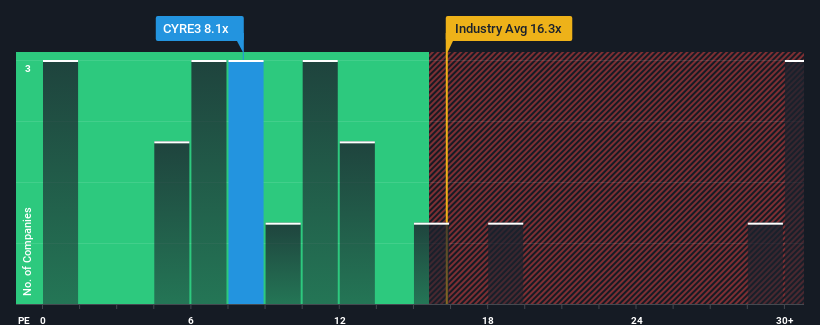

Cyrela Brazil Realty S.A. Empreendimentos e Participações' (BVMF:CYRE3) price-to-earnings (or "P/E") ratio of 8.1x might make it look like a buy right now compared to the market in Brazil, where around half of the companies have P/E ratios above 11x and even P/E's above 18x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Cyrela Brazil Realty Empreendimentos e Participações certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Cyrela Brazil Realty Empreendimentos e Participações

Does Growth Match The Low P/E?

Cyrela Brazil Realty Empreendimentos e Participações' P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 17% last year. Still, incredibly EPS has fallen 45% in total from three years ago, which is quite disappointing. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 18% per year during the coming three years according to the ten analysts following the company. With the market predicted to deliver 17% growth each year, the company is positioned for a comparable earnings result.

With this information, we find it odd that Cyrela Brazil Realty Empreendimentos e Participações is trading at a P/E lower than the market. It may be that most investors are not convinced the company can achieve future growth expectations.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Cyrela Brazil Realty Empreendimentos e Participações' analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

It is also worth noting that we have found 1 warning sign for Cyrela Brazil Realty Empreendimentos e Participações that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Cyrela Brazil Realty Empreendimentos e Participações, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:CYRE3

Cyrela Brazil Realty Empreendimentos e Participações

Develops and constructs residential properties in Brazil.

Undervalued with solid track record.

Market Insights

Community Narratives