Advertisement

- Brazil

- /

- Consumer Durables

- /

- BOVESPA:CYRE3

Is Cyrela Brazil Realty Empreendimentos e Participações (BVMF:CYRE3) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Cyrela Brazil Realty S.A. Empreendimentos e Participações (BVMF:CYRE3) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Cyrela Brazil Realty Empreendimentos e Participações

What Is Cyrela Brazil Realty Empreendimentos e Participações's Debt?

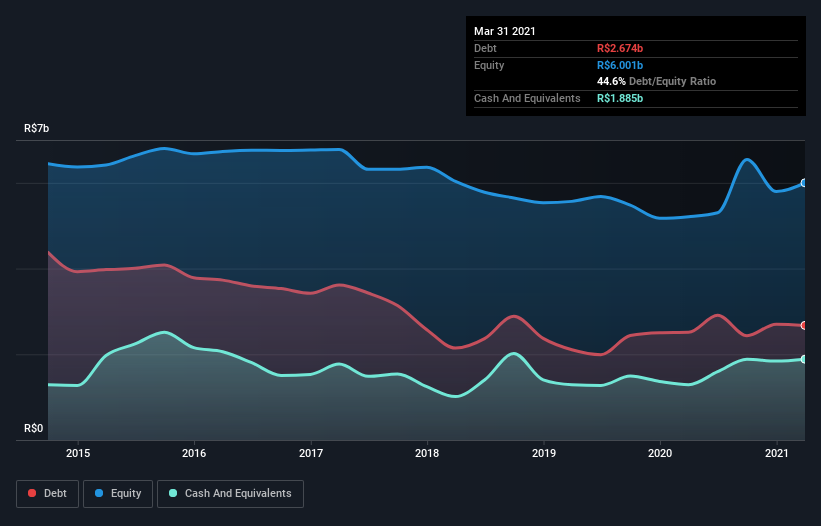

The image below, which you can click on for greater detail, shows that at March 2021 Cyrela Brazil Realty Empreendimentos e Participações had debt of R$2.67b, up from R$2.51b in one year. However, it also had R$1.89b in cash, and so its net debt is R$789.0m.

A Look At Cyrela Brazil Realty Empreendimentos e Participações' Liabilities

Zooming in on the latest balance sheet data, we can see that Cyrela Brazil Realty Empreendimentos e Participações had liabilities of R$2.21b due within 12 months and liabilities of R$3.45b due beyond that. Offsetting this, it had R$1.89b in cash and R$1.48b in receivables that were due within 12 months. So it has liabilities totalling R$2.29b more than its cash and near-term receivables, combined.

Cyrela Brazil Realty Empreendimentos e Participações has a market capitalization of R$8.58b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Cyrela Brazil Realty Empreendimentos e Participações has a low debt to EBITDA ratio of only 1.3. But the really cool thing is that it actually managed to receive more interest than it paid, over the last year. So there's no doubt this company can take on debt while staying cool as a cucumber. In addition to that, we're happy to report that Cyrela Brazil Realty Empreendimentos e Participações has boosted its EBIT by 56%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Cyrela Brazil Realty Empreendimentos e Participações can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Cyrela Brazil Realty Empreendimentos e Participações actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Cyrela Brazil Realty Empreendimentos e Participações's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Considering this range of factors, it seems to us that Cyrela Brazil Realty Empreendimentos e Participações is quite prudent with its debt, and the risks seem well managed. So the balance sheet looks pretty healthy, to us. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Cyrela Brazil Realty Empreendimentos e Participações (including 1 which makes us a bit uncomfortable) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BOVESPA:CYRE3

Cyrela Brazil Realty Empreendimentos e Participações

Develops and constructs residential properties in Brazil.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor