Advertisement

The recent 13% gain must have brightened CEO Stijn Van Rompay's week, Hyloris Pharmaceuticals SA's (EBR:HYL) most bullish insider

Key Insights

- Significant insider control over Hyloris Pharmaceuticals implies vested interests in company growth

- 50% of the business is held by the top 2 shareholders

- Using data from company's past performance alongside ownership research, one can better assess the future performance of a company

To get a sense of who is truly in control of Hyloris Pharmaceuticals SA (EBR:HYL), it is important to understand the ownership structure of the business. We can see that individual insiders own the lion's share in the company with 57% ownership. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

Clearly, insiders benefitted the most after the company's market cap rose by €20m last week.

Let's delve deeper into each type of owner of Hyloris Pharmaceuticals, beginning with the chart below.

Check out our latest analysis for Hyloris Pharmaceuticals

What Does The Lack Of Institutional Ownership Tell Us About Hyloris Pharmaceuticals?

We don't tend to see institutional investors holding stock of companies that are very risky, thinly traded, or very small. Though we do sometimes see large companies without institutions on the register, it's not particularly common.

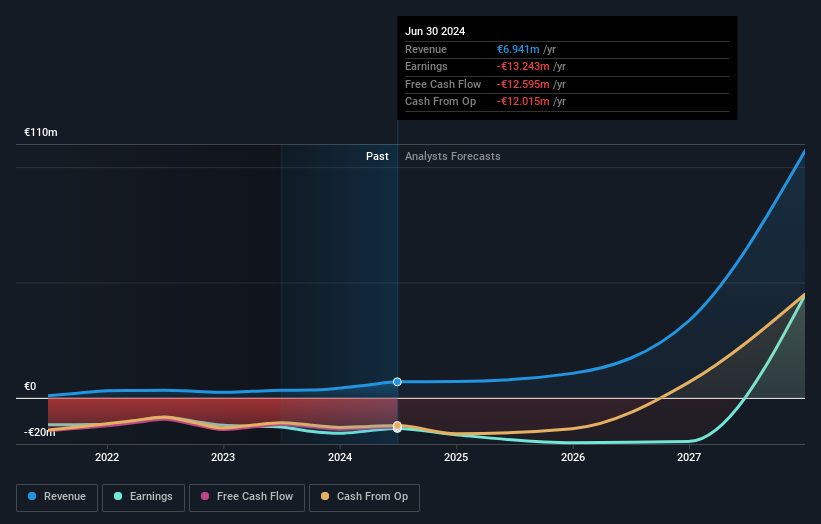

There could be various reasons why no institutions own shares in a company. Typically, small, newly listed companies don't attract much attention from fund managers, because it would not be possible for large fund managers to build a meaningful position in the company. On the other hand, it's always possible that professional investors are avoiding a company because they don't think it's the best place for their money. Hyloris Pharmaceuticals' earnings and revenue track record (below) may not be compelling to institutional investors -- or they simply might not have looked at the business closely.

We note that hedge funds don't have a meaningful investment in Hyloris Pharmaceuticals. The company's CEO Stijn Van Rompay is the largest shareholder with 37% of shares outstanding. Thomas Jacobsen is the second largest shareholder owning 14% of common stock, and Bart Versluys holds about 6.2% of the company stock. Interestingly, the second-largest shareholder, Thomas Jacobsen is also Co-Chief Executive Officer, again, pointing towards strong insider ownership amongst the company's top shareholders.

To make our study more interesting, we found that the top 2 shareholders have a majority ownership in the company, meaning that they are powerful enough to influence the decisions of the company.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. There is some analyst coverage of the stock, but it could still become more well known, with time.

Insider Ownership Of Hyloris Pharmaceuticals

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

It seems that insiders own more than half the Hyloris Pharmaceuticals SA stock. This gives them a lot of power. So they have a €83m stake in this €146m business. Most would argue this is a positive, showing strong alignment with shareholders. You can click here to see if those insiders have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 43% stake in the company, and hence can't easily be ignored. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Take risks for example - Hyloris Pharmaceuticals has 1 warning sign we think you should be aware of.

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Hyloris Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTBR:HYL

Hyloris Pharmaceuticals

Engages in the research, development, and manufacture of pharmaceutical products to address unmet medical needs.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor