Shareholders May Not Be So Generous With Superloop Limited's (ASX:SLC) CEO Compensation And Here's Why

Key Insights

- Superloop will host its Annual General Meeting on 16th of November

- Salary of AU$724.7k is part of CEO Paul Tyler's total remuneration

- The total compensation is similar to the average for the industry

- Over the past three years, Superloop's EPS fell by 4.9% and over the past three years, the total loss to shareholders 30%

The underwhelming share price performance of Superloop Limited (ASX:SLC) in the past three years would have disappointed many shareholders. Per share earnings growth is also lacking, despite revenue growth. In light of this performance, shareholders will have a chance to question the board in the upcoming AGM on 16th of November, where they can impact on future company performance by voting on resolutions, including executive compensation. We think shareholders may be cautious of approving a pay rise for the CEO at the moment, based on our analysis below.

See our latest analysis for Superloop

Comparing Superloop Limited's CEO Compensation With The Industry

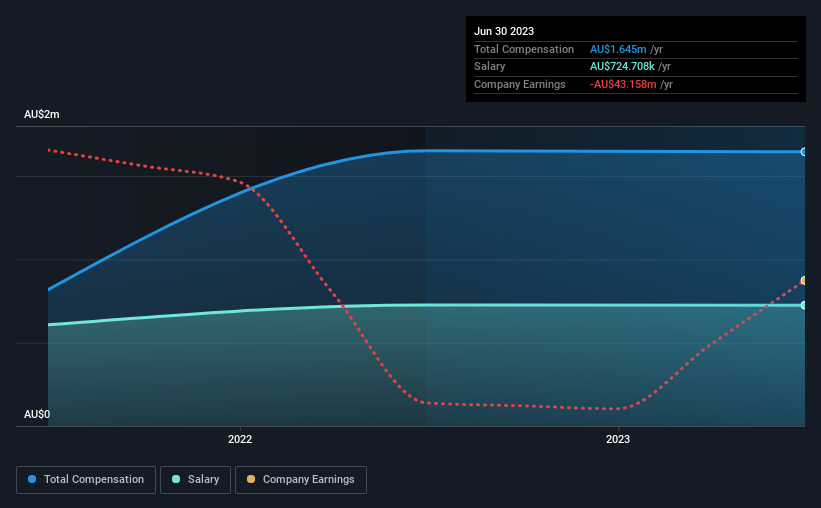

At the time of writing, our data shows that Superloop Limited has a market capitalization of AU$300m, and reported total annual CEO compensation of AU$1.6m for the year to June 2023. That is, the compensation was roughly the same as last year. While we always look at total compensation first, our analysis shows that the salary component is less, at AU$725k.

On examining similar-sized companies in the Australian Telecom industry with market capitalizations between AU$156m and AU$625m, we discovered that the median CEO total compensation of that group was AU$1.5m. So it looks like Superloop compensates Paul Tyler in line with the median for the industry. Moreover, Paul Tyler also holds AU$240k worth of Superloop stock directly under their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$725k | AU$726k | 44% |

| Other | AU$920k | AU$925k | 56% |

| Total Compensation | AU$1.6m | AU$1.7m | 100% |

On an industry level, around 45% of total compensation represents salary and 55% is other remuneration. Although there is a difference in how total compensation is set, Superloop more or less reflects the market in terms of setting the salary. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Superloop Limited's Growth Numbers

Superloop Limited has reduced its earnings per share by 4.9% a year over the last three years. It achieved revenue growth of 30% over the last year.

Investors would be a bit wary of companies that have lower EPS But in contrast the revenue growth is strong, suggesting future potential for EPS growth. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Superloop Limited Been A Good Investment?

Given the total shareholder loss of 30% over three years, many shareholders in Superloop Limited are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

The loss to shareholders over the past three years is certainly concerning and possibly has something to do with the fact that the company's earnings haven't grown. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 2 warning signs for Superloop that investors should be aware of in a dynamic business environment.

Important note: Superloop is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:SLC

Superloop

Operates as a telecommunications and internet service provider in Australia.

Excellent balance sheet and good value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)