As the Australian market experiences a positive close with the ASX 200 gaining 0.29% and sectors like Real Estate and Healthcare leading the way, investors are keeping a keen eye on economic indicators such as inflation, which remains a concern according to recent RBA minutes. In this context of cautious optimism, identifying high growth tech stocks involves looking for companies that demonstrate resilience and adaptability in an environment where interest rates remain unchanged and inflationary pressures persist.

Top 10 High Growth Tech Companies In Australia

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Pureprofile | 14.31% | 71.53% | ★★★★★☆ |

| Adherium | 86.80% | 73.66% | ★★★★★★ |

| Telix Pharmaceuticals | 21.55% | 38.32% | ★★★★★★ |

| ImExHS | 20.47% | 111.20% | ★★★★★★ |

| AVA Risk Group | 25.54% | 77.32% | ★★★★★★ |

| Pointerra | 56.62% | 126.45% | ★★★★★★ |

| Mesoblast | 45.80% | 62.77% | ★★★★★★ |

| Wrkr | 37.21% | 98.46% | ★★★★★★ |

| Opthea | 52.73% | 63.45% | ★★★★★★ |

| SiteMinder | 18.83% | 60.52% | ★★★★★☆ |

Click here to see the full list of 61 stocks from our ASX High Growth Tech and AI Stocks screener.

Let's uncover some gems from our specialized screener.

Codan (ASX:CDA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Codan Limited is a company that develops technology solutions for diverse clients including United Nations organizations, security and military groups, government departments, individuals, and small-scale miners, with a market cap of A$2.95 billion.

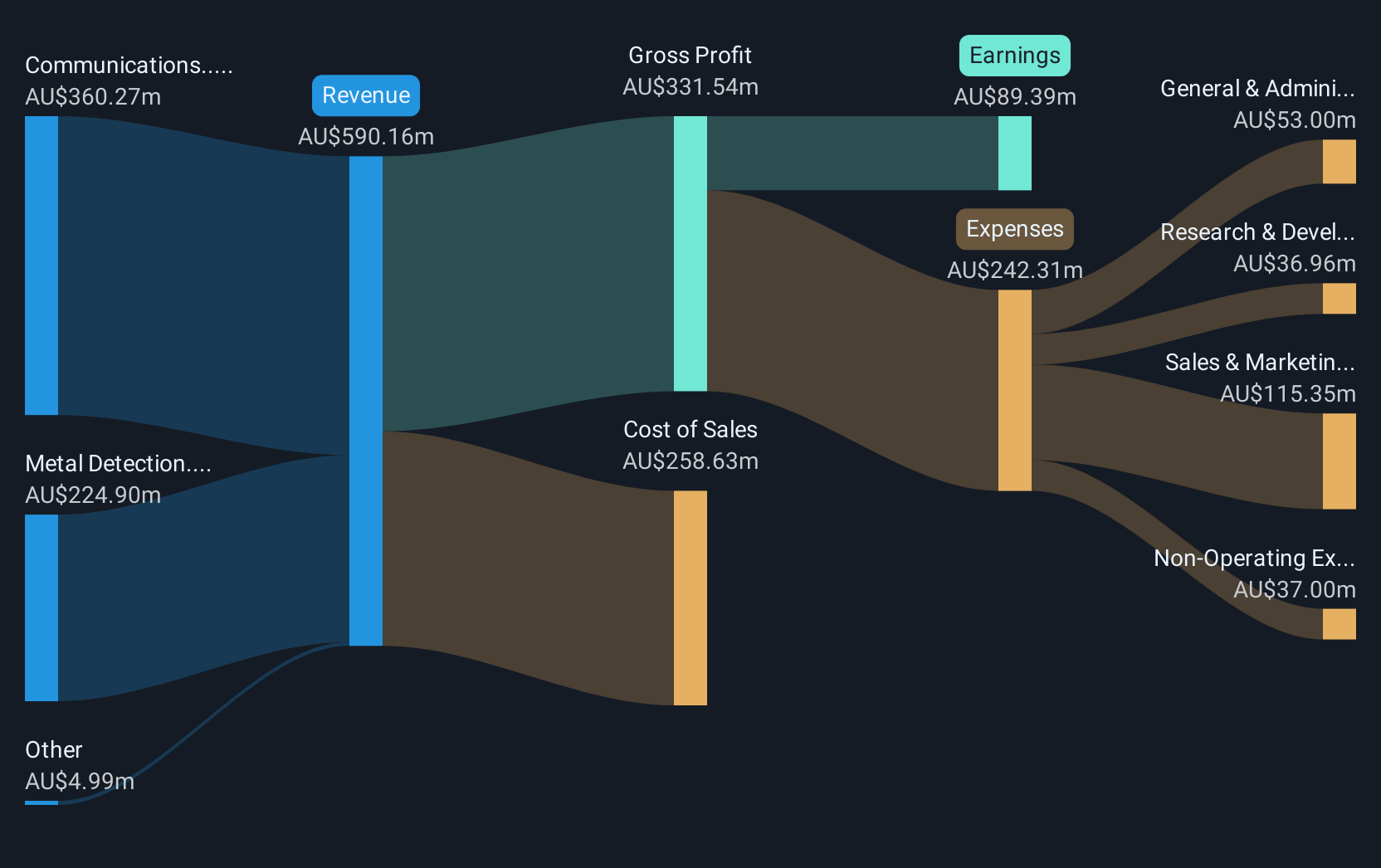

Operations: Codan generates revenue primarily from its Communications segment, contributing A$326.91 million, and Metal Detection segment, adding A$219.85 million.

Codan, an Australian tech firm, demonstrates robust growth metrics that are compelling within the high-growth technology sector. With a notable annual revenue increase of 10.6%, Codan outpaces the broader Australian market's average of 5.9%. This performance is complemented by an impressive earnings growth rate of 17.4% per year, significantly higher than the market average of 12.5%. The company’s commitment to innovation is evident in its R&D investments, crucial for maintaining technological leadership and supporting sustained financial health. Moreover, Codan's Return on Equity (ROE) is projected to reach an admirable 22.5% in three years, underscoring its efficient use of shareholder funds compared to industry benchmarks. These factors collectively underscore Codan’s potential in a competitive landscape and signal promising prospects for future growth.

- Click here and access our complete health analysis report to understand the dynamics of Codan.

Gain insights into Codan's past trends and performance with our Past report.

REA Group (ASX:REA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: REA Group Limited operates as an online property advertising company with a presence in Australia, India, the United States, Malaysia, Singapore, Thailand, Vietnam, and other international markets, with a market cap of approximately A$30.91 billion.

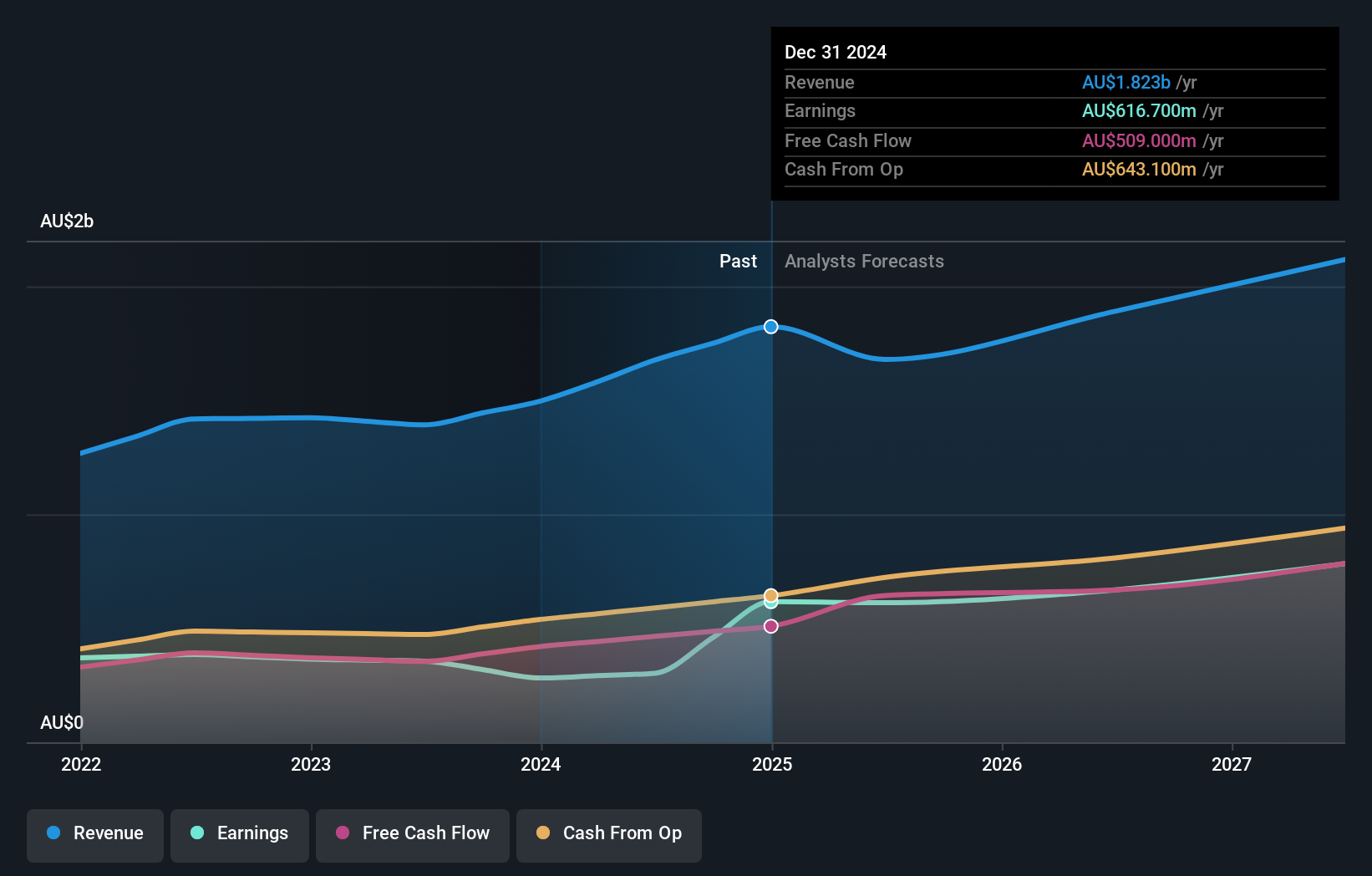

Operations: The company generates revenue primarily through its property and online advertising segment in Australia, contributing A$1.25 billion, followed by financial services in Australia at A$320.60 million, and operations in India at A$103.10 million. The business focuses on leveraging its digital platforms to offer advertising solutions across various international markets.

REA Group, a key player in Australia's technology sector, recently projected a revenue growth of 7.2% annually, outpacing the national average of 5.9%. This growth is supported by an anticipated earnings increase of 17.8% per year, significantly above the market norm of 12.5%. Despite facing challenges like a substantial one-off loss of A$153.6M last year, REA's robust forecast for Return on Equity at an impressive 32.8% in three years highlights its potential resilience and efficiency in capital utilization. The firm continues to innovate and adapt in the competitive Interactive Media and Services industry, promising dynamic future prospects despite past volatility.

- Unlock comprehensive insights into our analysis of REA Group stock in this health report.

Review our historical performance report to gain insights into REA Group's's past performance.

WiseTech Global (ASX:WTC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: WiseTech Global Limited develops and provides software solutions for the logistics execution industry across various regions, with a market cap of A$41.13 billion.

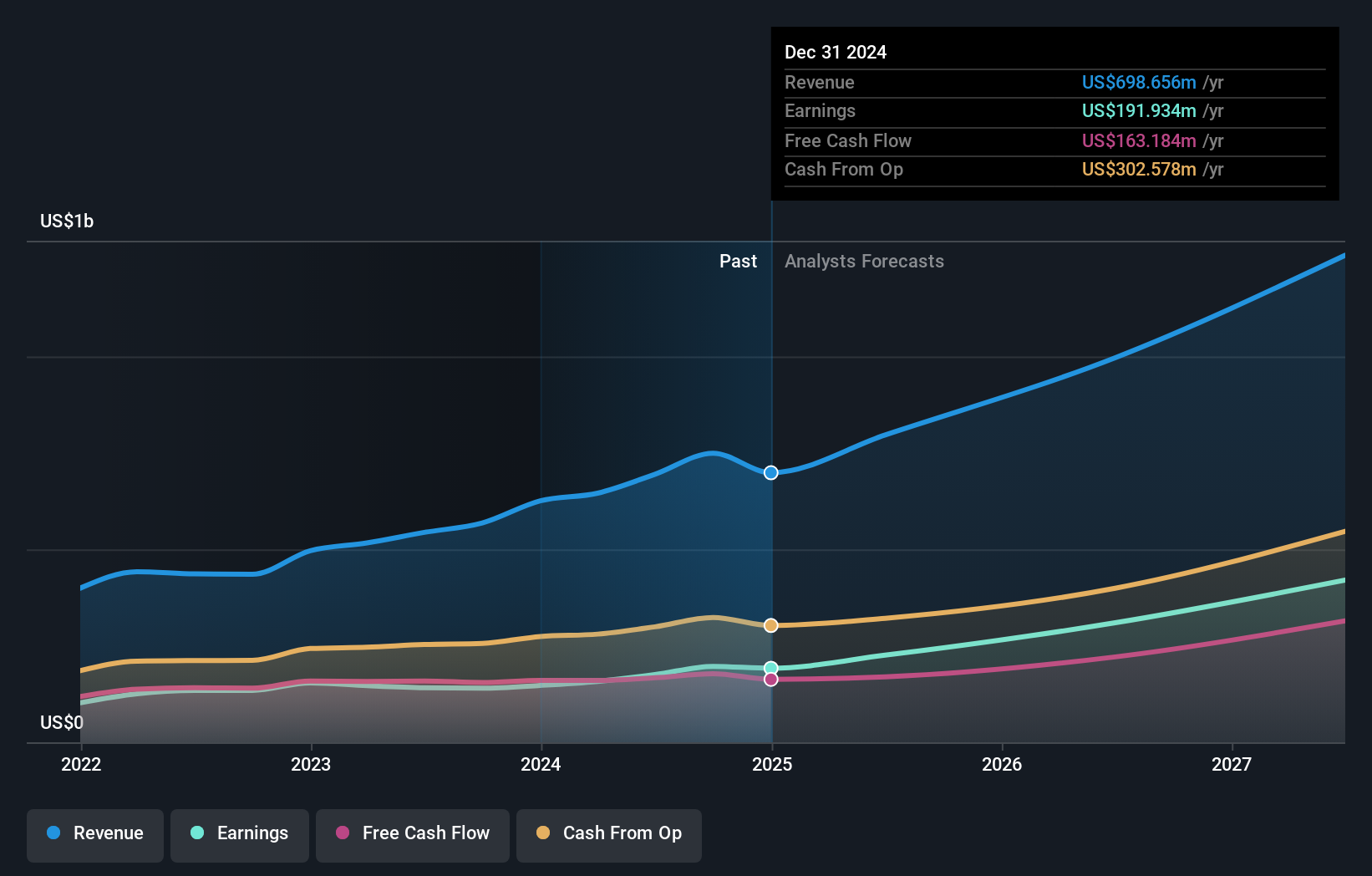

Operations: WiseTech Global Limited focuses on delivering software solutions for the logistics execution sector, generating revenue primarily from its Internet Software & Services segment, which amounts to A$1.04 billion.

WiseTech Global, an innovator in global logistics software, is poised for significant growth with its latest earnings forecast predicting a 24.1% increase annually, outstripping the broader Australian market's 12.5%. This robust projection is underpinned by a substantial investment in R&D, which amounted to A$150 million last year, representing over 15% of its total revenue. The company's strategic focus on enhancing its proprietary technology platform through continuous innovation ensures it remains at the forefront of the logistics software sector. Moreover, recent executive shifts signal a refreshed leadership strategy that could steer WiseTech towards new heights in operational efficiency and market expansion.

- Click here to discover the nuances of WiseTech Global with our detailed analytical health report.

Understand WiseTech Global's track record by examining our Past report.

Key Takeaways

- Discover the full array of 61 ASX High Growth Tech and AI Stocks right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WiseTech Global might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:WTC

WiseTech Global

Engages in the development and provision of software solutions to the logistics execution industry in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives