Advertisement

- Australia

- /

- Professional Services

- /

- ASX:CPU

What Does Computershare Limited's (ASX:CPU) Share Price Indicate?

Computershare Limited (ASX:CPU) received a lot of attention from a substantial price movement on the ASX over the last few months, increasing to AU$25.75 at one point, and dropping to the lows of AU$22.77. Some share price movements can give investors a better opportunity to enter into the stock, and potentially buy at a lower price. A question to answer is whether Computershare's current trading price of AU$24.45 reflective of the actual value of the large-cap? Or is it currently undervalued, providing us with the opportunity to buy? Let’s take a look at Computershare’s outlook and value based on the most recent financial data to see if there are any catalysts for a price change.

Check out our latest analysis for Computershare

What is Computershare worth?

Computershare is currently expensive based on my price multiple model, where I look at the company's price-to-earnings ratio in comparison to the industry average. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that Computershare’s ratio of 47.98x is above its peer average of 25.99x, which suggests the stock is trading at a higher price compared to the IT industry. Another thing to keep in mind is that Computershare’s share price is quite stable relative to the rest of the market, as indicated by its low beta. This means that if you believe the current share price should move towards the levels of its industry peers over time, a low beta could suggest it is not likely to reach that level anytime soon, and once it’s there, it may be hard for it to fall back down into an attractive buying range again.

What does the future of Computershare look like?

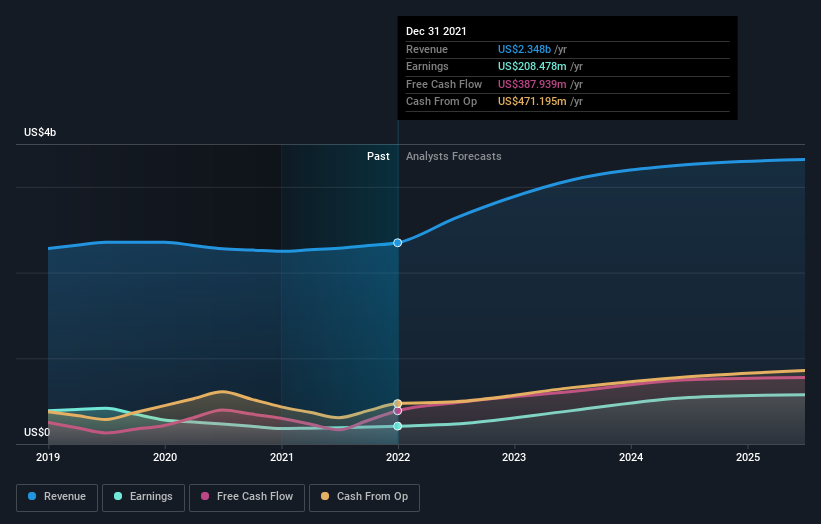

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Computershare's earnings over the next few years are expected to double, indicating a very optimistic future ahead. This should lead to stronger cash flows, feeding into a higher share value.

What this means for you:

Are you a shareholder? CPU’s optimistic future growth appears to have been factored into the current share price, with shares trading above industry price multiples. However, this brings up another question – is now the right time to sell? If you believe CPU should trade below its current price, selling high and buying it back up again when its price falls towards the industry PE ratio can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping an eye on CPU for a while, now may not be the best time to enter into the stock. The price has surpassed its industry peers, which means it is likely that there is no more upside from mispricing. However, the optimistic prospect is encouraging for CPU, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. For example, we've discovered 1 warning sign that you should run your eye over to get a better picture of Computershare.

If you are no longer interested in Computershare, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CPU

Computershare

Provides issuer, corporate trust, employee share plans and voucher, communication and utilities, technology and operations, and mortgage and property rental services.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

AN

andre_santos on Ferrari ·

Ferrari's Intrinsic and Historical Valuation

Fair Value:€243.5616.9% overvalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TI

TibiT on Costco Wholesale ·

Investment Thesis: Costco Wholesale (COST)

Fair Value:US$726.2934.6% overvalued

25 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3322.3% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will soar with €2.5 billion investments fueling future growth

Fair Value:₺475.5130.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

InvestingNurse on Lexaria Bioscience ·

Lexaria Bioscience's Breakthrough with DehydraTECH to Revolutionize Drug Delivery

Fair Value:US$5.5585.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AC

AceRoth on Sirios Resources ·

SIrios Resources (SOI) is significantly undervalued on a risk-adjusted basis.

Fair Value:CA$3.3593.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8231.0% undervalued

82 followersusers have followed this narrative

6 commentsusers have commented on this narrative

35 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3322.3% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.3% undervalued

1037 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

Trending Discussion

HO

Holger on IREN ·

<b>Reported:</b> Revenue growth: 2024 → 2025 sharp increase of approx. 165%. Assuming moderate annual growth of 40%, a fair value in three years would be approx. $170. Given the customer base and the story, this should be possible. I find the most valuable “property” particularly interesting, as it solves the electricity problem.

1

|0

HE

Hemingway on Aeva Technologies ·

NVDA+AEVA Agreement is a game changer for the AEVA stock even though it is just a partnership and does not have a roll out until 2028 (which means receivables as early as 2027, I would imagine) This agreement effectively moves the goal posts of profitability for AEVA much closer since this is in addition to the recent Forterra agreement, as well as the (just announced) European carmaker agreement (which is believed to be Mercedes-Benz). Underneath all of this, AEVA has a pre-existing agreement with Daimler truck. So business seems to be booming, especially with really big name brands…which tends to bring in more brand nanes (and more agreements/contracts/announcements, etc). This often creates more coverage from analysts (often with upside stock upgrades) that I believe will be occurring over the next 3 to 6 months (as professional traders/analysts often research for 2 to 3 months before initiating coverage of a new issue). Anyway, just my opinion , so please do your own due diligence. Disclaimer: I DO trade in this stock from time to time and I may have a position currently

0

|0

DO

doncarletto on Worldline ·

ok, if the downward trend keeps on people are distressed and cannot assess the general standing of this company. Yes, it plunged from about € 80 to 1 and a half. The personal losses and the general trend depict a detrimental development. However, the core figures of the decade long grown structure (WLN) is quite sound. Except they have far too many employees. A reduction would help, but is not so easy in France. This is a genuine case of restructuring a high tech company. It will take some 2 - 5 years. However, the firm itself and its business model is fine. The CEOs are attempting to get it on track. The valuation of the peer group can only help to image the possibilies and potentials of this enterprise. As the firm is thorougly probed and investigated, a wirecard case can be excluded. A range from 1.3 to 2 can be assumed as a bottom. Some turn around traders may see this as a decade chance.

0

|0