Advertisement

Companies Like WhiteHawk (ASX:WHK) Can Afford To Invest In Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should WhiteHawk (ASX:WHK) shareholders be worried about its cash burn? For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for WhiteHawk

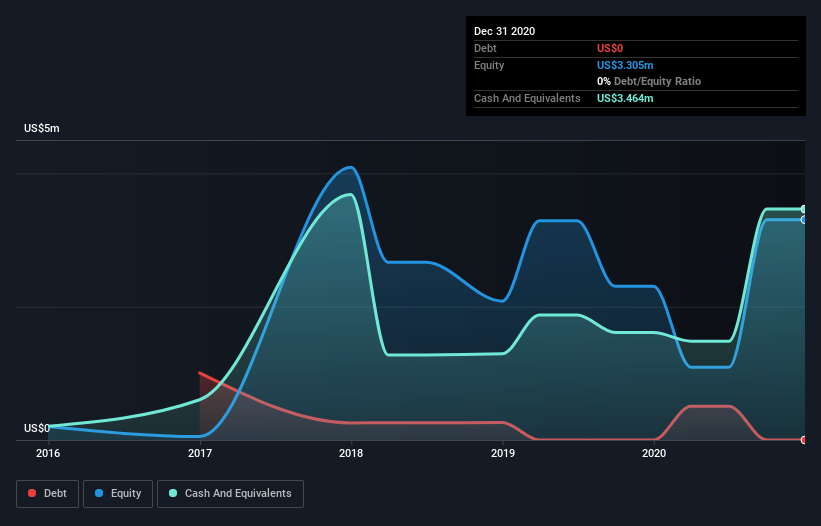

Does WhiteHawk Have A Long Cash Runway?

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. As at December 2020, WhiteHawk had cash of US$3.5m and no debt. Importantly, its cash burn was US$1.1m over the trailing twelve months. Therefore, from December 2020 it had 3.1 years of cash runway. A runway of this length affords the company the time and space it needs to develop the business. You can see how its cash balance has changed over time in the image below.

How Is WhiteHawk's Cash Burn Changing Over Time?

In our view, WhiteHawk doesn't yet produce significant amounts of operating revenue, since it reported just US$1.9m in the last twelve months. Therefore, for the purposes of this analysis we'll focus on how the cash burn is tracking. Even though it doesn't get us excited, the 42% reduction in cash burn year on year does suggest the company can continue operating for quite some time. Of course, we've only taken a quick look at the stock's growth metrics, here. You can take a look at how WhiteHawk is growing revenue over time by checking this visualization of past revenue growth.

How Easily Can WhiteHawk Raise Cash?

While WhiteHawk is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

WhiteHawk's cash burn of US$1.1m is about 3.9% of its US$28m market capitalisation. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

How Risky Is WhiteHawk's Cash Burn Situation?

As you can probably tell by now, we're not too worried about WhiteHawk's cash burn. For example, we think its cash runway suggests that the company is on a good path. Its cash burn reduction wasn't quite as good, but was still rather encouraging! Looking at all the measures in this article, together, we're not worried about its rate of cash burn, which seems to be under control. Taking a deeper dive, we've spotted 5 warning signs for WhiteHawk you should be aware of, and 1 of them is concerning.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you decide to trade WhiteHawk, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if WhiteHawk might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:WHK

WhiteHawk

Operates an online cybersecurity exchange platform of end-to-end Cyber Risk Software as a Service (SaaS) and Platform as a Service (PaaS) products and services in Australia and the United States.

Flawless balance sheet with moderate risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor