- Australia

- /

- Retail REITs

- /

- ASX:SCG

Scentre Group (ASX:SCG) Just Reported Annual Earnings: Have Analysts Changed Their Mind On The Stock?

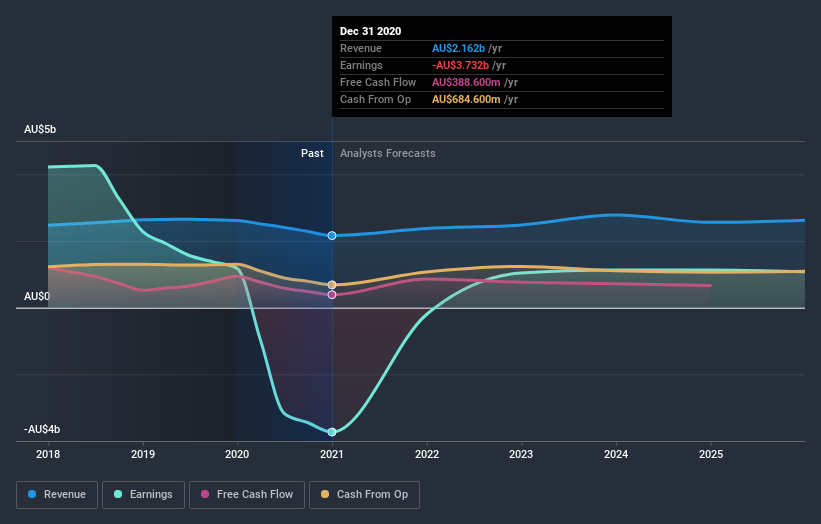

It's been a good week for Scentre Group (ASX:SCG) shareholders, because the company has just released its latest annual results, and the shares gained 7.7% to AU$2.93. Revenues of AU$2.2b beat expectations by a respectable 4.2%, although statutory losses per share increased. Scentre Group lost AU$0.72, which was 27% more than what the analysts had included in their models. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Scentre Group

Taking into account the latest results, the consensus forecast from Scentre Group's nine analysts is for revenues of AU$2.37b in 2021, which would reflect a notable 9.8% improvement in sales compared to the last 12 months. Earnings are expected to improve, with Scentre Group forecast to report a statutory profit of AU$0.075 per share. Before this earnings report, the analysts had been forecasting revenues of AU$2.40b and earnings per share (EPS) of AU$0.13 in 2021. The analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a large cut to EPS estimates.

The consensus price target held steady at AU$2.94, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Scentre Group analyst has a price target of AU$3.46 per share, while the most pessimistic values it at AU$2.11. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Of course, another way to look at these forecasts is to place them into context against the industry itself. One thing stands out from these estimates, which is that Scentre Group is forecast to grow faster in the future than it has in the past, with revenues expected to grow 9.8%. If achieved, this would be a much better result than the 2.6% annual decline over the past five years. Compare this against analyst estimates for the wider industry, which suggest that (in aggregate) industry revenues are expected to grow 1.2% next year. Not only are Scentre Group's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Scentre Group. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Scentre Group analysts - going out to 2025, and you can see them free on our platform here.

It is also worth noting that we have found 2 warning signs for Scentre Group (1 makes us a bit uncomfortable!) that you need to take into consideration.

If you decide to trade Scentre Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:SCG

Scentre Group

Owns and operates a leading portfolio of 42 Westfield destinations with 37 located in Australia and five in New Zealand encompassing more than 12,000 outlets.

Slight with limited growth.