- Australia

- /

- Hotel and Resort REITs

- /

- ASX:HPI

Hotel Property Investments' (ASX:HPI) Financials Are Too Obscure To Link With Current Share Price Momentum: What's In Store For the Stock?

Most readers would already know that Hotel Property Investments' (ASX:HPI) stock increased by 1.6% over the past month. However, the company's financials look a bit inconsistent and market outcomes are ultimately driven by long-term fundamentals, meaning that the stock could head in either direction. Specifically, we decided to study Hotel Property Investments' ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Hotel Property Investments

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hotel Property Investments is:

9.5% = AU$50m ÷ AU$534m (Based on the trailing twelve months to December 2020).

The 'return' is the income the business earned over the last year. Another way to think of that is that for every A$1 worth of equity, the company was able to earn A$0.09 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Hotel Property Investments' Earnings Growth And 9.5% ROE

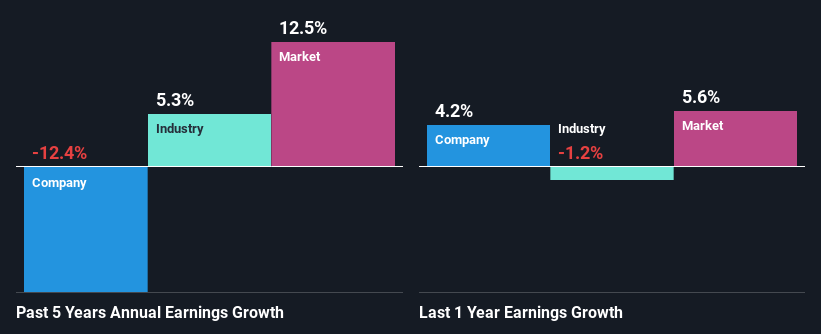

When you first look at it, Hotel Property Investments' ROE doesn't look that attractive. Although a closer study shows that the company's ROE is higher than the industry average of 6.7% which we definitely can't overlook. But seeing Hotel Property Investments' five year net income decline of 12% over the past five years, we might rethink that. Bear in mind, the company does have a slightly low ROE. It is just that the industry ROE is lower. Hence, this goes some way in explaining the shrinking earnings.

However, when we compared Hotel Property Investments' growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 5.3% in the same period. This is quite worrisome.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is HPI fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Hotel Property Investments Making Efficient Use Of Its Profits?

Hotel Property Investments seems to be paying out most of its income as dividends judging by its three-year median payout ratio of 52% (meaning, the company retains only 48% of profits). However, this is typical for REITs as they are often required by law to distribute most of their earnings. Accordingly, this likely explains why its earnings have been shrinking.

Additionally, Hotel Property Investments has paid dividends over a period of seven years, which means that the company's management is rather focused on keeping up its dividend payments, regardless of the shrinking earnings. Our latest analyst data shows that the future payout ratio of the company is expected to rise to 98% over the next three years. Consequently, the higher expected payout ratio explains the decline in the company's expected ROE (to 6.4%) over the same period.

Summary

In total, we're a bit ambivalent about Hotel Property Investments' performance. Specifically, the low earnings growth is a bit concerning, especially given that the company has a respectable rate of return. Investors may have benefitted, had the company been reinvesting more of its earnings. As discussed earlier, the company is retaining a small portion of its profits. Having said that, we studied the latest analyst forecasts, and found that analysts are expecting the company's earnings growth to improve slightly. This could offer some relief to the company's existing shareholders. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you decide to trade Hotel Property Investments, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hotel Property Investments might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:HPI

Hotel Property Investments

HPI owns a Portfolio of freehold hotels and associated specialty tenancies located throughout Queensland and South Australia.

Established dividend payer and fair value.

Market Insights

Community Narratives