Advertisement

Charter Hall Group And Two ASX Dividend Stocks To Consider For Your Portfolio

Simply Wall St

Reviewed by Simply Wall St

Over the past year, the Australian market has shown a robust increase of 11%, despite remaining flat in the last seven days. In this stable yet growing environment, dividend stocks like Charter Hall Group can be appealing for their potential to provide steady income and benefit from anticipated earnings growth of 13% per annum.

Top 10 Dividend Stocks In Australia

| Name | Dividend Yield | Dividend Rating |

| Nick Scali (ASX:NCK) | 5.31% | ★★★★★☆ |

| Collins Foods (ASX:CKF) | 3.13% | ★★★★★☆ |

| Centuria Capital Group (ASX:CNI) | 7.44% | ★★★★★☆ |

| Eagers Automotive (ASX:APE) | 7.32% | ★★★★★☆ |

| Fiducian Group (ASX:FID) | 4.09% | ★★★★★☆ |

| Fortescue (ASX:FMG) | 9.04% | ★★★★★☆ |

| Charter Hall Group (ASX:CHC) | 3.91% | ★★★★★☆ |

| Premier Investments (ASX:PMV) | 4.53% | ★★★★★☆ |

| Diversified United Investment (ASX:DUI) | 3.12% | ★★★★★☆ |

| New Hope (ASX:NHC) | 8.51% | ★★★★☆☆ |

Click here to see the full list of 27 stocks from our Top ASX Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

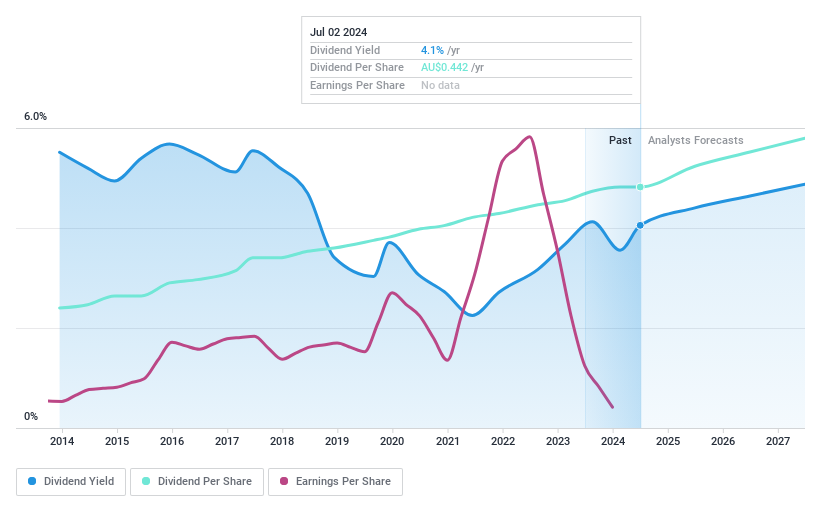

Charter Hall Group (ASX:CHC)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Charter Hall Group, operating in Australia, is a prominent property investment and funds management group with a market capitalization of approximately A$5.26 billion.

Operations: Charter Hall Group generates revenue primarily through funds management, which brought in A$515.60 million, and property investments, contributing A$142.20 million.

Dividend Yield: 3.9%

Charter Hall Group offers a relatively modest dividend yield of 3.91%, lower than the top quartile of Australian dividend stocks. Despite this, its dividends are well-supported, with a payout ratio of 43.8% and a cash payout ratio of 45.3%, indicating sustainability from both earnings and cash flow perspectives. Dividends have shown stability and growth over the past decade, although profit margins have declined year-over-year from 42.9% to 11.7%. The stock is currently trading at a significant discount to estimated fair value, suggesting potential for valuation adjustment.

- Delve into the full analysis dividend report here for a deeper understanding of Charter Hall Group.

- The analysis detailed in our Charter Hall Group valuation report hints at an inflated share price compared to its estimated value.

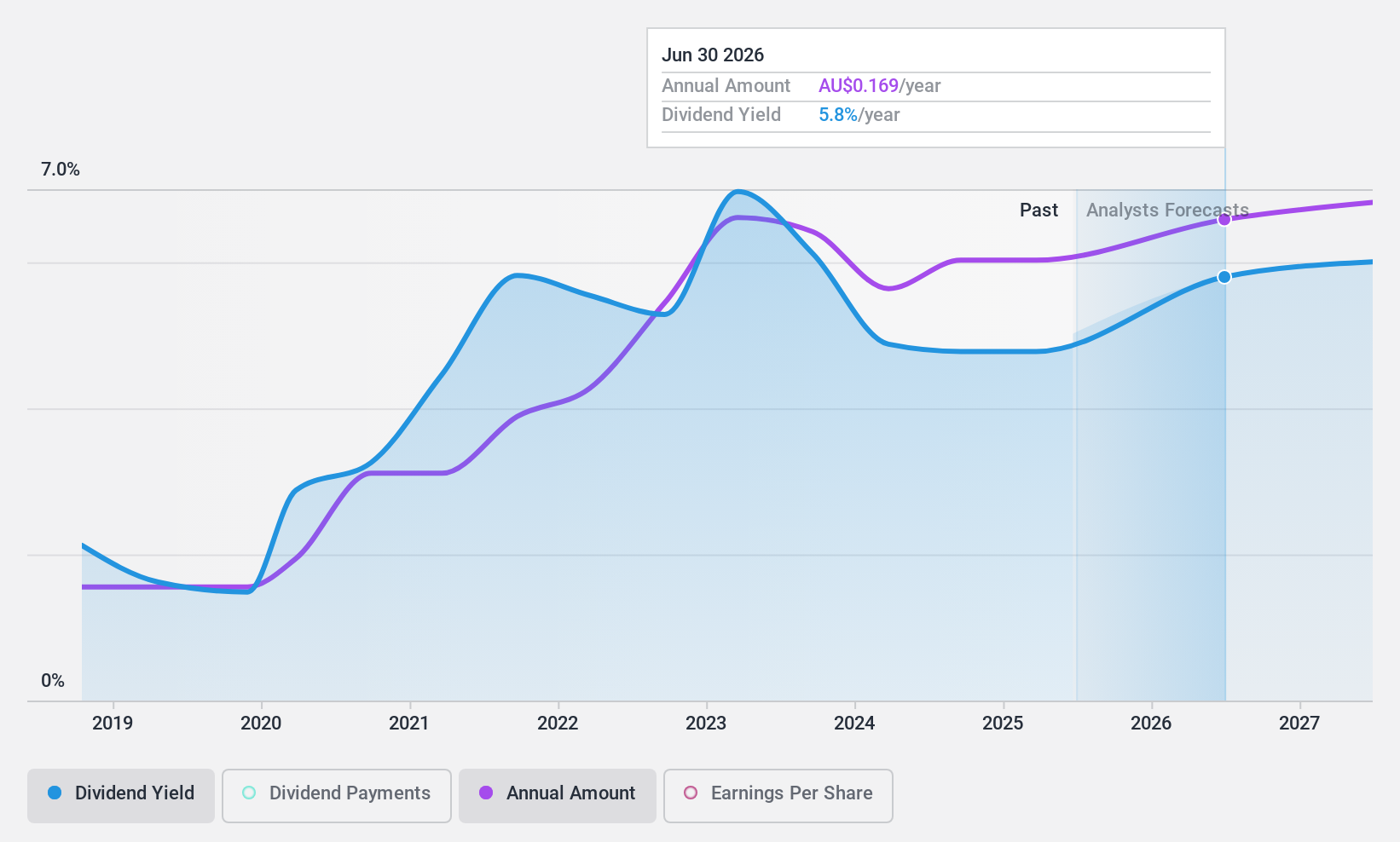

NRW Holdings (ASX:NWH)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: NRW Holdings Limited operates in Australia, offering a range of contract services to the resources and infrastructure sectors with a market capitalization of approximately A$1.38 billion.

Operations: NRW Holdings Limited generates revenue primarily through three segments: MET, which brought in A$739.07 million, Civil at A$593.62 million, and Mining, contributing A$1.49 billion.

Dividend Yield: 4.7%

NRW Holdings presents a mixed scenario for dividend investors. With a dividend yield of 4.74%, it falls below the top tier in the Australian market, yet its dividends are adequately covered by both earnings and cash flows, with payout ratios of 74% and 68.6% respectively. However, the company's dividend history has shown volatility over the past decade, despite an annual earnings growth of 15.8%. Additionally, NRW is trading at a 30.7% discount to its estimated fair value, suggesting potential undervaluation.

- Click to explore a detailed breakdown of our findings in NRW Holdings' dividend report.

- The analysis detailed in our NRW Holdings valuation report hints at an deflated share price compared to its estimated value.

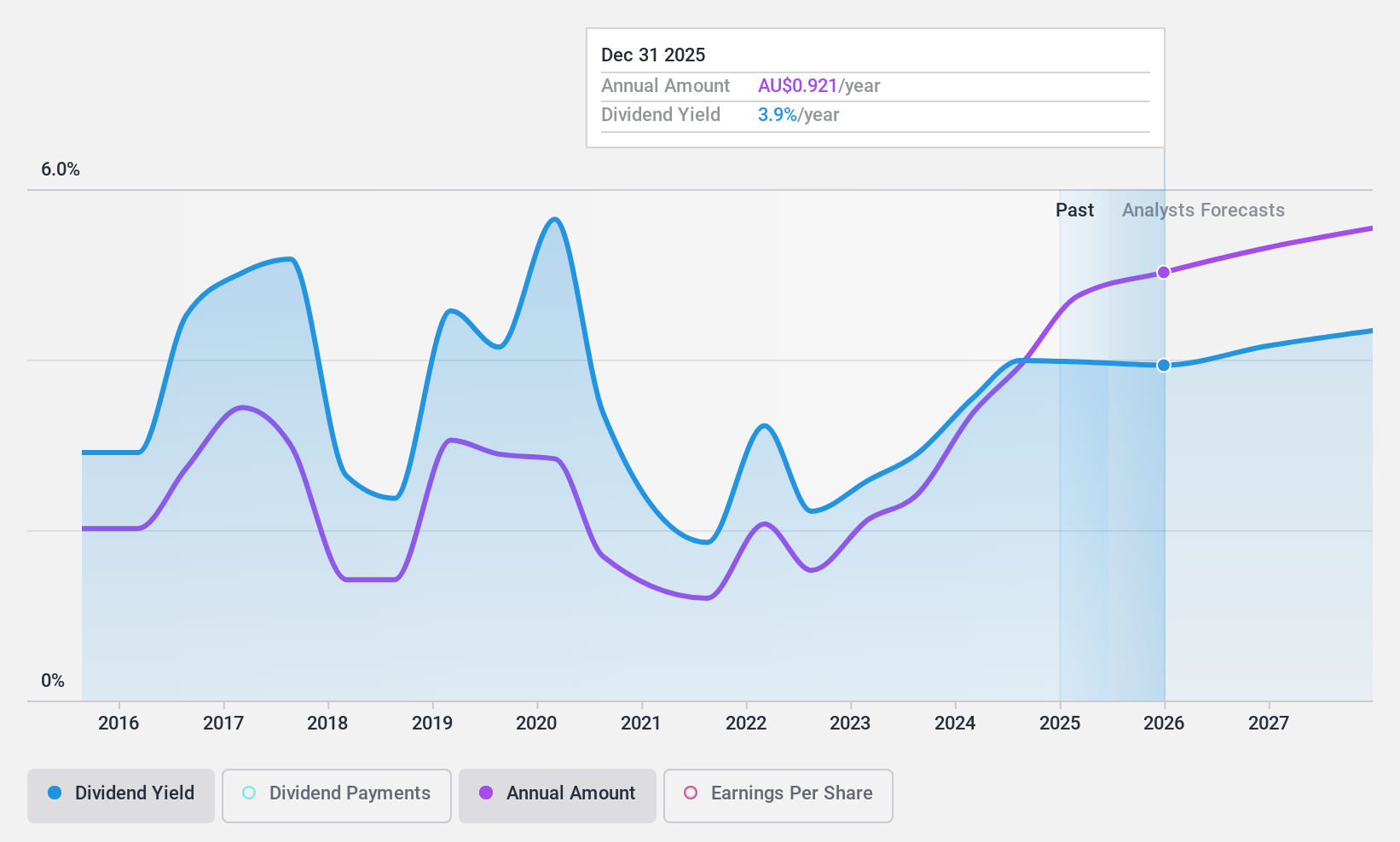

QBE Insurance Group (ASX:QBE)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: QBE Insurance Group Limited is a global insurer and reinsurer that operates in the Australia Pacific, North America, and other international markets, with a market capitalization of A$25.20 billion.

Operations: QBE Insurance Group Limited generates revenue through its operations in the Australia Pacific (A$5.97 billion), North America (A$11.12 billion), and internationally (A$9.56 billion).

Dividend Yield: 3.5%

QBE Insurance Group has demonstrated a fluctuating dividend history over the past decade, with recent years showing improvements. The current dividend yield stands at 3.48%, which is below the Australian market's top quartile of 6.54%. Despite this, QBE maintains a healthy payout ratio of 48.3% and a cash payout ratio of 44.7%, indicating that its dividends are well-supported by both earnings and cash flows. Additionally, QBE's earnings have grown by 143% this past year and are projected to increase annually by 6.47%. Recent board changes and a focus on sustainability may influence future governance and operations.

- Click here to discover the nuances of QBE Insurance Group with our detailed analytical dividend report.

- Our valuation report here indicates QBE Insurance Group may be undervalued.

Make It Happen

- Reveal the 27 hidden gems among our Top ASX Dividend Stocks screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if QBE Insurance Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:QBE

QBE Insurance Group

Engages in underwriting general insurance and reinsurance risks in the Australia Pacific, North America, and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|6.7% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|23.9% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|33.6% undervalued

DZ

Community Contributor