Advertisement

The Australian market recently saw a positive uptick, with the ASX closing up 0.7% at 7,999 points, driven by strong performances in sectors like Staples and Real Estate. In this environment of mixed sector outcomes, identifying undervalued stocks can be crucial for investors seeking opportunities; these are stocks that may not reflect their true potential value despite broader market movements.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Acrow (ASX:ACF) | A$1.10 | A$2.00 | 45% |

| Nido Education (ASX:NDO) | A$0.825 | A$1.58 | 47.9% |

| Domino's Pizza Enterprises (ASX:DMP) | A$27.01 | A$51.44 | 47.5% |

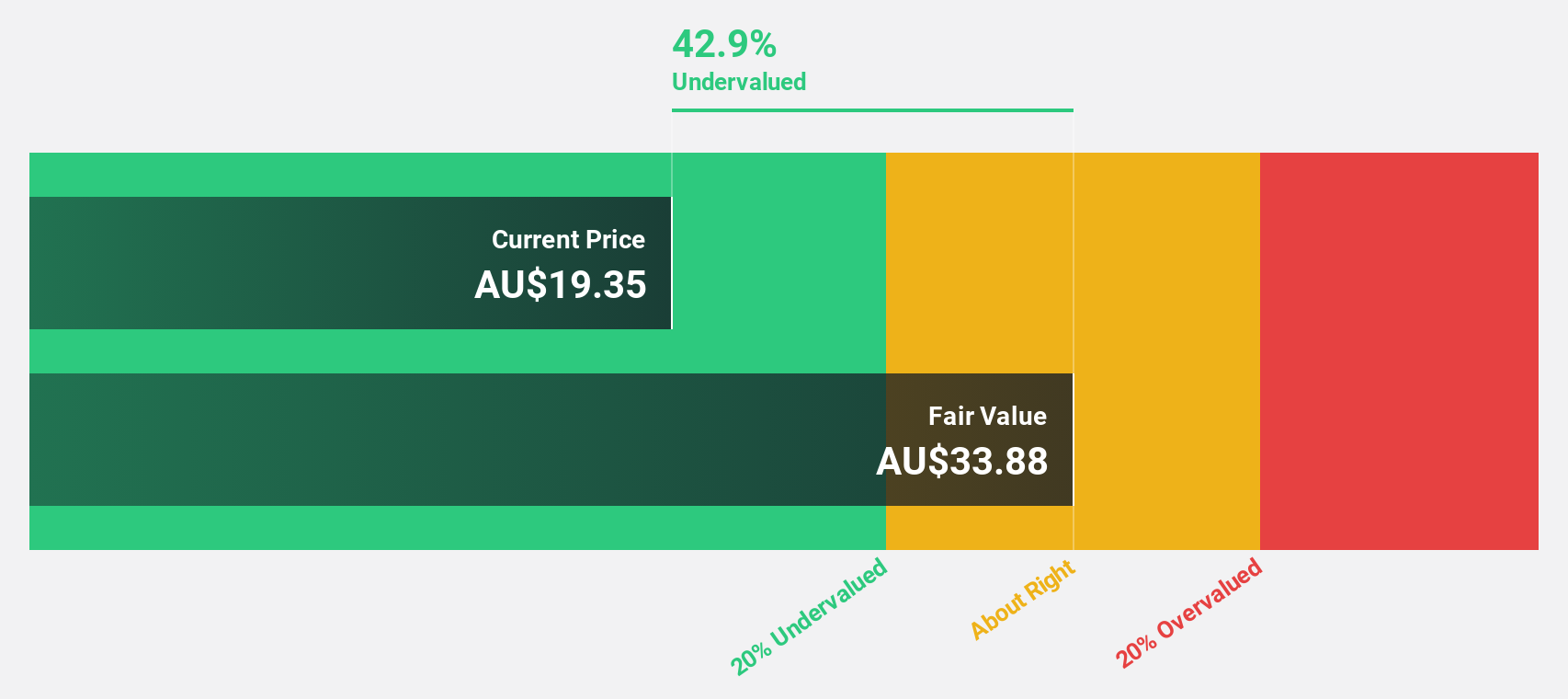

| Champion Iron (ASX:CIA) | A$5.26 | A$9.22 | 42.9% |

| South32 (ASX:S32) | A$3.51 | A$6.36 | 44.8% |

| Charter Hall Group (ASX:CHC) | A$17.06 | A$31.92 | 46.5% |

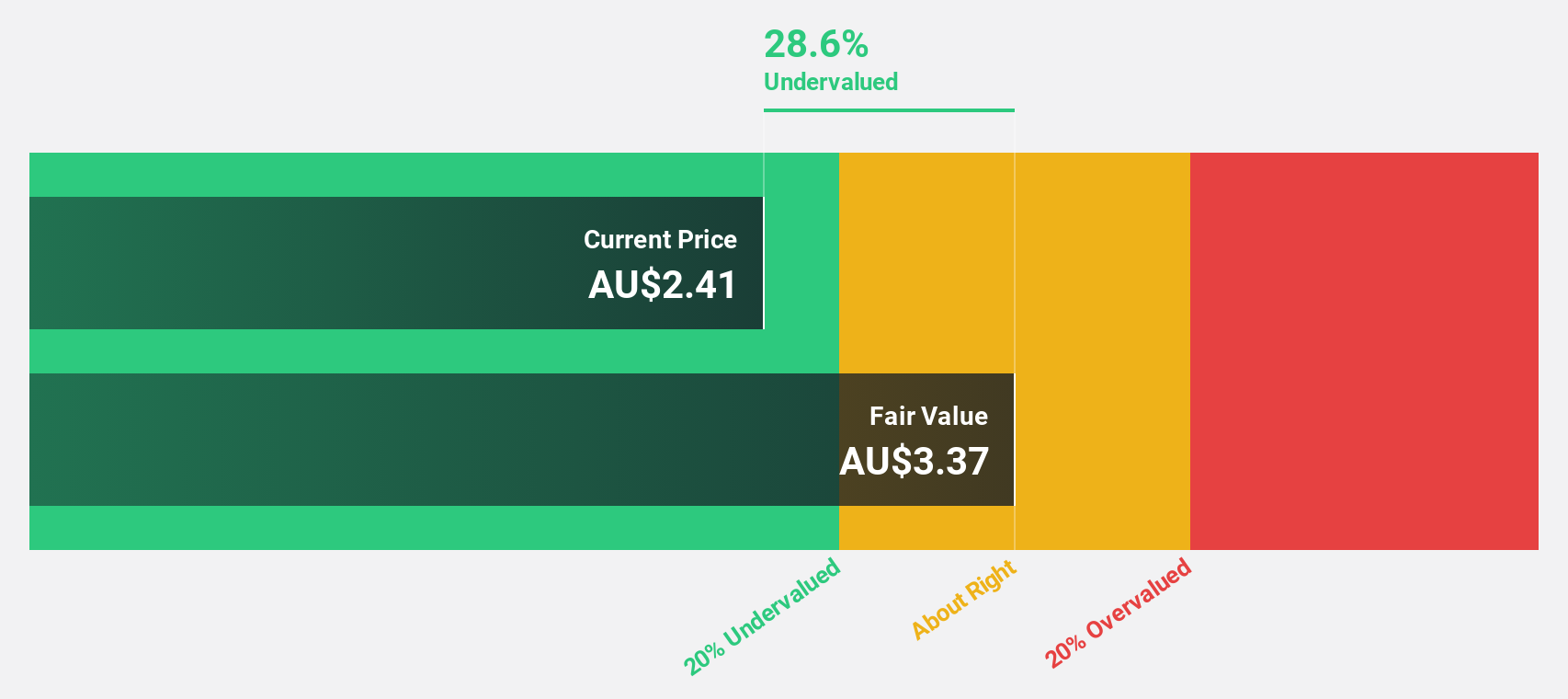

| SciDev (ASX:SDV) | A$0.465 | A$0.81 | 42.9% |

| PointsBet Holdings (ASX:PBH) | A$1.075 | A$2.15 | 49.9% |

| ReadyTech Holdings (ASX:RDY) | A$2.60 | A$5.07 | 48.7% |

| Sandfire Resources (ASX:SFR) | A$11.23 | A$20.51 | 45.3% |

We're going to check out a few of the best picks from our screener tool.

Charter Hall Group (ASX:CHC)

Overview: Charter Hall Group is a prominent Australian fully integrated property investment and funds management company with a market capitalization of A$8.01 billion.

Operations: The company's revenue is derived from three primary segments: Funds Management (A$441.60 million), Property Investments (A$332.50 million), and Development Investments (A$45.30 million).

Estimated Discount To Fair Value: 46.5%

Charter Hall Group is trading at A$17.06, significantly below its estimated fair value of A$31.92, indicating it may be undervalued based on cash flows. The company reported strong net income growth for the half year ended December 2024, with earnings per share from continuing operations more than doubling compared to the previous year. Despite slower revenue growth forecasts of 13.4% annually, Charter Hall offers a reliable dividend yield and has upgraded its FY25 earnings guidance to 81 cents per security.

- Insights from our recent growth report point to a promising forecast for Charter Hall Group's business outlook.

- Navigate through the intricacies of Charter Hall Group with our comprehensive financial health report here.

National Storage REIT (ASX:NSR)

Overview: National Storage REIT is the largest self-storage provider in Australia and New Zealand, operating over 225 centers and serving more than 90,000 residential and commercial customers, with a market cap of A$3.05 billion.

Operations: The company's revenue segment consists of A$369.99 million from the operation and management of storage centres.

Estimated Discount To Fair Value: 37.9%

National Storage REIT is trading at A$2.22, well below its fair value estimate of A$3.57, reflecting potential undervaluation based on cash flows. Despite a decline in net income to A$9.5 million for the half year ending December 2024 from A$16.7 million previously, earnings are expected to grow significantly at 21.2% annually, outpacing the Australian market's growth rate of 12%. However, debt coverage by operating cash flow remains a concern amidst lower profit margins and large one-off items impacting results.

- According our earnings growth report, there's an indication that National Storage REIT might be ready to expand.

- Click here to discover the nuances of National Storage REIT with our detailed financial health report.

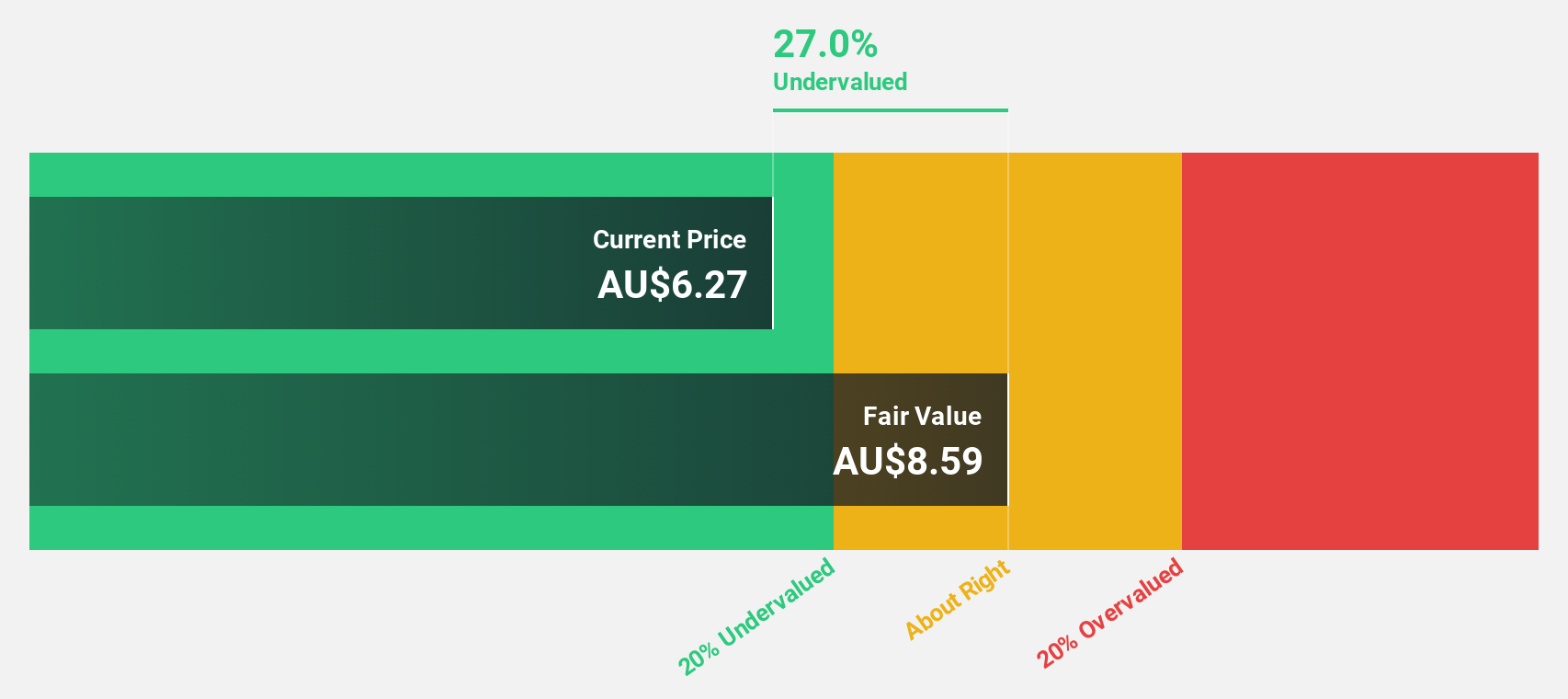

PWR Holdings (ASX:PWH)

Overview: PWR Holdings Limited specializes in the design, production, and sale of cooling products and solutions across various international markets, with a market cap of A$705.96 million.

Operations: PWR Holdings generates revenue from two main segments: PWR C&R, which contributes A$46.48 million, and PWR Performance Products, accounting for A$109.04 million.

Estimated Discount To Fair Value: 14.8%

PWR Holdings, trading at A$7.05, is below its fair value estimate of A$8.28, suggesting potential undervaluation based on cash flows. Despite a recent decline in net income to A$4.08 million for the half year ending December 2024 from A$9.78 million previously, earnings are expected to grow significantly at 24.2% annually, outpacing the broader Australian market's growth rate of 12%. However, revenue growth remains moderate and dividend payments have decreased recently.

- Our growth report here indicates PWR Holdings may be poised for an improving outlook.

- Click to explore a detailed breakdown of our findings in PWR Holdings' balance sheet health report.

Key Takeaways

- Click through to start exploring the rest of the 37 Undervalued ASX Stocks Based On Cash Flows now.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CHC

Charter Hall Group

Charter Hall is one of Australia’s leading fully integrated property investment and funds management groups.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor