Advertisement

Investors bid Orthocell (ASX:OCC) up AU$53m despite increasing losses YoY, taking one-year return to 347%

For many, the main point of investing in the stock market is to achieve spectacular returns. While not every stock performs well, when investors win, they can win big. For example, the Orthocell Limited (ASX:OCC) share price is up a whopping 347% in the last 1 year, a handsome return in a single year. Also pleasing for shareholders was the 166% gain in the last three months. And shareholders have also done well over the long term, with an increase of 310% in the last three years.

Since it's been a strong week for Orthocell shareholders, let's have a look at trend of the longer term fundamentals.

View our latest analysis for Orthocell

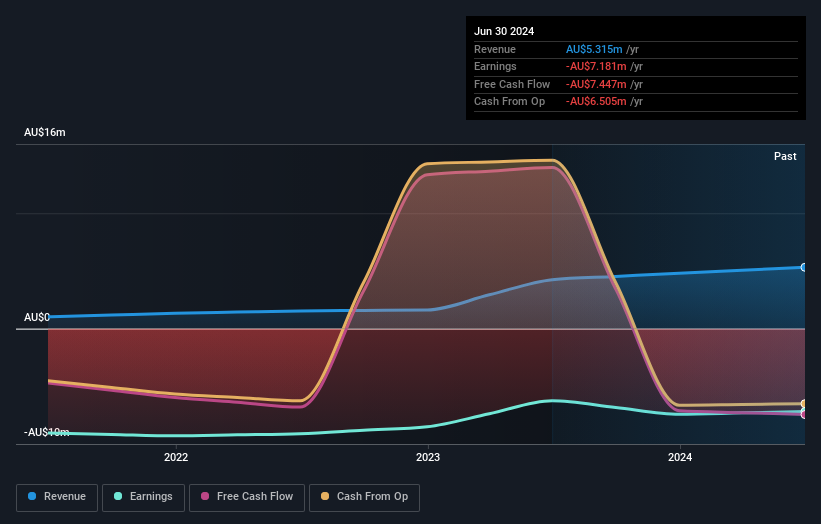

Because Orthocell made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. When a company doesn't make profits, we'd generally hope to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

Orthocell grew its revenue by 25% last year. We respect that sort of growth, no doubt. But the market is even more excited about it, with the price apparently bound for the moon, up 347% in one of earth's orbits. We're always cautious when the share price is up so much, but there's certainly enough revenue growth to justify taking a closer look at Orthocell.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. It's always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. Before buying or selling a stock, we always recommend a close examination of historic growth trends, available here..

A Different Perspective

It's good to see that Orthocell has rewarded shareholders with a total shareholder return of 347% in the last twelve months. Since the one-year TSR is better than the five-year TSR (the latter coming in at 29% per year), it would seem that the stock's performance has improved in recent times. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand Orthocell better, we need to consider many other factors. Even so, be aware that Orthocell is showing 4 warning signs in our investment analysis , and 1 of those makes us a bit uncomfortable...

We will like Orthocell better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:OCC

Orthocell

A regenerative medicine company, develops and commercializes cell therapies and biological medical devices for the repair of various bone and soft tissue injuries in Australia, the United States, the United Kingdom, and the European Union.

Flawless balance sheet very low.

Market Insights

Advertisement