- Australia

- /

- Medical Equipment

- /

- ASX:NAN

ASX Growth Companies With High Insider Ownership Seeing Up To 61% Earnings Growth

Reviewed by Simply Wall St

The Australian market has shown resilience with the ASX200 gaining 1.1% and all sectors marking positive territory, led by IT and Materials. In this buoyant environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong management confidence and potential for substantial earnings growth, making them noteworthy in a flourishing market landscape.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Catalyst Metals (ASX:CYL) | 14.8% | 33.1% |

| Medallion Metals (ASX:MM8) | 12.9% | 72.7% |

| Genmin (ASX:GEN) | 12.3% | 117.7% |

| Acrux (ASX:ACR) | 18.4% | 91.6% |

| Pointerra (ASX:3DP) | 20.8% | 126.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 67.1% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| Brightstar Resources (ASX:BTR) | 14.8% | 84.6% |

Let's dive into some prime choices out of the screener.

Cromwell Property Group (ASX:CMW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Cromwell Property Group (ASX:CMW) is a real estate investor and fund manager with operations across three continents, boasting a market cap of A$1.02 billion.

Operations: Cromwell Property Group generates revenue through its Co-Investments (A$127.50 million), Investment Portfolio (A$194.30 million), and Funds and Asset Management (A$94.90 million) segments.

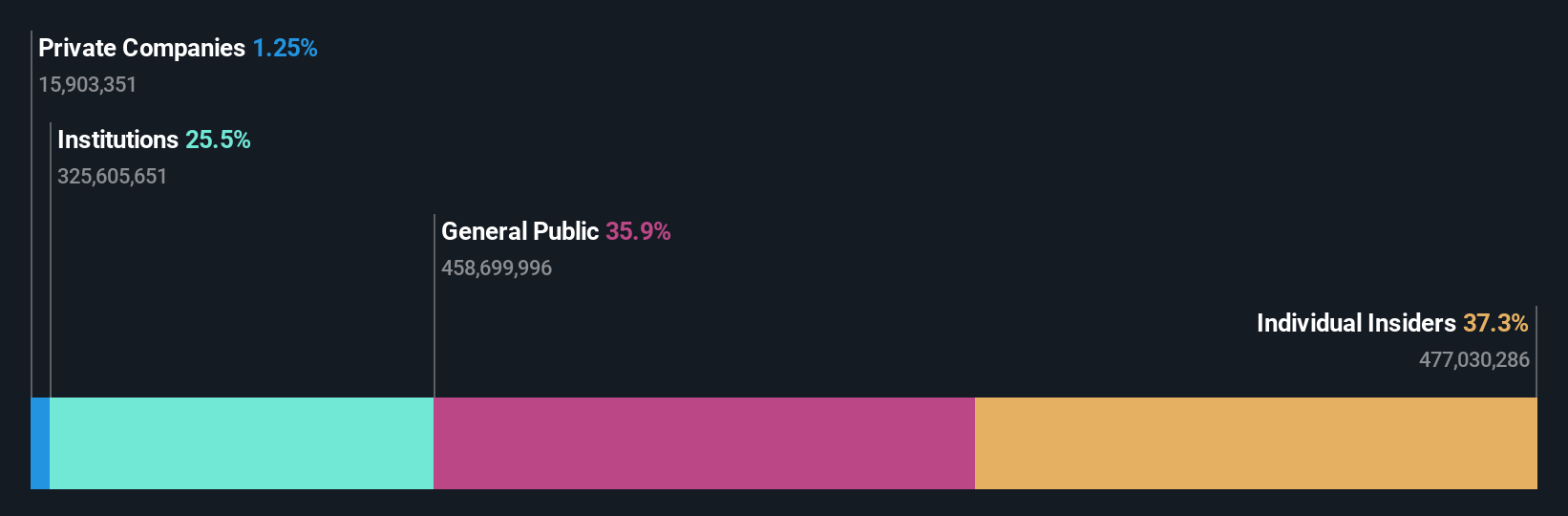

Insider Ownership: 14.0%

Earnings Growth Forecast: 45.9% p.a.

Cromwell Property Group exhibits significant insider ownership, with insiders buying more shares than selling in the past three months. While its earnings are forecast to grow 45.93% annually and it is expected to become profitable within three years, revenue growth at 6.3% per year lags behind high-growth benchmarks but exceeds the Australian market average. Despite trading at good value compared to peers, Cromwell faces challenges with interest coverage and a dividend not well supported by earnings.

- Click here and access our complete growth analysis report to understand the dynamics of Cromwell Property Group.

- Upon reviewing our latest valuation report, Cromwell Property Group's share price might be too pessimistic.

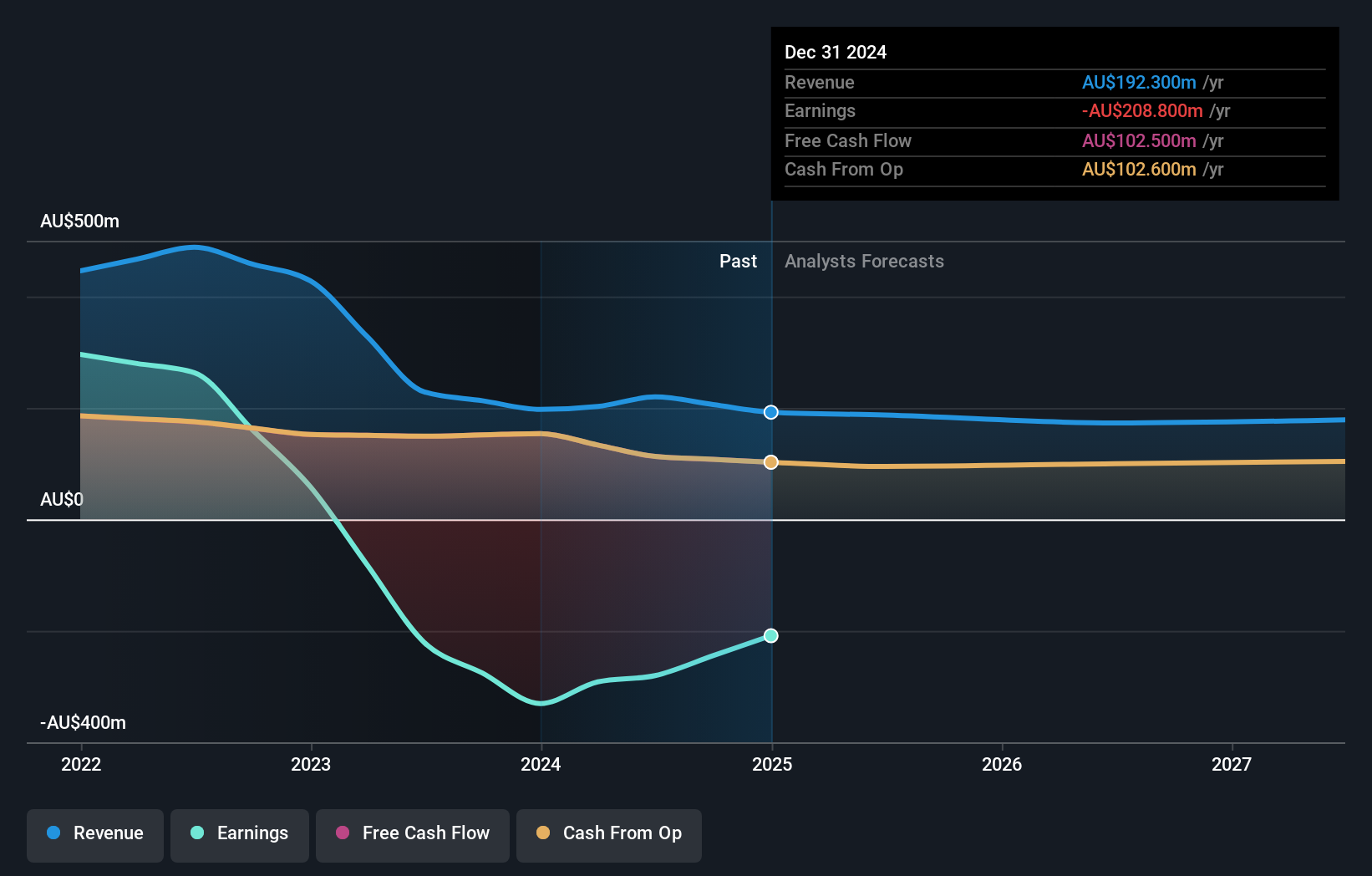

Mesoblast (ASX:MSB)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Mesoblast Limited is a company focused on developing regenerative medicine products across Australia, the United States, Singapore, and Switzerland, with a market capitalization of A$1.54 billion.

Operations: The company's revenue segment consists of $5.90 million from the development of its cell technology platform for commercialization.

Insider Ownership: 24.2%

Earnings Growth Forecast: 61.5% p.a.

Mesoblast insiders have been actively buying shares, aligning with expectations of high revenue growth at 45.8% annually, surpassing the Australian market average. Despite a recent drop from the S&P/ASX Emerging Companies Index and reporting a net loss of US$87.96 million for the year ending June 2024, Mesoblast is trading significantly below its estimated fair value and is forecast to become profitable within three years, indicating potential for future growth.

- Dive into the specifics of Mesoblast here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Mesoblast is trading behind its estimated value.

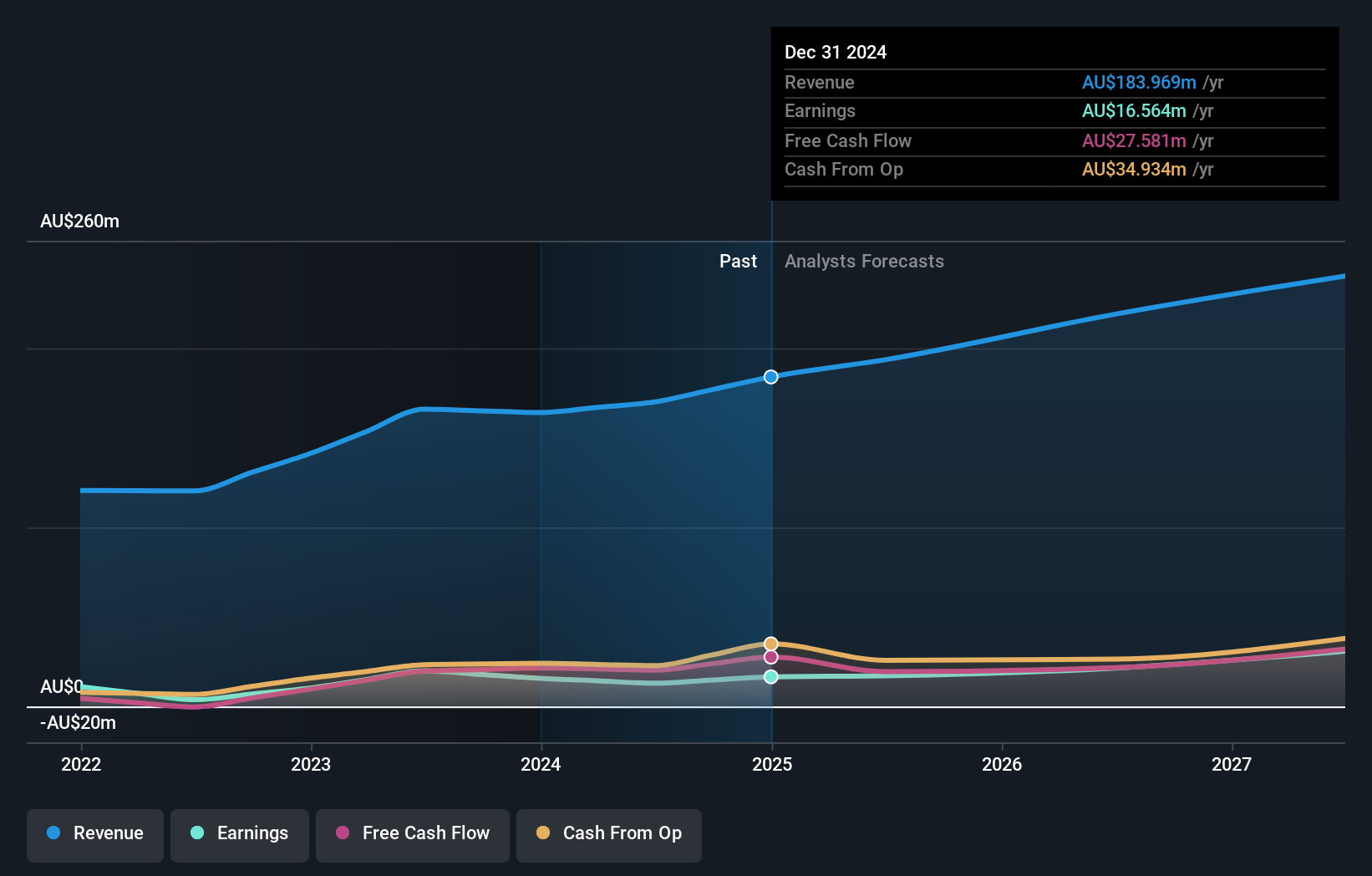

Nanosonics (ASX:NAN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Nanosonics Limited is an infection prevention company operating globally, with a market cap of A$982.91 million.

Operations: The company's revenue is derived entirely from its Healthcare Equipment segment, amounting to A$170.01 million.

Insider Ownership: 15.4%

Earnings Growth Forecast: 23.6% p.a.

Nanosonics has seen more insider buying than selling over the past three months, indicating confidence in its future prospects. The company's earnings are forecast to grow significantly at 23.6% annually, outpacing the Australian market average. However, revenue growth is slower at 8.7%. Despite trading 35.7% below estimated fair value, recent challenges include a drop from the S&P/ASX 200 Index and declining profit margins from last year’s figures.

- Get an in-depth perspective on Nanosonics' performance by reading our analyst estimates report here.

- Our valuation report here indicates Nanosonics may be overvalued.

Taking Advantage

- Access the full spectrum of 93 Fast Growing ASX Companies With High Insider Ownership by clicking on this link.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Nanosonics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:NAN

Flawless balance sheet with reasonable growth potential.