Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:VAU

ASX Value Picks Featuring Judo Capital Holdings And Two Other Stocks With Estimated Low Valuations

Simply Wall St

Reviewed by Simply Wall St

As the Australian market navigates a unique path, diverging from Wall Street to close above the 7,800 points level, investors are keenly observing sector performances with energy leading gains. In this environment of mixed sector outcomes and individual stock volatility, identifying undervalued stocks like Judo Capital Holdings can offer potential opportunities for those looking to capitalize on estimated low valuations.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Acrow (ASX:ACF) | A$1.05 | A$2.04 | 48.6% |

| GenusPlus Group (ASX:GNP) | A$2.60 | A$5.15 | 49.5% |

| Vault Minerals (ASX:VAU) | A$0.485 | A$0.94 | 48.4% |

| Medical Developments International (ASX:MVP) | A$0.45 | A$0.89 | 49.5% |

| Amaero (ASX:3DA) | A$0.23 | A$0.41 | 43.8% |

| Pantoro (ASX:PNR) | A$2.87 | A$5.36 | 46.5% |

| Nuix (ASX:NXL) | A$2.34 | A$4.29 | 45.4% |

| Integral Diagnostics (ASX:IDX) | A$2.25 | A$4.04 | 44.4% |

| Electro Optic Systems Holdings (ASX:EOS) | A$1.205 | A$2.39 | 49.6% |

| Superloop (ASX:SLC) | A$2.29 | A$4.58 | 50% |

We're going to check out a few of the best picks from our screener tool.

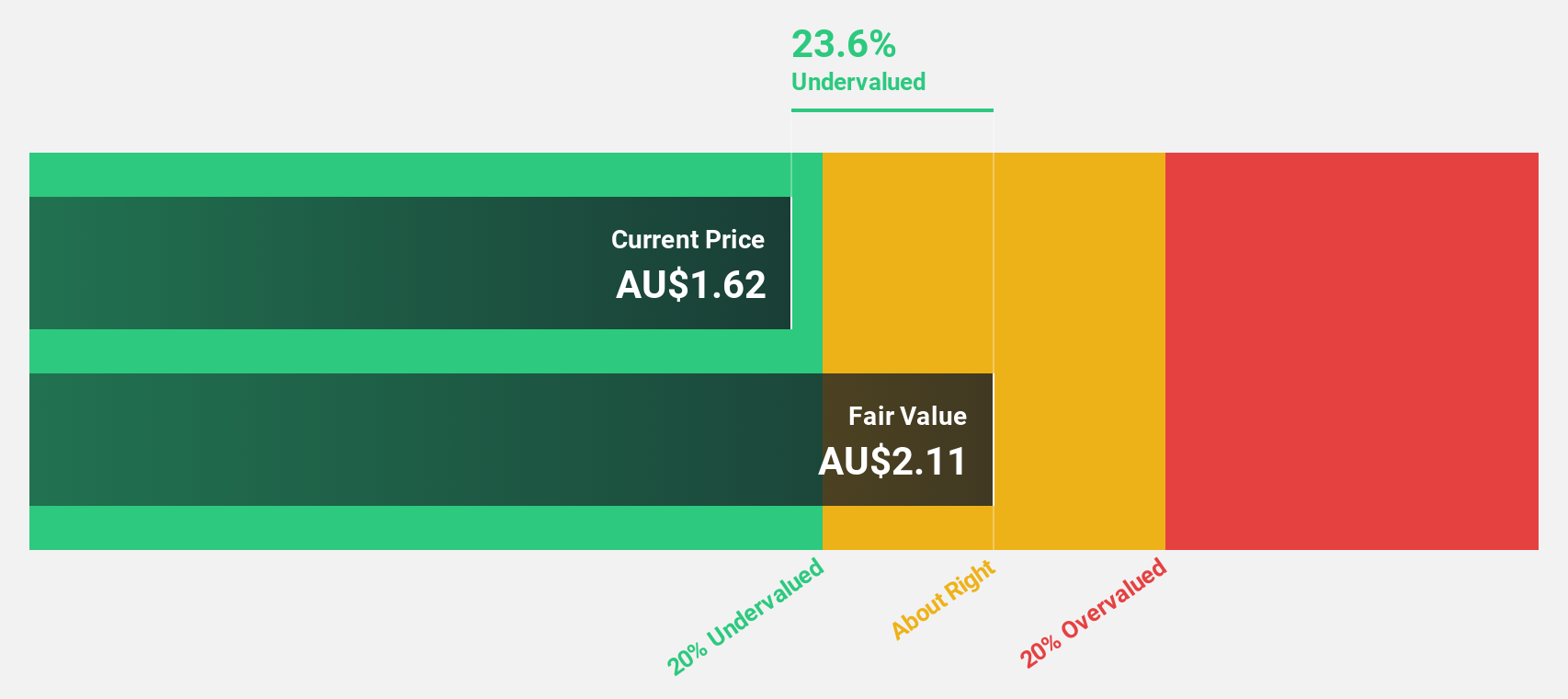

Judo Capital Holdings (ASX:JDO)

Overview: Judo Capital Holdings Limited, with a market cap of A$1.93 billion, provides a range of banking products and services specifically tailored for small and medium businesses in Australia through its subsidiaries.

Operations: Judo Capital Holdings Limited generates revenue of A$325.50 million from its banking products and services aimed at small and medium businesses in Australia.

Estimated Discount To Fair Value: 22.3%

Judo Capital Holdings is trading at A$1.73, below its estimated fair value of A$2.22, indicating it may be undervalued based on cash flows. Despite recent earnings showing a slight decline in net income to A$40.9 million for the half-year ending December 2024, Judo's earnings are forecast to grow significantly at 29.6% annually, outpacing the Australian market average of 11.7%. However, insider selling over the past quarter could be a concern for potential investors.

- In light of our recent growth report, it seems possible that Judo Capital Holdings' financial performance will exceed current levels.

- Delve into the full analysis health report here for a deeper understanding of Judo Capital Holdings.

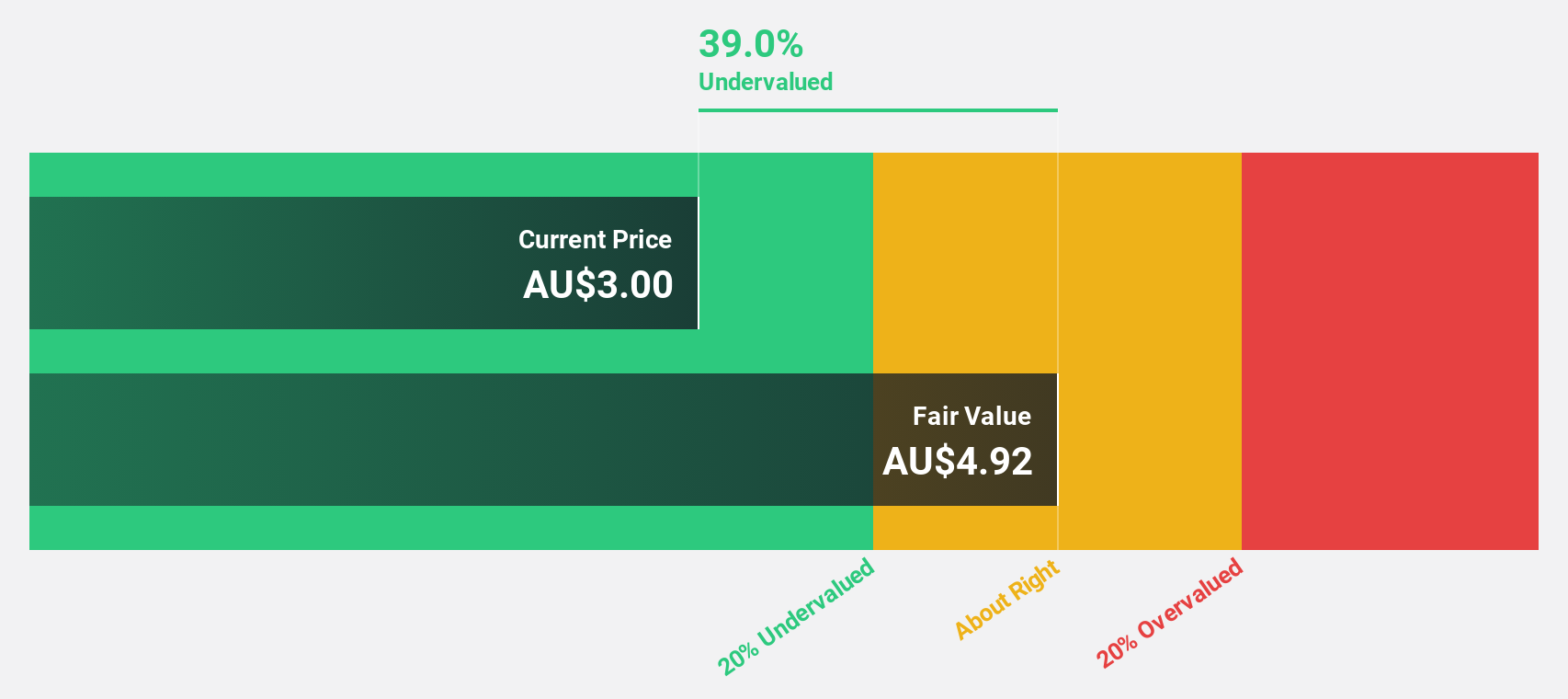

Superloop (ASX:SLC)

Overview: Superloop Limited, along with its subsidiaries, operates as a telecommunications and internet service provider in Australia with a market cap of A$1.17 billion.

Operations: Superloop's revenue is derived from three main segments: Business (A$103.63 million), Consumer (A$316.02 million), and Wholesale (A$60.05 million).

Estimated Discount To Fair Value: 50%

Superloop is trading at A$2.29, significantly below its estimated fair value of A$4.58, highlighting potential undervaluation based on cash flows. Recent earnings results show a reduced net loss of A$7.78 million for the half-year ending December 2024 compared to the previous year's A$18.7 million loss, indicating improving financial health. With revenue forecasted to grow at 13% annually and expected profitability within three years, Superloop presents an intriguing opportunity despite a low future return on equity projection of 11.5%.

- Insights from our recent growth report point to a promising forecast for Superloop's business outlook.

- Click here to discover the nuances of Superloop with our detailed financial health report.

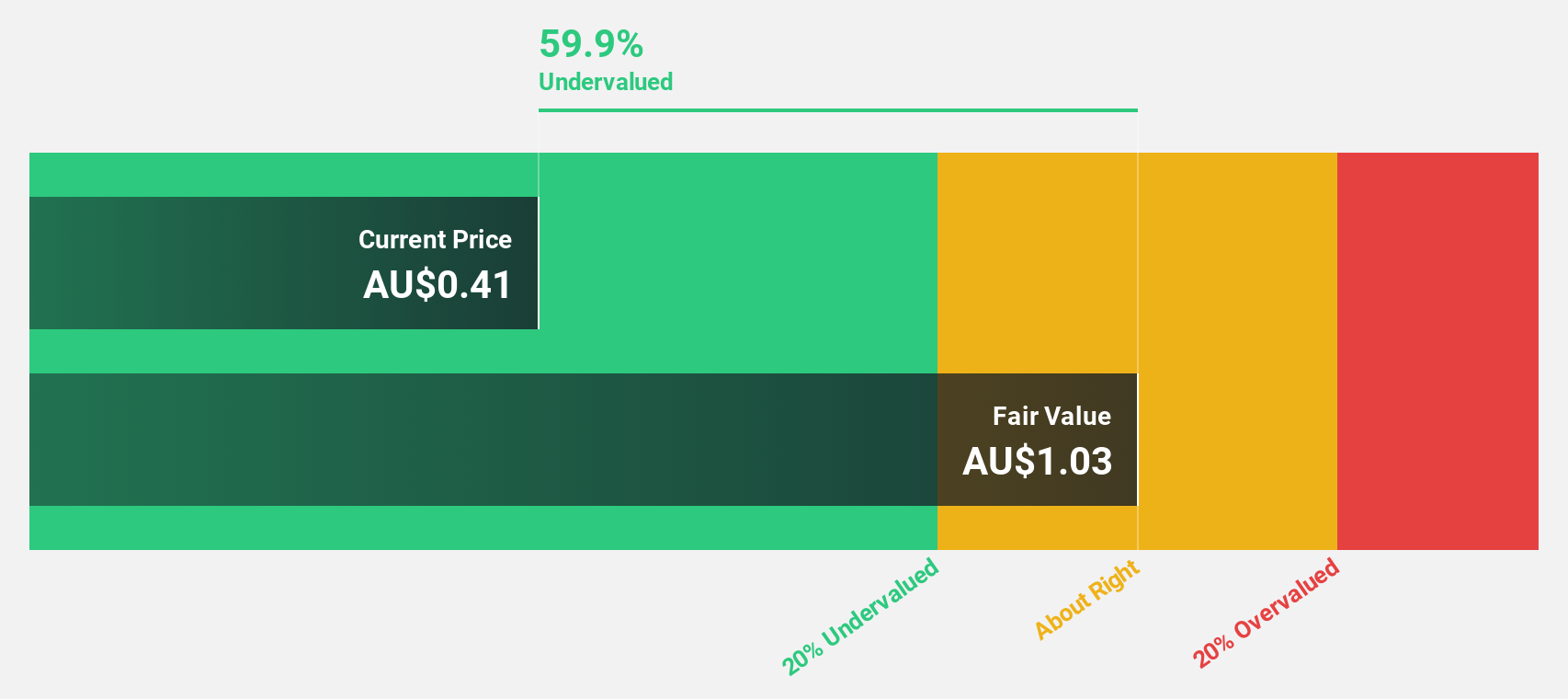

Vault Minerals (ASX:VAU)

Overview: Vault Minerals Limited is involved in the exploration, production, and mining of gold and gold/copper concentrates in Canada and Australia, with a market cap of A$3.30 billion.

Operations: The company's revenue segments include A$605.31 million from the Leonora Operation and a segment adjustment of A$409.98 million.

Estimated Discount To Fair Value: 48.4%

Vault Minerals, trading at A$0.49, is significantly undervalued against an estimated fair value of A$0.94, reflecting potential based on cash flows. Its earnings are forecast to grow 22.05% annually over the next three years, outpacing the Australian market's growth rate of 11.7%. Recent results show a substantial increase in sales to A$678.76 million and net income to A$119.29 million for H1 2024-25, despite shareholder dilution and low future return on equity projections (12.4%).

- Our growth report here indicates Vault Minerals may be poised for an improving outlook.

- Navigate through the intricacies of Vault Minerals with our comprehensive financial health report here.

Summing It All Up

- Unlock more gems! Our Undervalued ASX Stocks Based On Cash Flows screener has unearthed 37 more companies for you to explore.Click here to unveil our expertly curated list of 40 Undervalued ASX Stocks Based On Cash Flows.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:VAU

Vault Minerals

Engages in the exploration, mine development, mine operations and the sale of gold and gold/copper concentrate in Australia and Canada.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor