- Australia

- /

- Metals and Mining

- /

- ASX:NCM

Shareholders Should Look Hard At Newcrest Mining Limited’s (ASX:NCM) 5.8% Return On Capital

Today we are going to look at Newcrest Mining Limited (ASX:NCM) to see whether it might be an attractive investment prospect. In particular, we'll consider its Return On Capital Employed (ROCE), as that can give us insight into how profitably the company is able to employ capital in its business.

First up, we'll look at what ROCE is and how we calculate it. Then we'll compare its ROCE to similar companies. Then we'll determine how its current liabilities are affecting its ROCE.

Understanding Return On Capital Employed (ROCE)

ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. In general, businesses with a higher ROCE are usually better quality. Overall, it is a valuable metric that has its flaws. Renowned investment researcher Michael Mauboussin has suggested that a high ROCE can indicate that 'one dollar invested in the company generates value of more than one dollar'.

How Do You Calculate Return On Capital Employed?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Newcrest Mining:

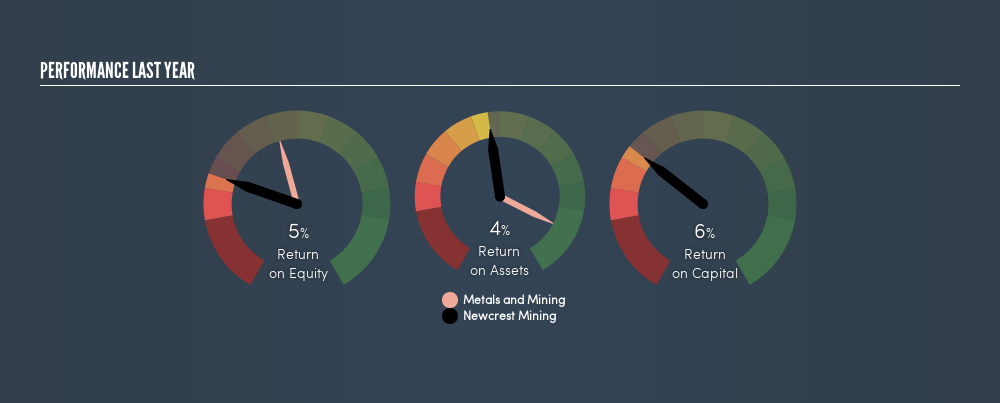

0.058 = US$621m ÷ (US$11b - US$637m) (Based on the trailing twelve months to December 2018.)

So, Newcrest Mining has an ROCE of 5.8%.

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

See our latest analysis for Newcrest Mining

Does Newcrest Mining Have A Good ROCE?

One way to assess ROCE is to compare similar companies. We can see Newcrest Mining's ROCE is meaningfully below the Metals and Mining industry average of 9.5%. This performance could be negative if sustained, as it suggests the business may underperform its industry. Separate from how Newcrest Mining stacks up against its industry, its ROCE in absolute terms is mediocre; relative to the returns on government bonds. Readers may find more attractive investment prospects elsewhere.

It is important to remember that ROCE shows past performance, and is not necessarily predictive. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. ROCE is only a point-in-time measure. Remember that most companies like Newcrest Mining are cyclical businesses. Since the future is so important for investors, you should check out our free report on analyst forecasts for Newcrest Mining.

Do Newcrest Mining's Current Liabilities Skew Its ROCE?

Liabilities, such as supplier bills and bank overdrafts, are referred to as current liabilities if they need to be paid within 12 months. Due to the way the ROCE equation works, having large bills due in the near term can make it look as though a company has less capital employed, and thus a higher ROCE than usual. To counteract this, we check if a company has high current liabilities, relative to its total assets.

Newcrest Mining has total liabilities of US$637m and total assets of US$11b. Therefore its current liabilities are equivalent to approximately 5.6% of its total assets. Newcrest Mining reports few current liabilities, which have a negligible impact on its unremarkable ROCE.

Our Take On Newcrest Mining's ROCE

Based on this information, Newcrest Mining appears to be a mediocre business. You might be able to find a better investment than Newcrest Mining. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:NCM

Newcrest Mining

Newcrest Mining Limited, together with its subsidiaries, engages in the exploration, mine development, mine operation, and sale of gold and gold/copper concentrates.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)