Advertisement

- Australia

- /

- Hospitality

- /

- ASX:FLT

ASX Growth Leaders With High Insider Stakes In July 2024

Simply Wall St

Reviewed by Simply Wall St

Amidst a generally positive trend in the Australian market with all sectors showing gains, and despite some challenges in consumer sentiment due to inflation concerns, investors continue to seek robust growth opportunities. Companies with high insider ownership often attract attention as they can signal strong confidence from those closest to the business, aligning well with current market dynamics where informed decision-making is key.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 26.7% |

| Biome Australia (ASX:BIO) | 34.5% | 114.4% |

| Liontown Resources (ASX:LTR) | 16.4% | 59.5% |

| Ora Banda Mining (ASX:OBM) | 10.2% | 94.3% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Change Financial (ASX:CCA) | 26.6% | 76.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| CardieX (ASX:CDX) | 12.2% | 115.3% |

We'll examine a selection from our screener results.

Emerald Resources (ASX:EMR)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Emerald Resources NL is a company focused on the exploration and development of mineral reserves in Cambodia and Australia, with a market capitalization of approximately A$2.51 billion.

Operations: The company generates revenue primarily from mine operations, which totaled A$339.32 million.

Insider Ownership: 18.5%

Return On Equity Forecast: 21% (2026 estimate)

Emerald Resources, with significant insider ownership, shows promising growth prospects in the Australian market. Its earnings are expected to grow by 23.2% annually, outpacing the market's 13.1%, while revenue forecasts also exceed market averages at an 18.6% increase per year. Despite some shareholder dilution last year, Emerald's robust projected Return on Equity of 20.7% underscores its potential for strong financial performance and stakeholder value creation in the coming years.

- Click here and access our complete growth analysis report to understand the dynamics of Emerald Resources.

- The valuation report we've compiled suggests that Emerald Resources' current price could be inflated.

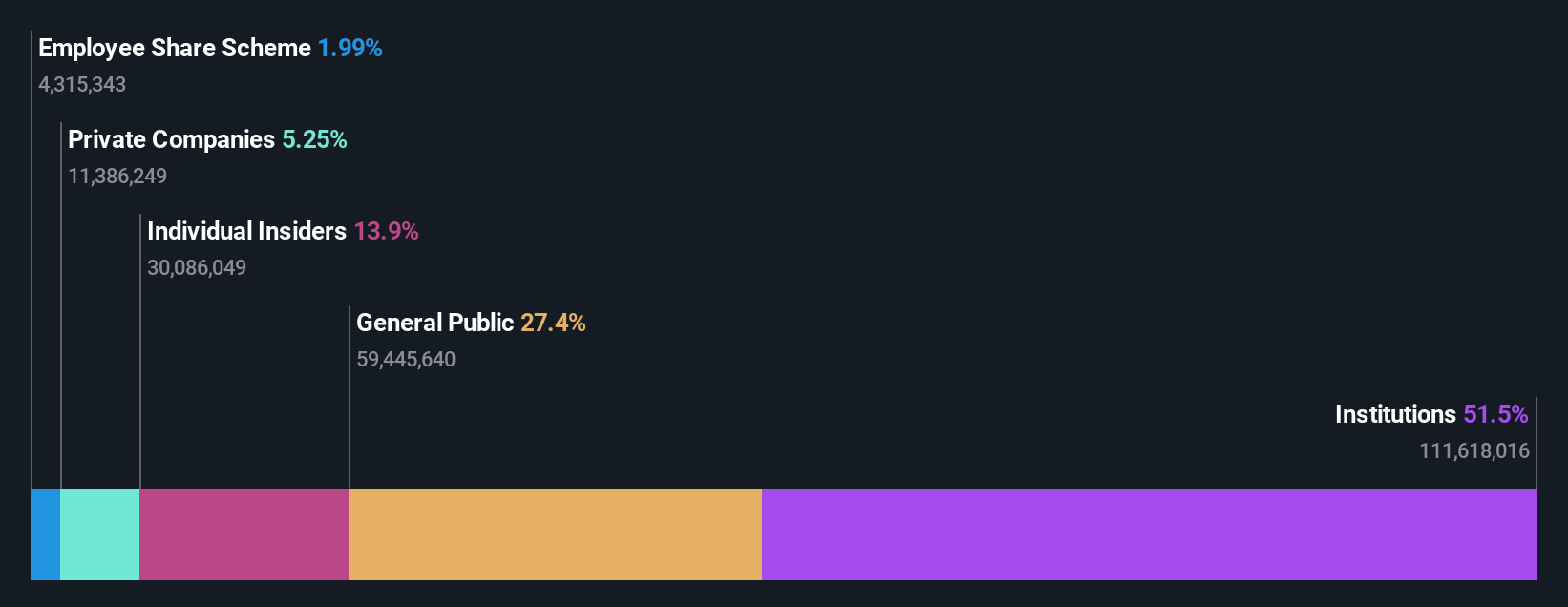

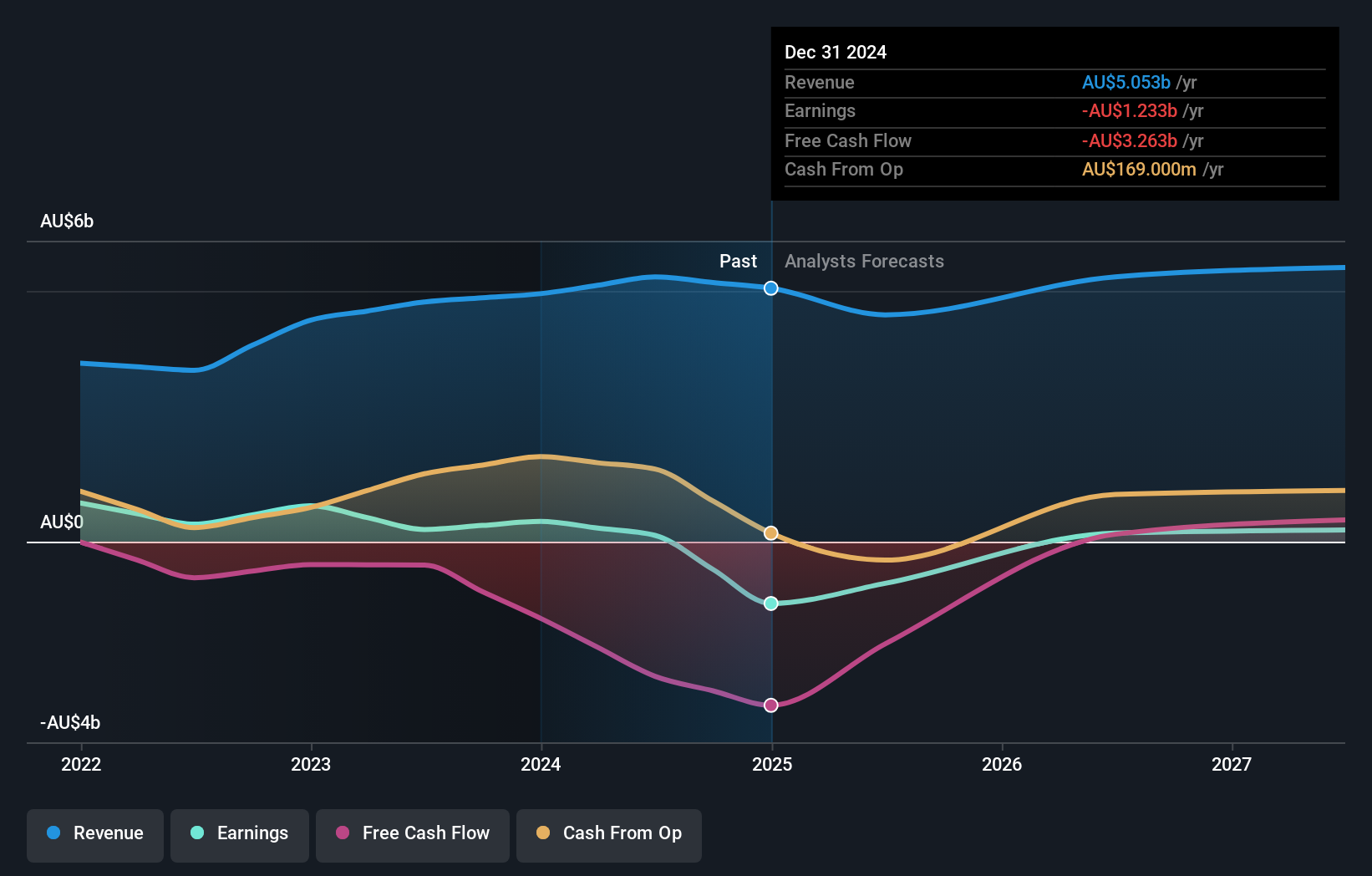

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across Australia, New Zealand, the Americas, Europe, the Middle East, Africa, and Asia with a market capitalization of A$4.70 billion.

Operations: The company generates A$1.28 billion from its leisure segment and A$1.06 billion from its corporate travel services.

Insider Ownership: 13.3%

Return On Equity Forecast: 22% (2026 estimate)

Flight Centre Travel Group, with substantial insider ownership, is poised for notable growth. The company recently became profitable and is trading 17.1% below its estimated fair value. Forecasted earnings growth stands at 18.8% annually, surpassing the Australian market's average of 13.1%. While its revenue growth forecast of 9.7% per year also exceeds the market expectation of 5.3%, it does not reach the high-growth threshold of over 20%.

- Click to explore a detailed breakdown of our findings in Flight Centre Travel Group's earnings growth report.

- Upon reviewing our latest valuation report, Flight Centre Travel Group's share price might be too pessimistic.

Mineral Resources (ASX:MIN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Mineral Resources Limited, a mining services company with operations in Australia, Asia, and internationally, has a market capitalization of approximately A$11.02 billion.

Operations: The company's revenue is derived from lithium (A$1.60 billion), iron ore (A$2.50 billion), and mining services (A$2.82 billion).

Insider Ownership: 11.6%

Return On Equity Forecast: 26% (2026 estimate)

Mineral Resources, characterized by high insider ownership, is set to expand with a revenue growth forecast of 12.1% annually, outpacing the Australian market's average of 5.3%. Despite not meeting the high-growth benchmark of 20%, its earnings are expected to surge by 27.5% per year. However, challenges persist as profit margins have declined from last year and interest payments are poorly covered by earnings. The stock is currently valued at 40.7% below its fair value estimate.

- Get an in-depth perspective on Mineral Resources' performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Mineral Resources shares in the market.

Make It Happen

- Click here to access our complete index of 91 Fast Growing ASX Companies With High Insider Ownership.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:FLT

Flight Centre Travel Group

Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

Very undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor