Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:EVN

Is Evolution Mining’s (ASX:EVN) Dividend Steadiness And Lithium Foray Quietly Recasting Its Risk Profile?

Reviewed by Sasha Jovanovic

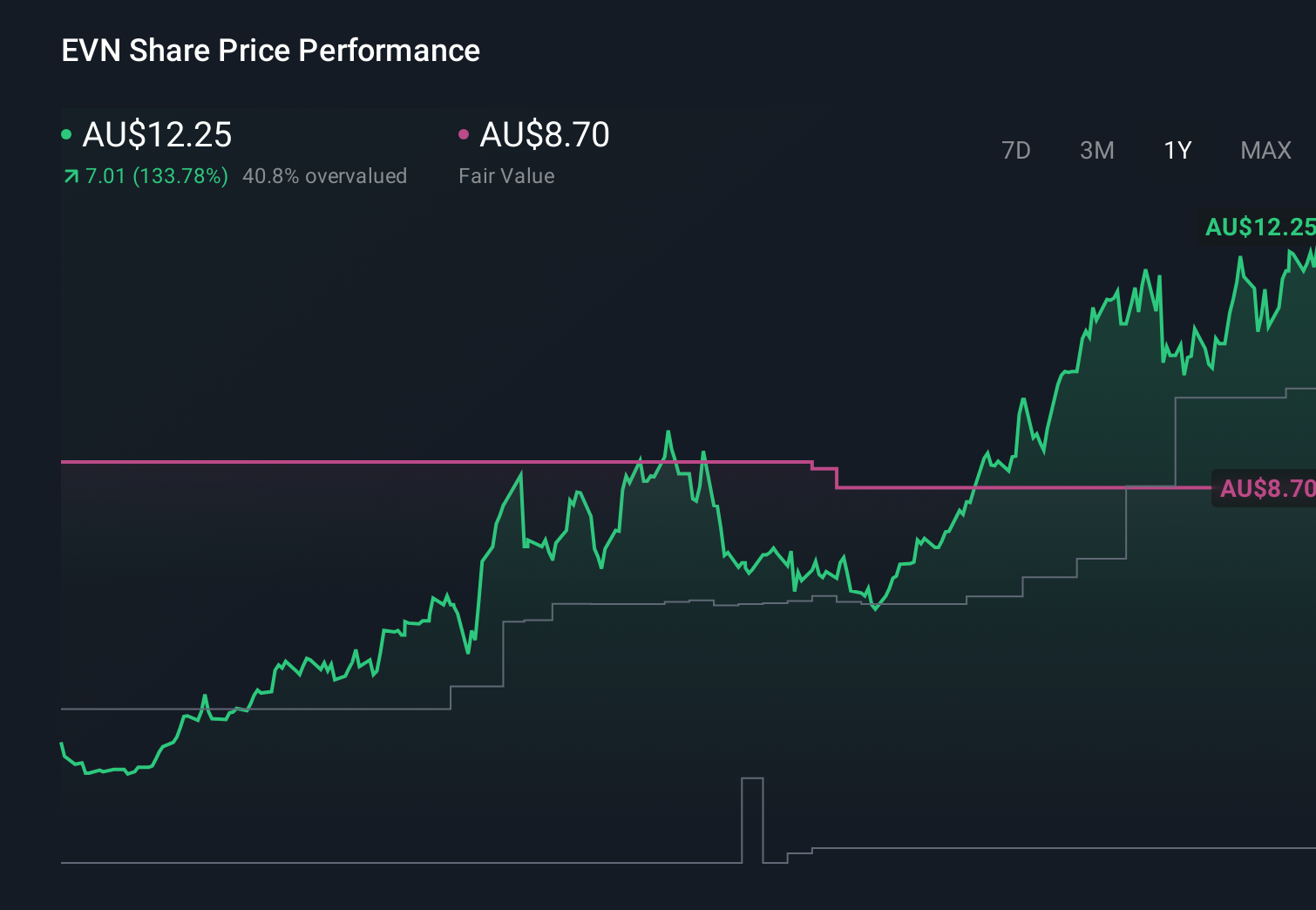

- In recent trading, Evolution Mining reaffirmed its full-year gold and copper production guidance, maintained its all-in sustaining cost outlook, and confirmed a fully franked interim dividend with the ex-dividend date having passed on March 3.

- Alongside these gold-focused developments, new assay results from its Nevada North Lithium joint venture with Surge Battery Metals highlight Evolution’s involvement in lithium exploration as part of its broader resource portfolio.

- We’ll now examine how the reaffirmed guidance and dividend announcement may influence Evolution Mining’s existing investment narrative and risk profile.

We've uncovered the 6 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Evolution Mining Investment Narrative Recap

To own Evolution Mining, you need to be comfortable with a gold producer whose fortunes are closely tied to gold prices and disciplined cost control, while increasingly exposed to long term ESG and regulatory pressures at key sites. The reaffirmed production and cost guidance, together with the confirmed interim dividend, supports the near term cash flow and capital management story, but does not appear to materially change the key short term swing factor, which remains gold price volatility versus rising input and compliance costs.

The fully franked interim dividend of A$0.20 per share, backed by record half year net profit of A$766.57 million on A$2,794.35 million of sales, is the most relevant recent announcement here. It anchors the current income and capital return angle that some shareholders focus on, but it also sharpens the question of how sustainable such payouts are if margins come under pressure from higher operating and ESG related costs over time.

Yet while the dividend looks appealing today, investors should be aware that rising tailings, water and closure compliance costs at assets like Mt Rawdon could...

Read the full narrative on Evolution Mining (it's free!)

Evolution Mining's narrative projects A$4.9 billion revenue and A$1.1 billion earnings by 2028.

Uncover how Evolution Mining's forecasts yield a A$13.17 fair value, a 21% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming earnings would fall to about A$721.4 million by 2028, so compared with consensus they paint a much sharper margin squeeze story that might or might not be softened by Evolution’s latest guidance and lithium JV progress.

Explore 6 other fair value estimates on Evolution Mining - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Evolution Mining research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Evolution Mining research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Evolution Mining's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 10 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evolution Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EVN

Evolution Mining

Engages in the exploration, mine development and operation, and sale of gold and gold-copper concentrates in Australia and Canada.

Outstanding track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative