Advertisement

Should Shareholders Reconsider Lynch Group Holdings Limited's (ASX:LGL) CEO Compensation Package?

Key Insights

- Lynch Group Holdings to hold its Annual General Meeting on 22nd of November

- Total pay for CEO Hugh Toll includes AU$604.7k salary

- Total compensation is 96% above industry average

- Lynch Group Holdings' three-year loss to shareholders was 38% while its EPS was down 108% over the past three years

Shareholders will probably not be too impressed with the underwhelming results at Lynch Group Holdings Limited (ASX:LGL) recently. At the upcoming AGM on 22nd of November, shareholders can hear from the board including their plans for turning around performance. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

See our latest analysis for Lynch Group Holdings

Comparing Lynch Group Holdings Limited's CEO Compensation With The Industry

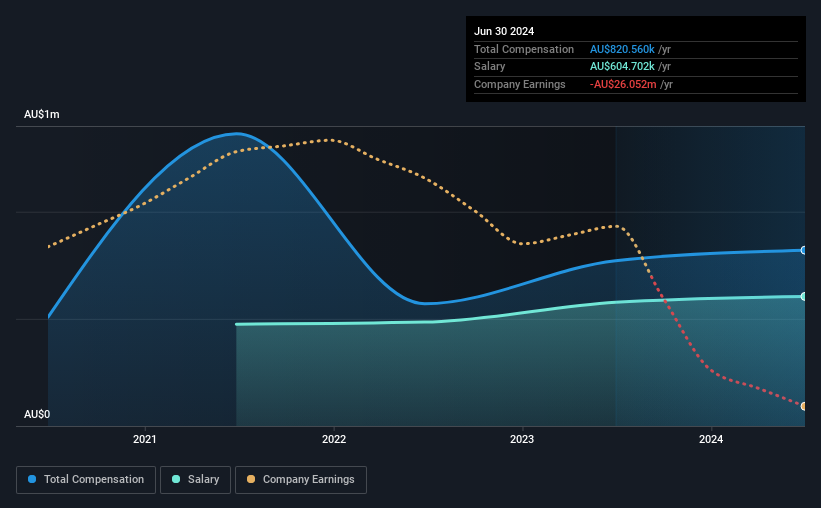

According to our data, Lynch Group Holdings Limited has a market capitalization of AU$212m, and paid its CEO total annual compensation worth AU$821k over the year to June 2024. That's a fairly small increase of 6.4% over the previous year. We note that the salary portion, which stands at AU$604.7k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Australian Food industry with market capitalizations below AU$309m, we found that the median total CEO compensation was AU$419k. Hence, we can conclude that Hugh Toll is remunerated higher than the industry median. Furthermore, Hugh Toll directly owns AU$1.1m worth of shares in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | AU$605k | AU$578k | 74% |

| Other | AU$216k | AU$194k | 26% |

| Total Compensation | AU$821k | AU$771k | 100% |

On an industry level, roughly 62% of total compensation represents salary and 38% is other remuneration. Lynch Group Holdings pays out 74% of remuneration in the form of a salary, significantly higher than the industry average. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Lynch Group Holdings Limited's Growth Numbers

Over the last three years, Lynch Group Holdings Limited has shrunk its earnings per share by 108% per year. In the last year, its revenue changed by just 0.7%.

Few shareholders would be pleased to read that EPS have declined. And the flat revenue is seriously uninspiring. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Lynch Group Holdings Limited Been A Good Investment?

The return of -38% over three years would not have pleased Lynch Group Holdings Limited shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 1 warning sign for Lynch Group Holdings that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:LGL

Lynch Group Holdings

Operates as a grower, wholesaler, retailer, and importer of flowers and potted plants in Australia and China.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor