Clean Seas Seafood Limited's (ASX:CSS) 32% Share Price Plunge Could Signal Some Risk

Clean Seas Seafood Limited (ASX:CSS) shareholders won't be pleased to see that the share price has had a very rough month, dropping 32% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 45% share price drop.

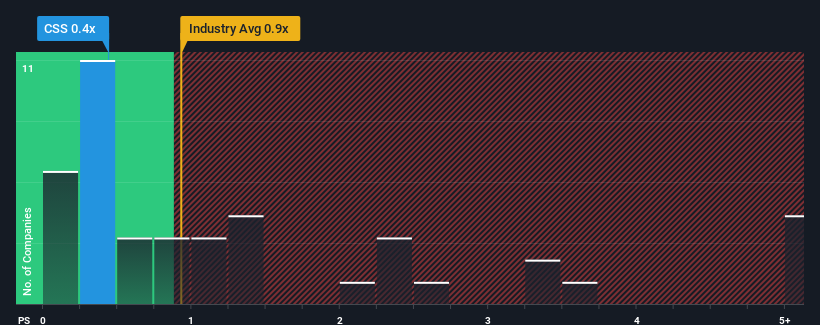

In spite of the heavy fall in price, there still wouldn't be many who think Clean Seas Seafood's price-to-sales (or "P/S") ratio of 0.4x is worth a mention when the median P/S in Australia's Food industry is similar at about 0.9x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Clean Seas Seafood

What Does Clean Seas Seafood's Recent Performance Look Like?

Clean Seas Seafood hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Clean Seas Seafood will help you uncover what's on the horizon.How Is Clean Seas Seafood's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Clean Seas Seafood's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Although pleasingly revenue has lifted 42% in aggregate from three years ago, notwithstanding the last 12 months. Therefore, it's fair to say the revenue growth recently has been great for the company, but investors will want to ask why it has slowed to such an extent.

Shifting to the future, estimates from the only analyst covering the company suggest revenue should grow by 0.8% per year over the next three years. That's shaping up to be materially lower than the 6.5% per annum growth forecast for the broader industry.

In light of this, it's curious that Clean Seas Seafood's P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Bottom Line On Clean Seas Seafood's P/S

With its share price dropping off a cliff, the P/S for Clean Seas Seafood looks to be in line with the rest of the Food industry. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

When you consider that Clean Seas Seafood's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Before you take the next step, you should know about the 4 warning signs for Clean Seas Seafood that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CSS

Clean Seas Seafood

Operates in the aquaculture industry in Australia, Europe, North America, Asia, and internationally.

Slight and slightly overvalued.