- Australia

- /

- Oil and Gas

- /

- ASX:VEA

Should Weak Q3 Sales and Refining Intake Prompt Action From Viva Energy (ASX:VEA) Investors?

Reviewed by Sasha Jovanovic

- Viva Energy Group recently reported a decrease in third-quarter convenience sales to A$392 million and a 23% drop in refining intake, primarily due to maintenance activities.

- This update also highlighted the impact of regulatory changes on tobacco sales and rising in-store wage costs affecting the company’s operations.

- We'll examine how weaker convenience sales amid regulatory pressures could influence Viva Energy Group’s investment case moving forward.

Find companies with promising cash flow potential yet trading below their fair value.

Viva Energy Group Investment Narrative Recap

Viva Energy Group’s investment story is built on its ability to successfully expand higher-margin convenience offerings while maintaining a resilient fuel retail business amid industry transition. The recent decline in third-quarter convenience sales and refining volumes appears to underscore heightened regulatory pressures and cost challenges, with weaker non-fuel sales emerging as the most material short-term risk; however, these factors seem unlikely to fundamentally alter the group’s longer-term retail shift, which is still the central catalyst for improved returns. Among recent company updates, the appointment of Jennifer Gray as Interim CEO for the Convenience and Mobility business is directly relevant to these short-term headwinds. With executive focus now sharpened on store-level priorities, investors will be watching how leadership manages wage inflation and the rollout of retail transformations as these could influence store profitability in the months ahead. Yet, it’s the persistently falling tobacco sales, amid ongoing regulatory changes and shifting consumer habits, that investors should closely consider...

Read the full narrative on Viva Energy Group (it's free!)

Viva Energy Group's narrative projects A$30.9 billion in revenue and A$405.0 million in earnings by 2028. This requires a yearly revenue decline of 0.1% and an earnings increase of A$756.7 million from the current earnings of A$-351.7 million.

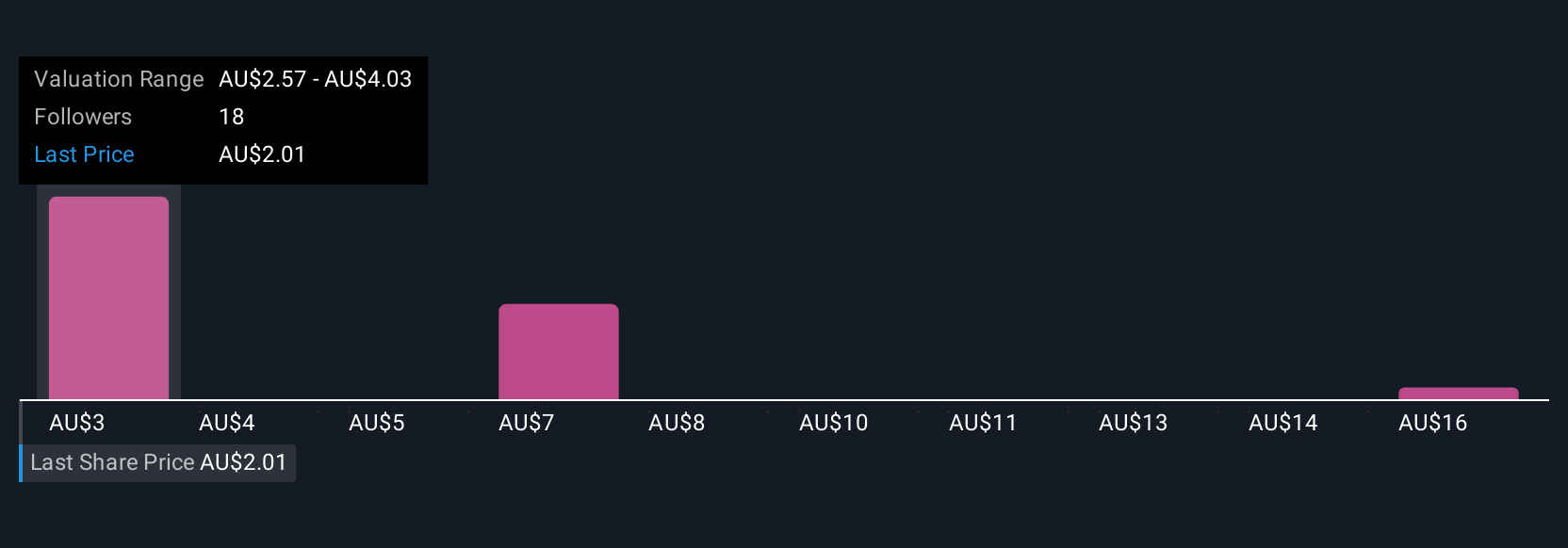

Uncover how Viva Energy Group's forecasts yield a A$2.57 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Six separate community members on Simply Wall St valued Viva Energy Group between A$2.45 and A$17.19 per share. Alongside this wide gap, the short-term pressures from weaker convenience sales and regulatory change illustrate why understanding the range of opinions can be critical when assessing future prospects.

Explore 6 other fair value estimates on Viva Energy Group - why the stock might be worth over 9x more than the current price!

Build Your Own Viva Energy Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Viva Energy Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Viva Energy Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viva Energy Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:VEA

Viva Energy Group

Operates as an energy company in Australia, Singapore, and Papua New Guinea.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)