- Australia

- /

- Consumer Finance

- /

- ASX:ZIP

Zip Co (ASX:ZIP): Valuation Check After Recent Buy-Backs and New Equity Issuances

Reviewed by Simply Wall St

Zip Co (ASX:ZIP) has been busy reshaping its share base, buying back millions of ordinary shares while simultaneously issuing new securities and performance rights. For investors, these moves quietly reshape dilution, earnings per share and future upside.

See our latest analysis for Zip Co.

These capital moves come after a choppy run, with the share price now at A$3.03 and a modest year to date share price return of 2.02 percent. However, the three year total shareholder return of 388.71 percent suggests long term momentum remains robust even as shorter term share price performance has cooled.

If Zip Co’s repositioning has your attention, this could be a good moment to scan the market for other fintech style names and discover fast growing stocks with high insider ownership

With revenue and earnings still climbing and the share price trading well below consensus targets, the key question now is simple: Is Zip Co undervalued, or is the market already pricing in all that future growth?

Most Popular Narrative Narrative: 40.5% Undervalued

With Zip Co last closing at A$3.03 against a narrative fair value of about A$5.10, the valuation hinges on aggressive growth and expanding margins.

The company's ongoing international expansion, particularly in the underpenetrated U.S. market where BNPL is less than 6% of e-commerce spend, provides significant runway for organic revenue growth and supports geographic diversification, de-risking the business model and enabling long-term scale.

Curious how this growth story justifies a much higher price tag? The narrative leans on rapid revenue compounding, expanding profit margins and a punchy future earnings multiple. Want to see exactly how those moving parts combine into that fair value call?

Result: Fair Value of $5.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising regulatory scrutiny and intensifying BNPL competition could compress margins, slow customer growth and undermine the optimistic fair value narrative.

Find out about the key risks to this Zip Co narrative.

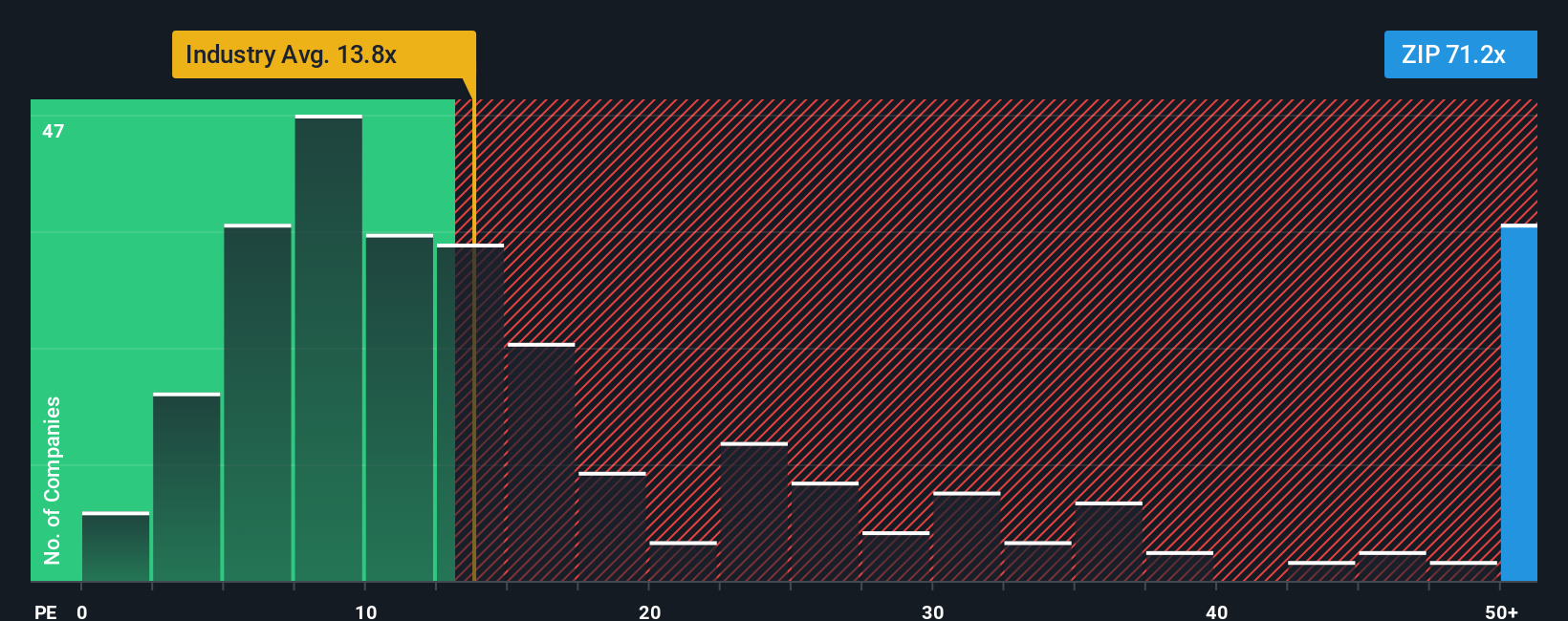

Another Take On Valuation

On earnings, Zip Co looks anything but cheap. Its price to earnings ratio sits around 48.5 times, versus about 11.4 times for peers and a fair ratio closer to 30.1 times, suggesting investors are already paying up for growth and taking on valuation risk. Is that premium really justified?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Zip Co Narrative

If you are not convinced by this view, or would rather dig into the numbers yourself, you can build a custom Zip Co storyline in just a few minutes, Do it your way

A great starting point for your Zip Co research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop at one compelling story. Use the Simply Wall St Screener to uncover your next edge before other investors even start looking.

- Target reliable income by reviewing these 13 dividend stocks with yields > 3% that can strengthen your portfolio with consistent cash returns.

- Capture tomorrow’s tech leaders early by scanning these 26 AI penny stocks shaping the future of automation and intelligence.

- Capitalize on mispriced opportunities through these 909 undervalued stocks based on cash flows that may offer strong upside based on solid cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Zip Co might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:ZIP

Zip Co

Engages in the provision of digital retail finance, personal finance, and payments solutions in Australia, New Zealand, and the United States.

High growth potential with solid track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)