Advertisement

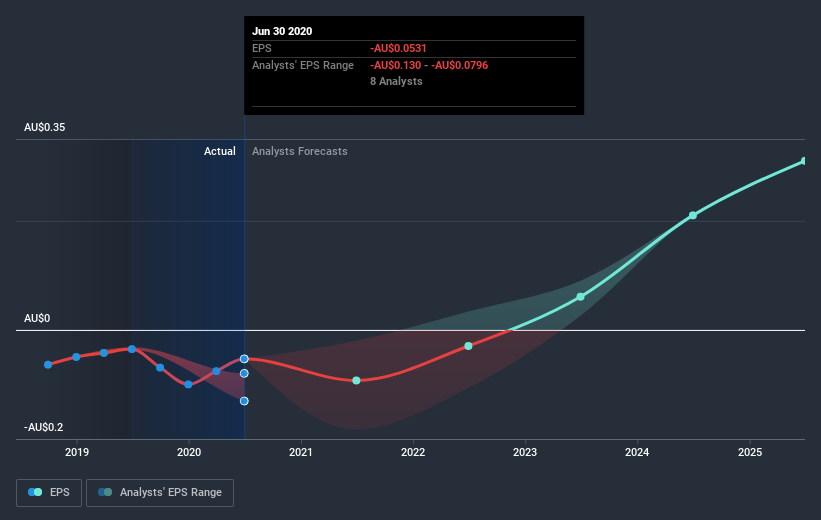

We feel now is a pretty good time to analyse Zip Co Limited's (ASX:Z1P) business as it appears the company may be on the cusp of a considerable accomplishment. Zip Co Limited provides point-of-sale credit and digital payment services to consumers and merchants in Australia, the United Kingdom, the United States, New Zealand, and South Africa. On 30 June 2020, the AU$5.4b market-cap company posted a loss of AU$20m for its most recent financial year. The most pressing concern for investors is Zip Co's path to profitability – when will it breakeven? In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

Check out our latest analysis for Zip Co

According to the 9 industry analysts covering Zip Co, the consensus is that breakeven is near. They anticipate the company to incur a final loss in 2022, before generating positive profits of AU$16m in 2023. So, the company is predicted to breakeven approximately 2 years from now. How fast will the company have to grow each year in order to reach the breakeven point by 2023? Working backwards from analyst estimates, it turns out that they expect the company to grow 47% year-on-year, on average, which is extremely buoyant. If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

Given this is a high-level overview, we won’t go into details of Zip Co's upcoming projects, though, keep in mind that generally a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

One thing we would like to bring into light with Zip Co is its debt-to-equity ratio of over 2x. Typically, debt shouldn’t exceed 40% of your equity, and the company has considerably exceeded this. Note that a higher debt obligation increases the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on Zip Co, so if you are interested in understanding the company at a deeper level, take a look at Zip Co's company page on Simply Wall St. We've also put together a list of essential factors you should further examine:

- Historical Track Record: What has Zip Co's performance been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Zip Co's board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you’re looking to trade Zip Co, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Zip Co might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:ZIP

Zip Co

Engages in the provision of digital retail finance, personal finance, and payments solutions in Australia, New Zealand, and the United States.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|24.5% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|24.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|97.7% undervalued

RO

Community Contributor